Early last year we released a major research piece titled Systemic impacts of ‘big super’ (full paper and summary version). We concluded that, on balance, super is beneficial. Among the sources of systemic risk we highlight, two stand out: a sustained period of market weakness, and limitations in the industry’s operational infrastructure, i.e. systems and processes.

Our new research explores the first risk of sustained market weakness. The backdrop is a system where growth asset exposure is approaching 75 per cent for APRA-regulated funds. While justifiable as more likely than not to generate better long-term member outcomes, it leaves the industry and members exposed to returns turning out to be poor over an extended period.

We examine this risk in a two-part series. This article overviews Part A (found here), which addresses the likelihood of ‘substantial and extended weakness’ in markets framed as negative real returns spanning a decade or so. Part B, considering the potential implications and what super funds might do to prepare, will be covered in a future article. A seven-page summary covering both parts is found here.

Precedent and probabilities

Extended periods of market weakness are not as rare as often thought. The historical run rate for negative 10-year real returns sits above 10 per cent even in US financial markets. Nearly every country has suffered a major decline in their markets at some stage. Japanese equities took over 30-years to reclaim the asset bubble peak of 1989.

World equities delivered negative real returns spanning over 10-years both during the stagflation period of the 1970s through to the early 1980s and again following the bursting of the tech bubble in 2000 where the initial recovery from the tech wreck was followed up by the GFC.

We attach a notional 20 per cent probability to super funds delivering negative real returns over a decade or so: higher than the historical run rate in recognition of some vulnerabilities and risk that could come to bear.

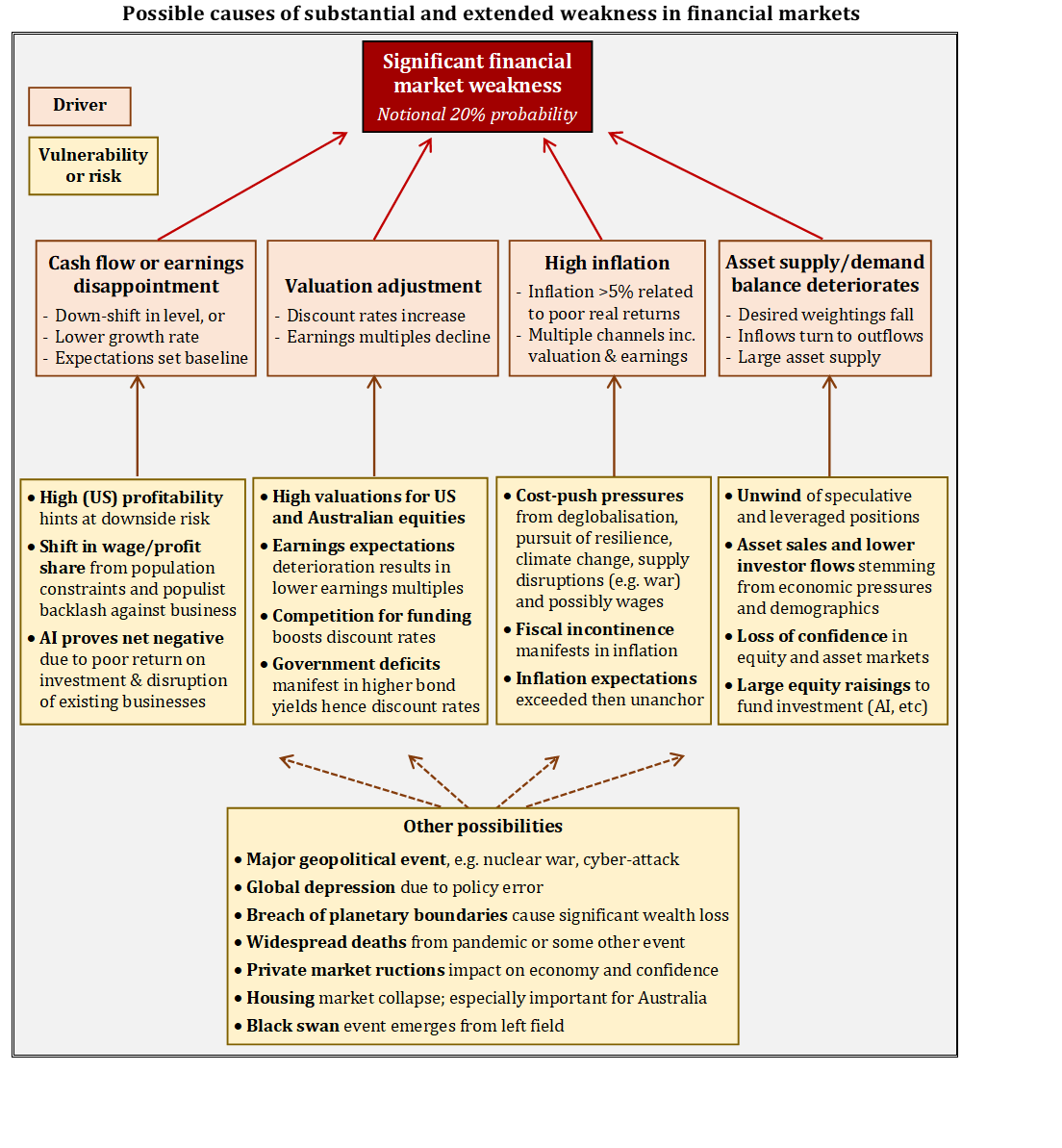

Possible causes

The diagram below summarises the possible causes of poor returns comprising a set of four drivers coupled with a range of vulnerabilities and risks that could impact on returns through the drivers.

