In Mary Shelley’s 1818 novel Frankenstein, the feared monster reflects, “of my creation and creator I was absolutely ignorant, but I knew that I possessed no money, no friends, no kind of property”.

In Senator Andrew Bragg’s shorter 2024 version “Canberra’s Frankenstein”, it seems Australia’s super funds are creatures to be feared because they possess money and property, and (in the case of industry funds) have the wrong sort of friends.

Bragg’s horror narrative says our super funds could “eat up the whole local exchange” and use it for nefarious purposes.

But is this a plausible plot?

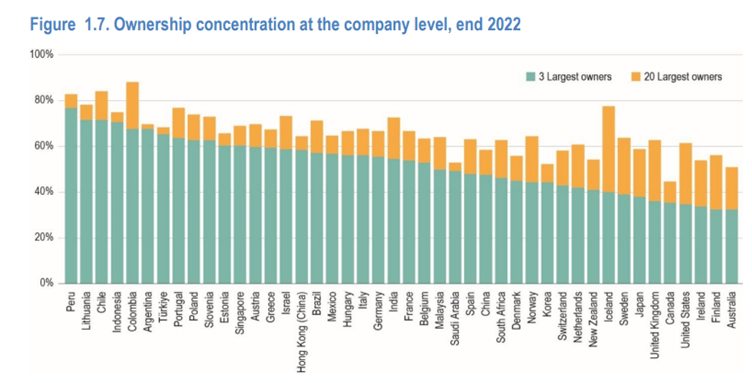

According to the OECD Corporate Governance Factbook 2023, the Australian stock market has the second lowest ownership concentration in the world.

At the company level, Australia has the lowest concentration for the three largest shareholders and only Canada has less when it comes to the top 20 shareholders.

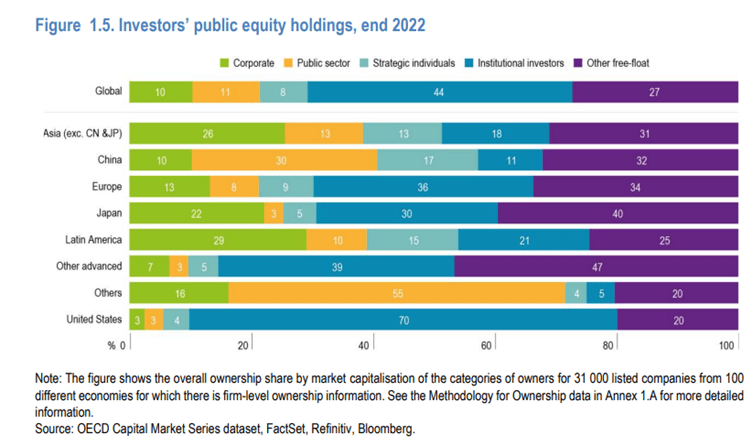

At the global level, institutional investors are the largest owner category, owning 44 per cent of global stock market capitalisation. However, for Australia institutional investors only own 29 per cent of ASX-listed equities by value, according to the OECD Factbook.

The Factbook notes that some key global developments have shifted ownership structures of listed companies towards concentrated ownership models – and institutional investment is only one part of this shift.

The Factbook notes that some key global developments have shifted ownership structures of listed companies towards concentrated ownership models – and institutional investment is only one part of this shift.

Institutional investors are by far the most dominant shareholders in the US, where they own at least 70 per cent of equity. Institutions are also the biggest investors in Europe, Japan and other advanced markets.

(It should be noted the Factbook’s methodology does understate institutional ownership for nearly all countries by categorising additional shares held by institutional investors that do not exceed the required threshold for public disclosure as “other free float”).

Corporations are the most important owners in some regions such as Latin America and Asia (excluding China and Japan) where they own 29 per cent and 26 per cent respectively of market capitalisation.

In half of the markets, at least one-third of all listed companies have a single owner holding more than 50 per cent of the equity capital. In Peru, Argentina, Chile and Indonesia, more than 60 per cent of companies have a single shareholder holding more than half of the equity capital.

Why the shift?

The OECD says the growing importance of Asian companies in stock markets is one factor. “Since Asian companies often have a controlling shareholder – either a corporation, family or the state – their growing presence in capital markets has increased the prevalence of controlled companies,” the OECD notes.

The “rise of institutional investors” is another factor. “While assets under management by institutional investors have increased during the last two decades, many companies in advanced economies have left public equity markets. Therefore, a growing amount of funds flowing into a decreasing number of companies has increased ownership concentration at the company level,” according to the OECD.

The other key factor has been the partial privatisation of many state-owned companies through stock market listings since the 1990s. “In many cases, privatisation through stock market listings has not led to any change in control and today states have controlling stakes in a large number of listed companies, particularly in emerging Asian markets,” the Factbook says.

This highlights the fact that different markets face different governance issues depending on their investor mix and concentration.

