Impact investing is facing an identity crisis as many in the global finance community try to convince themselves – and others – that holding a portfolio of listed equities can be regarded as impact investing.

The crisis has been brought on by a genuine desire to ‘scale’ impact investing so that it applied more widely to address social and economic challenges; evolving community expectations about where and how their money should be invested; and by a desperate desire by asset owners and managers to litter their marketing documents and prospectuses with the word ‘impact’.

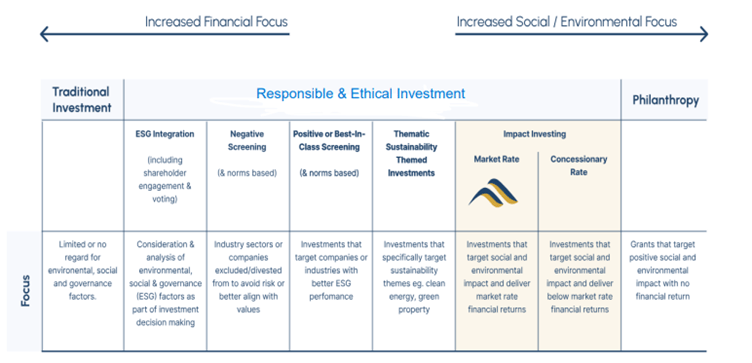

Impact investments are investments made in companies, assets or organisations with the intent to contribute measurable positive social or environmental impact, alongside a financial return, according to the Global Impact Investing Network (GIIN). The three pillars of impact investing are investor intent, investor contribution (or ‘additionality’) and impact measurement.

Earlier this month the CFA Institute, the Global Sustainable Investment Alliance (GSIA) and the UN Principles for Responsible Investment (PRI) jointly released Definitions for Responsible Investment Approaches in an effort to harmonise definitions for terms such as screening, ESG integration, thematic investing, stewardship and impact investing (although the guidance curiously doesn’t include a definition for ‘responsible investment’).

The guidance, which follows the GIIN’s impact investing definition, says impact investing “requires a ‘theory of change’ – that is, a credible explanation of the investor’s contributory and/or catalytic role, as distinct from the investee’s impact”. It is not enough to just allocate capital to investees that have a net positive impact.

Subtracting additionality

The problem here is not everyone is happy with the definition. It is the high bar or hurdle of ‘additionality’ – requiring an investor to be able to identify financial and social value that would not have been otherwise created without their investment or support – that is frustrating those who want to promote themselves as impact investors in listed equities.

London-based impact investment manager WHEB, for example, acknowledges “there is broad agreement that there are two levels of impact in the investment value-chain. That being delivered by the underlying asset (‘enterprise impact’) and that delivered by the investor (‘investor impact’ comprising investor ‘intention’ and ‘contribution’).

However, in its paper Impact investing in listed equities –WHEB’s perspective, WHEB also opines that “this traditionalistic view is necessarily restricted to philanthropic activity, or at best to situations where new capital is invested in markets with very poor liquidity”.

WHEB prefers a ‘holistic’ view that “recognises the ‘intense’ impact generated by investments demonstrating additionality, but also embraces a spectrum of more ‘diffuse’ positive impact delivered through other mechanisms. These include changes in the cost of capital, engagement and wider signalling”.

However, it would be difficult for an individual super fund to demonstrate or attempt to measure how it reduced the cost of capital for a medium or large-sized listed company. And the jury is still definitely out when it comes to judging the quality and effectiveness of the investee engagement and ‘active ownership’ strategies of asset owners and managers.

Listed equities

In its Guidance For Pursuing Impact In Listed Equities, the GIIN examines the issue. “As an asset class, listed equities are idiosyncratic by nature, such that it is not possible to exactly replicate many of the impact practices used in other asset classes,” according to the GIIN.

GIIN says “holding shares with patience in highly illiquid or inefficient markets arguably has more influence than shorter-term holdings in large-cap companies trading in the world’s most liquid markets.