The four drivers amount to a framework for thinking about market risk. They include cash flows and earnings, how those cash flows and earnings are valued, inflation, and asset supply/demand. Developments need to have a significantly adverse impact through at least one if not multiple drivers for poor returns to be delivered.

Current vulnerabilities and risks are listed at the bottom. These should be considered as possibilities rather than forecasted events. The point is that all are feasible and a number could coalesce into an impactful scenario for the economy, financial markets and thus super fund returns.

Some things to focus on

We selectively highlight four items that are worthy of attention:

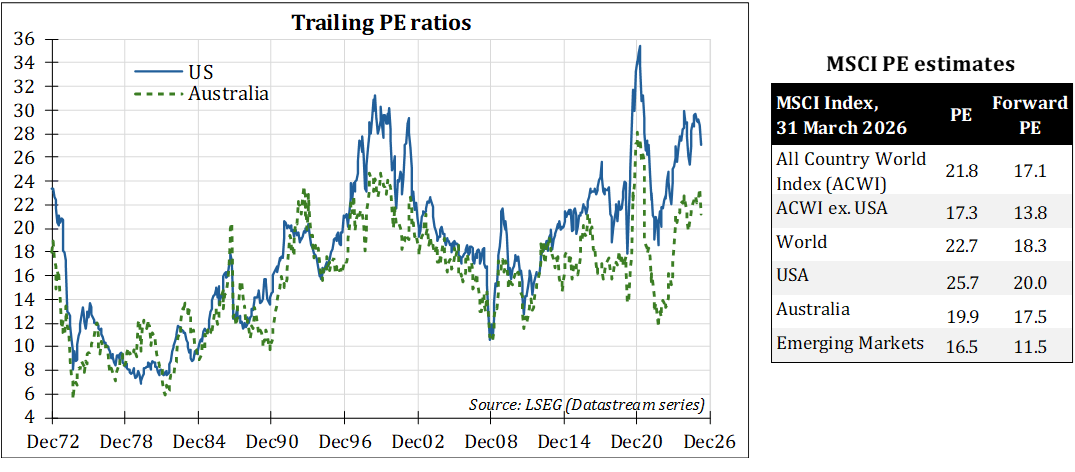

- US and Australian equity valuations – Both US and Australian equities trade on relatively high PE multiples (see exhibits below), with Australia expensive versus overseas counterparts (the banks are a stand-out). These two markets comprised around 22 per cent and 24 per cent respectively (total 46 per cent) of APRA-regulated fund portfolios as of December 2025. All example episodes of extended poor returns highlighted in Part A entail shifts from very high to very low PE multiples, underlining how starting valuations matter to downside potential.

- Sustainability of high US profitability – US profitability is at or near historic highs on many measures. What if this proves unsustainable, and the realisation coincides with a PE de-rating? We calculate that US return on equity and PE jointly reverting to their historical means could manifest in a -46% price adjustment.

- Inflation – High inflation especially over 5% has historically been associated with poor real returns. Markets do not appear priced for a structural rise in inflation. However, there are a number of ways that this might occur including various pressures on efficiency and productivity, supply disruptions, wage increases, monetisation of government debt, and an unanchoring of inflation expectations.

- Wage/profit share – A shift in the wage/profit share could have detrimental impacts on corporate earnings and inflation. Pressures may arise from declining workforces due to aging demographics and lower immigration and populist governments supporting higher wages to curry favour with voters.

Sources of resilience

There are ALWAYS things to worry about, yet in most cases markets have been able to take adverse developments on the chin to deliver solid returns over the long run. Potential sources of resilience include:

- Markets are priced to deliver positive real returns, even if lower than average. Things need to go meaningfully wrong to deliver negative real returns over extended periods such as 10-years.

- Markets appear expensive in pockets but not universally.

- The A$ might buffer returns on unhedged overseas assets in a stress scenario.

- Authorities may come to the rescue (yet again), i.e. the ‘Fed put’.

- Profitability might remain high due to monopolistic power in key sectors, lack of worker bargaining power, and corporates influencing the political process.

- AI could lead to a productivity miracle and major new growth sources. (Overall we are ambivalent over AI turning out positive or negative for markets.)

- There are currently few signs of a shift in the supportive supply/demand balance for equities.

- Never write off human ingenuity and desire to grow as fuel for upward momentum.

Final reflections

Our aim is not to paint a pessimistic outlook for financial markets and hence super fund returns. Rather, we want to make the point that significant weakness over an extended period such as a decade is possible. Our plea is that this possibility be recognised, and to avoid operating on the assumption it won’t happen.

Leave a Comment

You must be logged in to post a comment.