The Magnificent Seven is a catchy moniker but investors have been warned that not all of them will live up to the name. In fact, some active equity shops are ready to pounce on the non-discerning market by gaining exposure to the ‘Formidable Two’ – best of the best names in the Magnificent Seven that will likely alone outperform the group.

For the Franklin Templeton-owned Martin Currie, the Formidable Two is currently Nvidia and Microsoft, but Apple and Meta are both runners-up for the title.

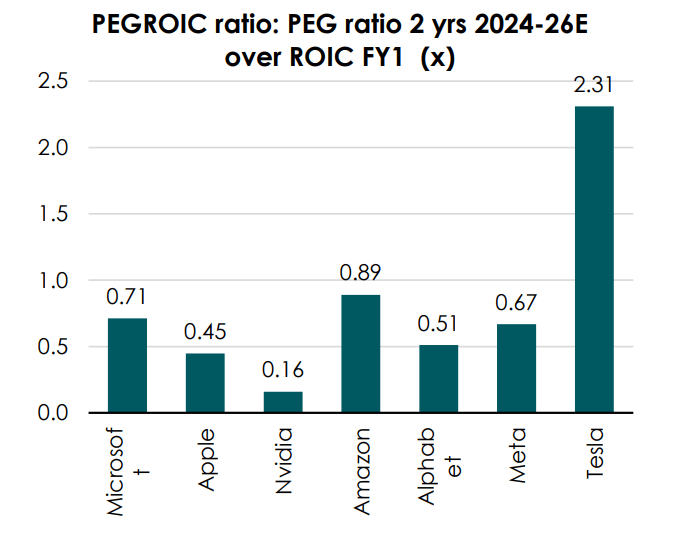

Martin Currie head of global long-term unconstrained Zehrid Osmani said the key metric is the price/earnings to growth to return on invested capital (PEG-ROIC) ratio, which marries the three crucial factors of valuation, earnings growth, and ROIC profiles.

“Nvidia still appears as [having] outstanding value across the three measures. Apple is actually cheap on that measure, and that’s because Apple’s got this outstanding 60 per cent ROIC,” Osmani told the Investment Magazine Fiduciary Investors Symposium in Healesville, Victoria.

“So we sometimes look at Apple as a staple, effectively, with a very strong return on invested capital that can compound over time, if you think that they can sustain that competitive advantage and market positioning that they have.

“Tesla [is] expensive still. And then the other ones are in the range that you would need to take a view on whether that range is going to improve or whether that’s going to decline over time.”

Breaking the spell

Osmani said return of the Magnificent Seven over the past 18 months has accounted for 51 per cent of the MSCI US index, and 34 per cent of the MSCI ACWI index.

“In history, when the market has become so concentrated, it’s tended to then lead to a period of underperformance for that basket because of the law of big numbers,” he said.

“But what’s interesting on this occasion with the Mag Seven is that that outperformance, to some extent, has been supported by earnings momentum.

“When you look at the growth profile of these businesses, yes, they could be challenged on the go-forward basis, but they’re not poor growth profiles – over 10 per cent growth and on the bottom-line basis, is actually very attractive.”

Still, the concentration is making active managers’ jobs harder, and how to break the spell of the Magnificent Seven is also a top concern for asset owners who are handing out the mandates.

Capital allocators can choose to neutralise the Magnificent Seven and use skilled managers to find alpha in the rest of the market, or they can bet on specialist managers who can meaningly outperform within the Magnificent Seven, Osmani said.

“You [can] try and pick the two best or the three best out of the seven based on fundamental assessment, or it can be some managers that are skilled at identifying trading ranges,” he said.

“There’s probably a good opportunity in the very liquid parts of the market to have an element of trading ranges. So if you can appoint some managers that can arbitrage between the seven – and it can be quite rapid arbitrage at times, but so be it – that can again deliver that excess return that you might need in your plans.”

However, while investors can have the investment case down pat, some other forms of risk on the Magnificent Seven are harder to quantify – most notably potential regulatory actions taken against the tech companies when they reach a quasi-monopoly status, Osmani said.

The most prominent case is Alphabet’s Google, which has been entangled in an antitrust lawsuit with the U.S. Department of Justice since 2020. In October, US federal judge Amit Mehta ruled that Google is a “monopolist” in the search and advertising market, raising fears that a breakup of its search business is on the cards. Specific actions towards the company have yet to be announced and Google said it will appeal the ruling.

“If you get a forced breakup of their business, and yes, it can still be valued in the assets, but it’s very difficult to estimate it,” Osmani said.

Leave a Comment

You must be logged in to post a comment.