In this article we review the APRA data on fund membership characteristics focusing on account numbers, account size, age and gender. The large dispersion across funds along these dimensions creates fascinating challenges for funds, service providers, policymakers and regulators.

Our analysis draws on APRA fund datasets, where we aggregate the data at an entity level and account for announced mergers.

Account dynamics

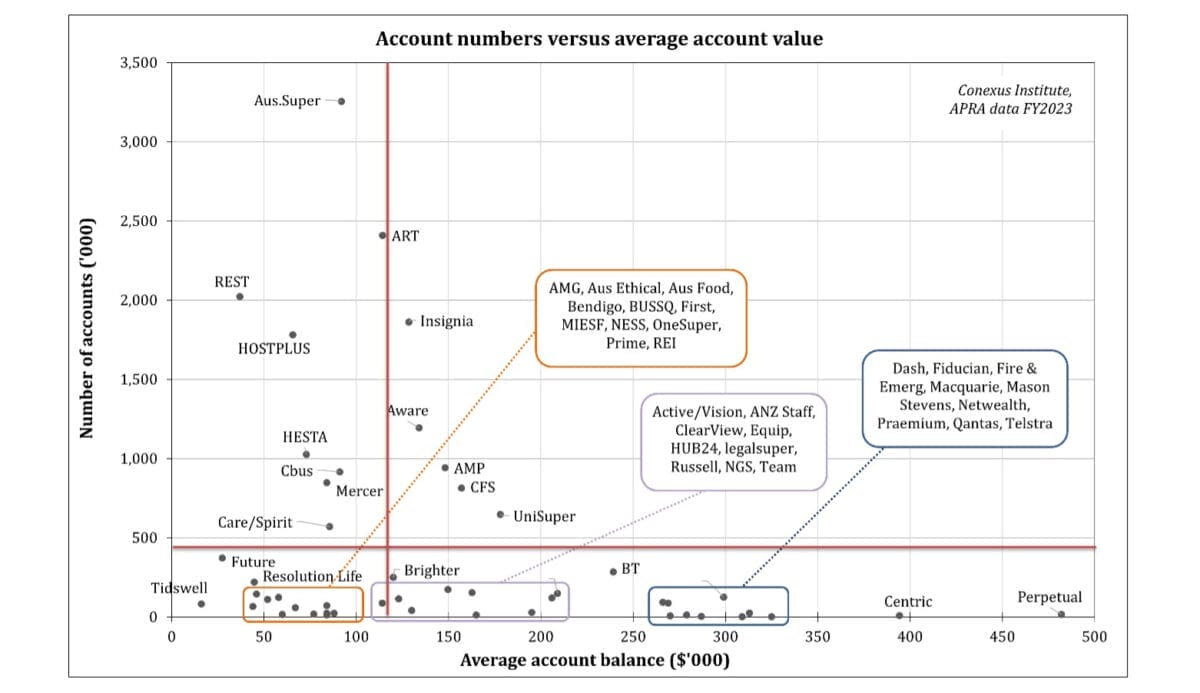

We first examine funds along the two dimensions of number of accounts and average account balance. The figure below highlights the sizeable dispersion that exists.

The red lines represent averages. The average super fund has 443,000 accounts and the average account balance is about $117,000. Focusing on the intersection of the red lines reveals that no fund is anywhere near the average!

The chart raises two important challenges for the industry.

First, some funds face a sustainability challenge, namely those in the bottom left corner of the chart. Funds in this zone need a strategy for growing account numbers, or member balances, or both. Many of these funds are in the ‘dangerous Q4’ part of our size / growth sustainability chart. Others are in the small ‘scale / high growth Q1’ part of the chart, notably certain retail platforms and sustainability-focused groups.

The second challenge is how trustees determine an appropriate balance between fixed and account balance-based administration fees. Account-based fees introduce a member cross-subsidisation challenge, whereby higher-balance members partly fund the services provided to lower-balance members.

Further complication is added by the Your Future, Your Super performance test. The use of a $50,000 balance to create administration fee benchmarks incentivises charging a lower fixed fee and loading up on the account-based fee notwithstanding the cross-subsidisation implications.

