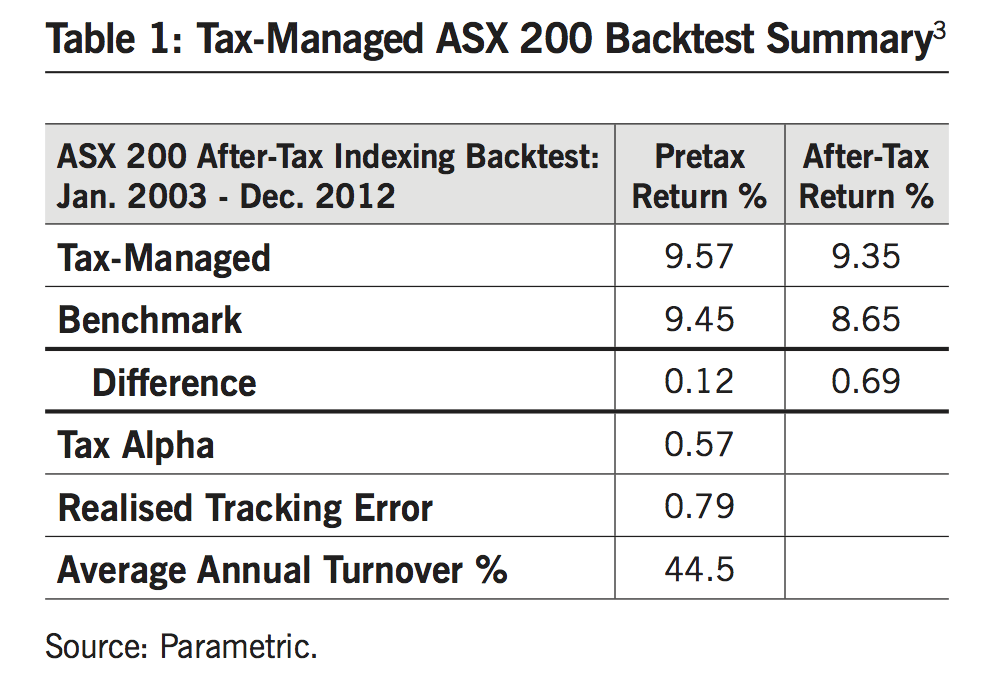

Active tax management can be used to enhance after-tax returns of indexed Australian and international equity portfolios for superannuation funds. The systematic and prudent implementation of tactics such as capital-gains/loss management and holding-period management can add real after-tax value. Simulations and back tests carried out by Parametric consistently demonstrate added value in the range of 30bps to 90bps of after-tax alpha on an annual basis.

With the increasing industry focus on net (after-tax) returns and the expanding research, technology and investment capabilities to properly tax-managed portfolios, we believe that a standard low-tracking-error equity indexing strategy will materially cost members in long-term after-tax returns.

Whenever there is any type of portfolio transition – such as withdrawals, benchmark changes or any time assets are sold – these events need to be managed very carefully with respect to the taxation consequences.

A tax-managed portfolio is ideally placed to facilitate such portfolio changes in the most tax-efficient manner. Any fund that currently uses or is considering indexing of equity assets should, at a minimum, genuinely consider tax-managed indexing as an alternative strategy – particularly when after-tax returns matter most.

MySuper regulations require that fund trustees consider taxes and adopt an investment objective that is net of taxes. However, according to tax regulations, a strategy cannot have tax avoidance as its dominant purpose. Parametric has received guidance from PricewaterhouseCoopers that our process is not subject to the general income tax anti-avoidance rules contained with Part IVA of the Income Tax Assessment Act 1936.

| Day 2 newsletter from CMSF 2013 | |

| Day 1 newsletter from CMSF 2013 | |

Leave a Comment

You must be logged in to post a comment.