As Treasury releases its Superannuation in Retirement consultation paper, we have finalised our paper titled “Pathways for directing members into retirement solutions”, a precursor of which previously appeared in Investment Magazine. We thank those who provided comments on the draft paper, which we very much appreciate. They have led to improvements.

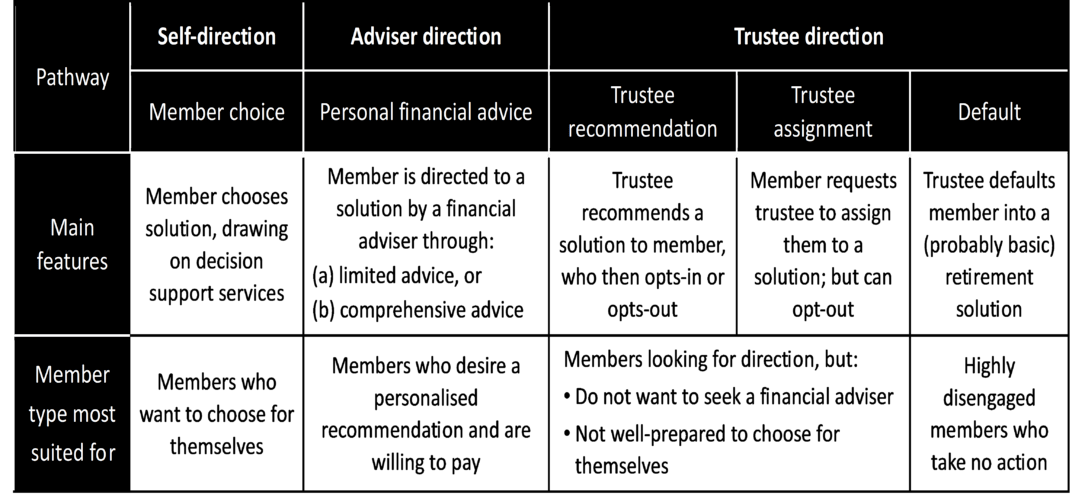

To recap, the paper considers the choice architecture around retirement solutions. It identifies and discusses five potential pathways (see table) through which members might find their way to a suitable solution. We argue a range of pathways is required to cater for the differing ways that members engage with retirement decisions.

The paper itself is largely written as a reference document, which we encourage readers to access for the details and issues around the various pathways. In this article, we reflect on the potential policy implications of our research.

Writing the final version of this paper convinced us even more that some form of trustee direction pathway is necessary to cater to the bulk of retirees who are currently receiving little guidance.

We recognise that trustee direction will most likely be inferior to holistic personal financial advice provided by a financial adviser. However, personal financial advice is quite constrained in offering guidance to all members due to capacity and cost issues. It cannot carry the load by itself.

Currently those members who do not seek or pay for advice are required to make their own retirement decisions, i.e. they land in the self-direction pathway. Many members either don’t want to, or shouldn’t be, choosing for themselves. Some help, even if falling short of the optimum, should be better than no help.

Super funds are best placed to solve this ‘something or nothing’ conundrum. The policy challenge is to facilitate trustee direction in a way that delivers two key things. First is accommodating the ability of funds to provide retirement guidance to members at scale and low cost. Second is protecting members from the harm that could arise from the likely limited nature of the guidance that trustees would offer.

The government initially mentioned using intra-fund advice as the mechanism. In itself, this is insufficient. Intra-fund advice is code for collective charging of all members for an advice service. It is still personal financial advice, and hence attracts the same compliance – and hence cost and scalability – hurdles that are faced by financial advisers.

The government has recently indicated it is looking beyond the funding model, with issues such as scope and education requirements being discussed. The challenge for the government is to create specific rules around what fund trustees are able and expected to do under trustee direction – whether it be facilitated via collective or individual charging.

Let’s speculate how these rules might work.

In terms of what fund trustees are able to do, at the top of our list is an ability to collect personal information to identify which solution is suitable for the member, and then recommend or assign the member a solution. The information that is necessary to undertake this matching process could define the scope of what information that trustees are permitted to collect and use.

For example, say the fund has designed solutions that tailor for members that differ in their total assets including those outside of superannuation, partnered status and homeownership. The trustee might be allowed to collect information on these attributes to match members to solutions, and nothing more.

What trustees are expected to do could hinge around the obligations aimed at ensuring that members are offered suitable solutions. Central to this would be the capacity to deliver a range of solutions that caters for key member differences.

Obligations might also extend to triaging members into a suitable decision pathway. This obligation would include directing members towards personal financial advice where appropriate. Where the member’s situation is complex, or the fund does not offer a suitable solution for their needs, they should be encouraged to take personal advice rather than simply offered a solution.

What we discuss here would amount to creating a separate set of advice rules for super funds. While differing rules for differing players is undesirable, it seems unavoidable if the problem of many members receiving no guidance whatsoever is to be solved. To do so will require addressing a range of issues that we do not address in our paper, such advice process requirements, qualifications and competencies, and legal and regulatory protections.

It is worth mentioning that we harbour doubts over a default pathway whereby trustees assign members to a solution without prior assent. This pathway runs into significant implementation challenges related to dealing with highly disengaged members. We would first prefer to see to what extent other forms of trustee direction can solve the guidance problems.

We encourage the Government to address the issues raised above under stream two of the Delivering Better Financial Outcomes reforms. Further, we hope this reform agenda increases the effectiveness of the adviser direction pathway so that more members can received personal advice from financial advisers at a reasonable cost.

Our wish is that policy changes will allow many more members to receive guidance that leaves them better off than otherwise. While perfection is a bridge too far, it should be possible to create a retirement choice architecture that is better than the one that currently exists.

David Bell is executive director and Geoff Warren is research director of The Conexus Institute, an independent think-tank funded philanthropically by Conexus Financial, publisher of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.