A snapshot of age and gender dynamics

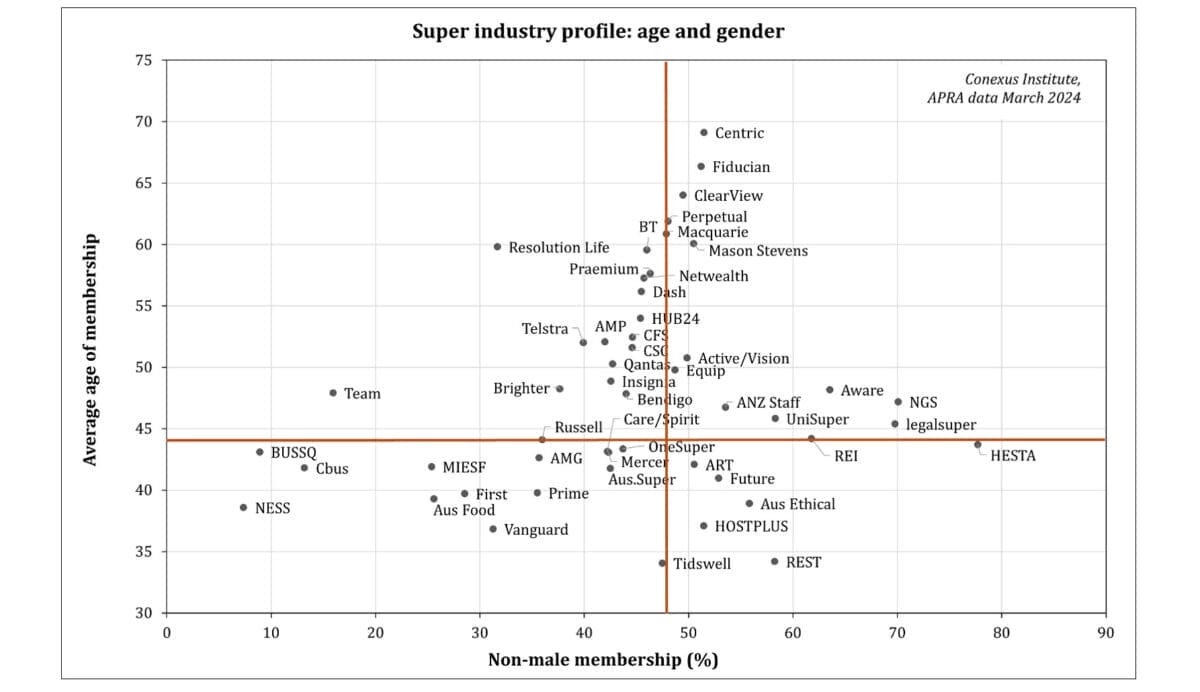

The chart below details the age and gender spectrum for the industry. The red lines represent industry averages. We estimate that super fund members have an average age of 44 with a mean non-male representation of around 48 per cent.

A range of factors explain much of the large dispersion evident in the chart above. Industry is influential. Some industries, like retail and hospitality, lend themselves to a younger workforce (as experienced by REST and Hostplus). Industry is also a driver of gender representation. NESS Super (electricity sector), CBUS and BUSSQ (construction) and Team (mining and transportation) have a male dominated membership. HESTA (healthcare) stands out as a fund with large non-male representation.

Another factor is engagement models. Some funds target specific membership cohorts. Examples of funds targeting younger members include Guild Super (largely young females, but has merged into Future Super), and Tidswell (which consolidated Spaceship Super). Meanwhile some thematic offerings such as climate and sustainability have resonated with younger cohorts. Australian Ethical is a good example.

A third factor is the role of financial advice. People who are advised by a financial planner are often older and have higher total wealth and larger super balances.

Financial advice explains why the top of the above chart (i.e. funds with an older membership) is dominated by many of the platform funds designed to service advisers including vertically integrated advice groups (such as Centric and Fiducian). It also explains the presence of many of these groups amongst the higher balance cohort in the first chart.

The dispersion in demographics across funds creates interesting challenges. One is engagement and communication. Here, funds need to consider whether to tailor their approach to match specific characteristics of their membership or cater to a broader audience.

The fascinating strategy of branding

Brand strategy is one fascinating challenge. Can (or should) funds with specific membership characteristics develop a brand suitable for a public offer marketplace? How many brand elements – such as age, gender, sustainability, etc. – can a mainstream brand incorporate before it becomes undifferentiated?

Cross-subsidisation also rears its head again as a challenge for fund trustees. Demographic-based cross-subsidisation challenges relate to the features and pricing of various services, and prioritisation decisions around the spending on projects.

There may be instances where one generation of members benefits at a cost to another generation. A prominent example is the design of insurance offerings, where there are pricing and pooling considerations.

Another example is the development of retirement income strategies and related services. Older members benefit immediately from the potentially large expense, while younger members will need to wait decades to realise benefits.

The Retirement Income Covenant requires every fund to develop a retirement income strategy to service the needs of their retired and retiring members.

However, the demographics of funds differ significantly, with some having limited members and assets in the retirement zone. These funds face a weaker case for committing resources and effort to retirement. This raises the risk of significant dispersion in the quality of retirement offerings, with some retiring members getting neither the guidance nor a solution that is suitable for their needs.

Leave a Comment

You must be logged in to post a comment.