“Compared to private market situations where investors may be contributing completely new capital to allow for the expansion of operations, investor contribution in listed equities through secondary trading is harder to measure, and attribution is more complex”.

Individual investors in listed equities tend to have less concentrated ownership in a single investee, instead focusing on portfolio diversity, which can “limit their ability to engage with and influence companies,” the GIIN says.

And perhaps the biggest problem is that “managers in the listed equities asset class often face implicit, significant market pressure to match the attributes of a given benchmark as they design their portfolios, which can constrain the perceived scope for innovation”.

In this situation it would therefore be difficult, for example, for an asset owner or manager to accept lower returns or to have a higher risk tolerance by offering investment or funding on concessionary terms – as impact investors often do through the catalytic ‘blended finance’ model used to support difficult-to-fund projects.

Meanwhile, the GIIN itself also seems to have muddied the waters through the recent launch of its ‘Corporate Impact Investing Initiative’ to “help corporations connect their financial assets and capabilities with impact investing practices to realise social and environmental goals”.

The GIIN’s Corporates Deploying Impact Investing Strategies document does make this initiative sound like a new take on corporate social responsibility (CSR) or a shared value approach.

Red flags

So, what should asset owners look out for if they do want to engage an impact investment fund manager for listed equities?

According to Impact Due Diligence And Management For Asset Allocators: A Field Guide prepared by BlueMark and CASE at Duke University, some “red flags” include:

- A weak or vague theory of change where the asset manager’s thesis does not include a problem statement and/or the links between the strategy and expected results are tenuous.

- Conflated impact and ESG goals, where the thesis does not distinguish between the goals associated with ESG risk management and those related to impact, and where impact is considered more of a “bonus” than an intentional outcome of the investment.

- Asset managers producing slick impact reports that look good, but lack rigour. There is reporting on only aggregated figures without context or supporting explanations of the data, using “flashy” presentations to distract from data discrepancies.

Time for a rebalancing act

As universal owners, many super funds may already be invested in the listed companies that an impact fund manager has – or plans to have – in their portfolio. So apart from the brand marketing boost, claiming that you are now impacting investing doesn’t really mean much.

If asset owners and fund managers are concerned that impact investing is too niche – and needs to be reinvented to apply to the huge listed equities asset class – they could instead think about a portfolio rebalance from stockmarkets to private equity (and debt).

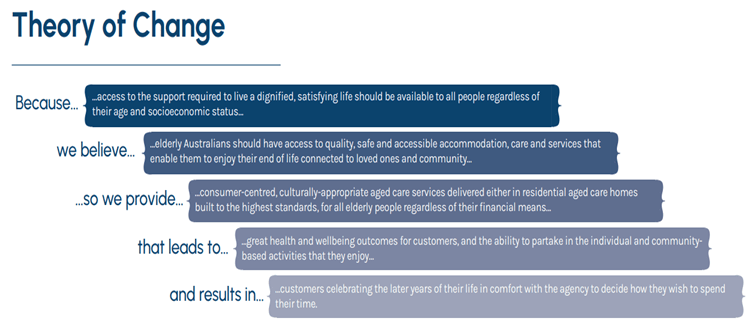

Here, more members’ money could be directed to areas such as aged care, affordable housing, disability accommodation and Indigenous economic empowerment where stronger theories of change can be developed (the illustrative diagram below shows the theory of change For Purpose Investment Partners investee Luson Aged Care).

As our super funds exist to deliver benefits to Australians when they retire, investments made in, for example, the aged care sector are closely aligned with the needs of their members – given so many Australians will interact with, or rely upon, the sector as they grow older.

Many Australians will need to draw upon their retirement savings to secure a place in what they hope will be a high-quality residential aged care facility.

Such investments certainly sound a lot more impactful than continuing to unimaginatively siphon members’ money into the likes of Woodside, Qantas or a big four bank.

Leave a Comment

You must be logged in to post a comment.