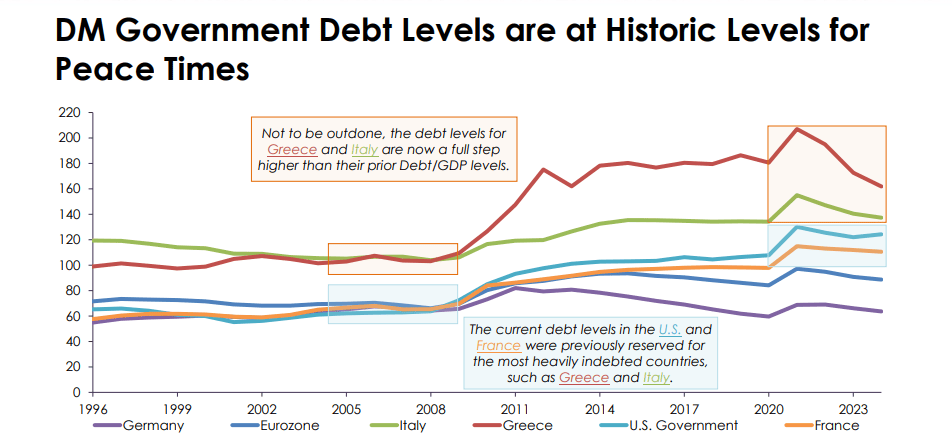

Concerns around global governments running on unprecedented debt levels have been well-documented, but PGIM’s top fixed income strategist said this new reality has both good and bad news for bond investors.

The asset manager’s chief investment strategist and head of global bonds, Robert Tipp, said countries historically with less debt, like US and France, now have a debt-to-GDP level previously seen only in Greece and Italy during the European sovereign crisis, while the latter two are becoming even further indebted.

“Everybody has now stepped up… it’s happened all around the world,” he told the Investment Magazine Fiduciary Investors Symposium in Healesville, Victoria.

Tipp said the good news is investors have been able to capture a lot of the higher rate of interest especially from developed bond markets with high debt burdens but low risk of defaults. But the bad news is that there are huge varieties and uncertainties between different governments’ economic approaches.

“The thing that that I’ve seen across developed countries and emerging market countries, the critical difference is does the government go out of its way to destroy the economy through corruption, protectionism, [and] ruin its domestic economy at which point it can’t support anything and everything collapses?” Tipp said.

“That would be the last 115 years in Argentina.

“A leading country, [but] they ruined the economy. They get it to a place where there is not any level of the currency at which – with the policies they had until recently – they could possibly support themselves.”

But Tipp said he does not have similar concerns for the US.

“There are two major markets where you can deploy a lot of money across a lot of sectors – US and Europe – and we’re way ahead of Europe, [in] trading around the clock [and] in size,” he said.

“I think DM economies are okay with this [debt level]. It is problematic, and as we saw with the European sovereign crisis, if countries are not careful, they can get into trouble. But right now, we’re at a relative sweet spot.”

Divergent outlook

Investors are also grappling with the big theme of varied inflation outlooks between countries. Tipp said factors that will drive inflation down or further up are at play simultaneously.

Forces that will keep inflation higher include workers continuing to want to claw back their real income growth and argue for ongoing wage-price tension; while economic protectionism such as tariffs may also boost inflation.

But Tipp said he believes the elements that will likely keep inflation down are longer-term drivers.

“This is a world of excess capacity, looking across Latin America, Africa and Northern Europe,” he said.

“The other thing that is important is prices are high. If you look at the trend in something like automobile prices in the United States, they have fallen 25 per cent for used car prices by one index, [but] they’re still 20 per cent above the trend that they would have been on pre-Covid.

“Once you get prices up at these levels, competitive markets have a tendency to bring them down.”

The third downward pressure on inflation is immigration, which is one element having different effects on Australia compared to other developed markets. Elsewhere, immigration creates labour supply and little demand in the economy in early generations, but that is not the case in Australia.

“A lot of people here come in, they go to university and end up in jobs, and the immigration here is massive, and so it is a lot of demand,” Tipp said.

“That creates these pressures, the structure of the real estate market creates a very high cost of living. So it’s an incredibly difficult situation.”

While central banks in the rest of the world have moved to cut interest rates, the Reserve Bank of Australia is expected to hold its current policy position until at least February 2025.

“The central bankers cannot solve all the problems. I’m not sure anybody really can, and what I’m referring to is the per capita problem,” Tipp said.

“There’s a really high population growth, and you don’t have per capita income growth, and then most places have widening inequality, which means, for half the people, it’s lousy per capita income growth.

“If they [the RBA] cut rates to boost growth, then they’re going to boost the housing prices and exacerbate the problems, and yet you have the immigration, and you have on-the- ground inflation. That’s why they’re at a different point in the cycle.

“The problems here, compared to a lot of DM places, are great problems to have, but it is tough.”

Leave a Comment

You must be logged in to post a comment.