It is often assumed that financial markets will recover from sell-offs to deliver reasonable real returns in the fullness of time. What if this doesn’t occur?

We explore this risk in a two-part series. Our first article overviewed Part A (full paper here), which addressed the likelihood of super funds delivering negative real returns spanning a decade or so. This article covers Part B (full paper here) considering the potential implications and what super funds might do to prepare. A seven-page summary covering both parts is available here.

Context matters

The context in which market weakness occurs matters. One consideration is ‘shape’ — the magnitude and pattern by which weakness unfolds. A 10-year span of negative real returns could arrive as a sharp initial sell-off followed by recovery, a slow drip of persistent weakness, or some other combination. Although the net loss of wealth over a given period may be similar, the behavioural impacts, potential for contagion and implications for rebalancing can differ.

Even more important are the underlying causes and any coinciding developments impacting the economy, asset markets and fund members. This can bear on scope to diversify losses, liquidity available to accommodate asset sales, the pain being felt outside of super, and potential for feedback effects. Widespread job losses, for example, may reduce net contributions and cause members under financial strain to seek to access their super.

It is entirely possible that several adverse developments could coalesce into a scenario with wide-ranging implications. Market weakness is more likely than not to occur in the context of broader stress across economies and asset markets, or under elevated inflation — with its own implications. A wide lens is required.

Implications across six areas

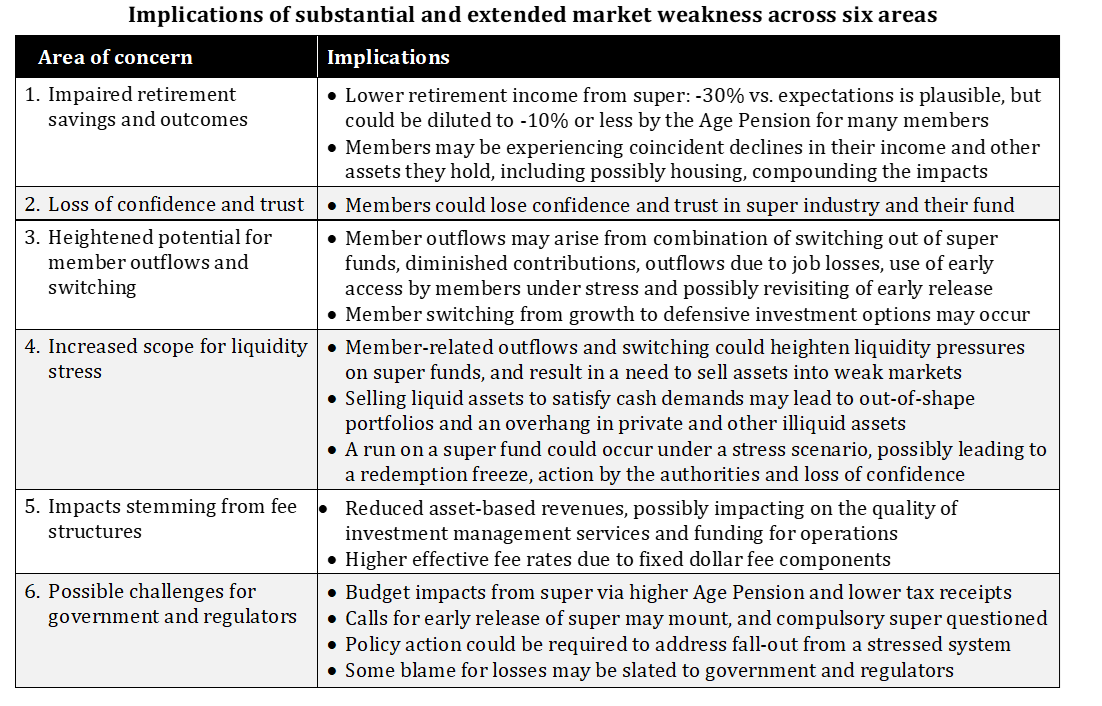

We arranged our discussion of implications along the lines of six broad areas. These are summarised in the table below, followed by a focus on selected elements.