Much of the fear-mongering about super fund investment in the ASX is that the large funds are becoming increasingly emboldened to use their individual and combined voting power to exert influence on company boards (particularly on ESG matters such as climate change).

However, the recently-revised G20/OECD Principles of Corporate Governance doesn’t see this as a bad thing. The principles say “institutional shareholders, should be allowed to consult with each other on issues concerning their basic shareholder rights as defined in the principles, subject to exceptions to prevent abuse”.

The OECD says it has long been recognised that in companies with dispersed ownership there is an “agency issue” where the interests of a company’s shareholders may not be sufficiently aligned with the interests of management and where shareholders do not have the resources to address this.

To overcome this asymmetry, the principles say institutional shareholders “should be allowed, and even encouraged to co-operate and co-ordinate their actions in nominating and electing board members, placing proposals on the agenda, and holding discussions directly with a company in order to improve its corporate governance, subject to shareholders’ compliance with applicable law, including, for example, beneficial ownership reporting requirements”.

Unsubstantiated fears

There is no doubt super fund investment in Australian listed equities is significant, but there is nothing worrisome about it.

The rather bizarre 2022 Report on the implications of common ownership and capital concentration in Australia prepared by the House of Representatives Standing Committee on Economics tried to stoke fears that if a large super fund simultaneously held shares in competing firms – say, in a few banks or a few retailers – they would be tempted to stifle industry competition and thus hurt bank customers and retail shoppers.

Despite being grilled by the committee, the ACCC, APRA and ASIC all said there was no evidence of this.

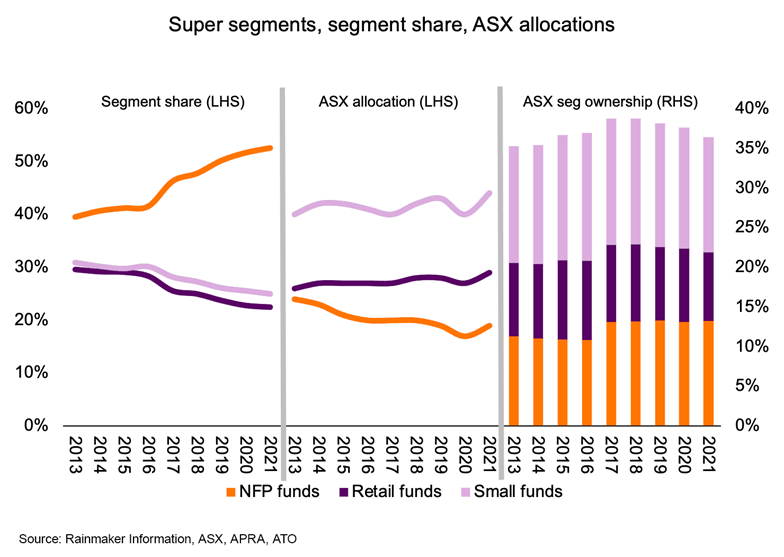

According to research house Rainmaker, super funds own about 38 per cent of the Australian bourse and this is expected to only grow to 41 per cent by 2030. Back in 2019 Deloitte was predicting super funds would own more than 60 per cent of the ASX by 2040. However Deloitte has since revised its forecast to only 43 per cent.

Data also suggests super fund ownership of the ASX has been levelling off. And while industry super funds have been successful in building their share of the total super fund pie, their percentage allocation to the ASX has been drifting downwards and their total ownership of the ASX would be under 15 per cent.

While money may be pouring into superannuation funds – and the size of the sector may be much larger than the ASX’s market capitalisation, the fear mongers prefer to overlook that Australian super funds only invest a portion of this in the local stock market.

While money may be pouring into superannuation funds – and the size of the sector may be much larger than the ASX’s market capitalisation, the fear mongers prefer to overlook that Australian super funds only invest a portion of this in the local stock market.

Super funds are increasingly investing in global equities and unlisted assets overseas. For example, member assets at AustralianSuper should grow by more than $200 billion over the next four to five years but around seven out of 10 new dollars invested will likely be invested overseas.

Super funds are also diversifying away from the ASX because there are limited new investment opportunities. In 2023, there was no growth in the ASX’s market capitalisation. There were few new major listings and with a number of mergers and de-listings there was an overall fall in the number of listed companies. The ASX also offers limited exposure to the clean energy transition and climate solutions.

Given the attacks on them, Australia’s super funds could no doubt empathise with Shelley’s monster, who tells a blind man that his life has been “in some degree beneficial; but a fatal prejudice clouds their eyes, and where they ought to see a feeling and kind friend, they behold only a detestable monster.”

The man replies, “that is indeed unfortunate; but if you are really blameless, cannot you undeceive them?”

Perhaps a job here for the new Super Members Council of Australia.

Leave a Comment

You must be logged in to post a comment.