Retirement outcomes

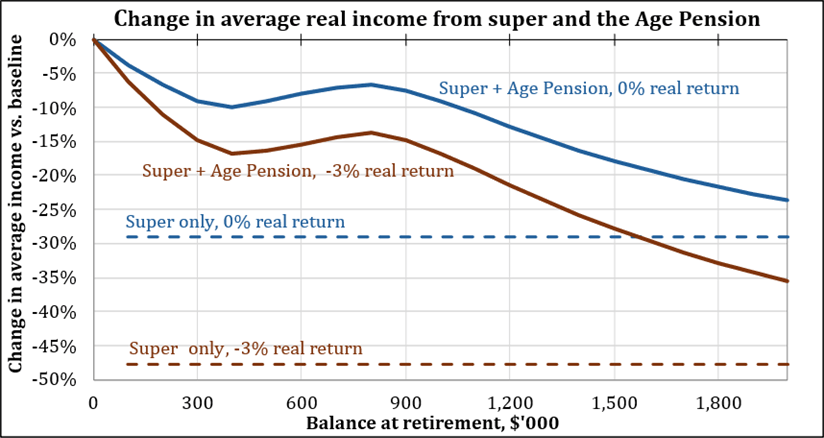

Our modelling indicates that 0 per cent real returns over 10 years could reduce average real income from super by around −30 per cent compared to a baseline of +3 per cent real returns. A fixed drawdown amount calibrated to last until age 92 under +3 per cent returns may be exhausted about eight years earlier at around age 84.

These declines are substantially diluted once the Age Pension is included, which raises the income base and provides additional income through the means test. The estimated income decline including the Age Pension falls to below −10 per cent at balances under $1 million — the range covering most members.

Confidence and trust

An extended period of poor returns could undermine confidence in super, which has already suffered some damage from operational issues. Members who have ‘stayed the course’ at their fund’s urging and then experienced years of poor returns may become disillusioned — with their fund, with regulators, and with the compulsory super system itself.

Some may respond by switching away from APRA-regulated funds or into defensive investment options at an inopportune time, to their own detriment, while creating liquidity and portfolio management challenges for funds. In a situation involving serious loss of confidence, a run on a fund cannot be dismissed.

Government and regulators

We highlight two implications. First are budget impacts. Market weakness tends to occur when government finances are already under pressure, and super can add to the pressure through higher Age Pension payments and lower super-related tax receipts.

Indicative estimates suggest 0 per cent real returns over the next decade could increase Age Pension costs by around $17 billion or 0.46 per cent of GDP (rising to $34 billion or 0.90 per cent of GDP under −3 per cent real returns) — a significant uplift on projections that place the Age Pension at approximately 2.2 per cent of GDP in 10 years.

Second, poor returns amid broader stress on households could generate calls for early release of super (‘people need their money now, not later’), which could prove politically attractive and difficult to resist.

Preparing for the possibility

Super funds might take three types of actions to prepare for the possibility of market weakness:

(1) Aim to anticipate or take protection against market declines. Anticipating declines is difficult, while taking protection runs into the problem that removing risk can impair returns.

(2) Build resilience – This entails managing exposure to key risks to limit the downside and enhancing flexibility to respond.

(3) Communicate to modulate expectations – Funds should foster an understanding that higher returns bring the prospect of better outcomes but there is always risk. Giving members the impression that growth assets are virtually certain to deliver solid long-run returns places the industry in a vulnerable position if that proves not to be the case.

Two key messages

We emphasise two key messages. First, the potential implications of significant market weakness should not be viewed in isolation but rather in the context of what else may be going on at the time. A wide lens is needed.

Second, negative real returns spanning a decade or more can happen, and the industry should prepare accordingly. The assumption that markets will always recover in a timely manner seems made too readily. We suggest dropping this as the working assumption and focus instead on portfolio resilience and clear communication, including conveying to members that solid long-term returns may be likely but are not guaranteed.

*The Conexus Institute is a not-for-profit think-tank philanthropically funeded by Conexus Financial, the publisher of Investment Magazine.

The Conexus Institute will offer an in-depth discussion of the research at the Fiduciary Investors Symposium NSW, to be held between 12-14 May in the Blue Mountains. Register to attend the event here.

Leave a Comment

You must be logged in to post a comment.