What should a super fund choose: low fees that attract and retain members, or higher fees strategies that regularly outperform and give members better returns? The latter appears to be more popular, but there are those in the industry who think this is an oversimplification of the debate.

The first point of consideration when choosing a super fund, the public is told by the Government on its Money Smart website, is the level of fees, with lower being better. This is putting those super funds with a higher level of fees at risk of losing existing members and not being able to attract new ones.

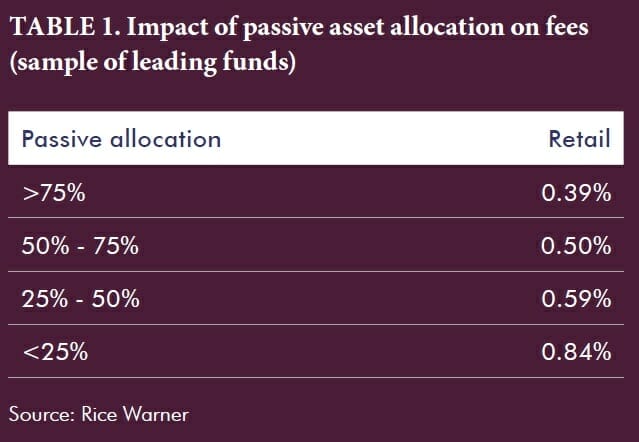

In its submission to the Financial Services Inquiry, Rice Warner states the headline fee of MySuper products has caused some funds to favour higher allocations to passive investing because of the associated lower level of fees (see Table 1, click to enlarge).

Its research indicates that:

- Many large industry funds are continuing to invest actively and have left their allocations unchanged

- However, some smaller industry funds have increased the proportion of passively managed assets in their portfolios to reduce costs

- Of a representative basket of leading commercial funds the average percentage of assets passively managed increased from 24.0 per cent in 2011 to 46.6 per cent in 2013

- Corporate and public sector funds have largely left their allocations unchanged.

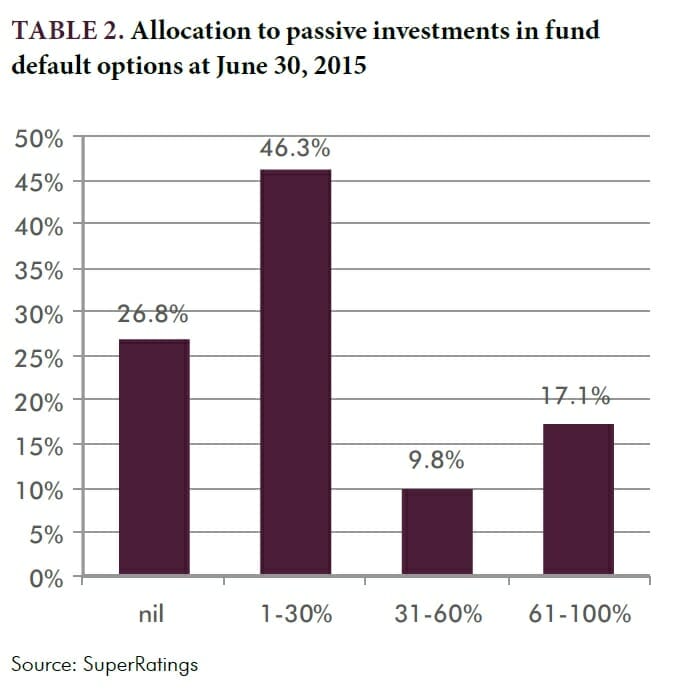

According to SuperRatings, only 17.1 per cent of super funds have a heavy (61 per cent to 100 per cent) allocation to passive, indicating that optimal net investment outcomes still holds sway across the industry (see Table 2, click to enlarge).

A range of views

This said, there are a range of strategies used in relations to the active and passive debate.

REST Super is ardent the focus should be on net benefit to members, something it doesn’t believe passive guarantees. Mercer believes the debate has been oversimplified and utilises systemic evidence in its decisions on portfolio construction. Meanwhile Aon Master Trust takes a pragmatic stance, operating around the median level for fees, while offering members a low-cost investment option should they desire it.

REST Super is ardent the focus should be on net benefit to members, something it doesn’t believe passive guarantees. Mercer believes the debate has been oversimplified and utilises systemic evidence in its decisions on portfolio construction. Meanwhile Aon Master Trust takes a pragmatic stance, operating around the median level for fees, while offering members a low-cost investment option should they desire it.

REST Super

Damian Hill, chief executive of REST Super, says the overall net return to members should be the focus.

Damian Hill, chief executive of REST Super, says the overall net return to members should be the focus.

“It should always be on net benefit to members. We are among a few trying to make sure this is the primary focus,” he says. “We have certainly made that comment to APRA, to make sure it does not become overly focused on low cost, which does not guarantee having the best member return.”

He adds the environment we are currently in is indicative of the need not to be passive, because of the recent falls in the equity markets.

“Active managers will have been holding cash up to around 15 per cent, a passive manager would not. This makes fundamental research more important in this environment than in the past.”

Mercer

Russell Clarke, senior partner and chief investment officer at Mercer, has been heading an in-depth research paper into passive and active management (due to be released next year) and says the debate needs to move beyond the simplistic notions that tend to get raised whenever the subject of cost or passive comes up.

“For most people it is a simple cost saving exercise or a philosophical exercise of ‘I don’t believe in active management, full stop,’ or ‘I don’t believe in active management in bonds because how could you possibly add value?’ That is far, far too simplistic and you need to look at the evidence to do it much more systemically.

“This is the part that may be missing for some – systemically looking at what the evidence says if you are going to decide with a certain fee budget what [allocation] is passive and what is active.

“I’m not sure that many people have really taken a good long, hard look at the evidence rather than using the conventional wisdom of where they should be.”

Mercer follows this systemic process through each area of the portfolio, acting on what the evidence tells it – whether active or passive has been successful in an asset class, or is likely to be successful going forward.

“We don’t try and be too philosophical and say we must have active in this area and we must have passive in this area, because quite often the evidence actually shows the opposite,” Clarke says.

For example, conventional wisdom says active emerging market equity mangers are a good investment option because there’s a lot of inefficient markets and therefore opportunities to add alpha, while active managers shouldn’t be used in global sovereign bonds because they’re really efficient.

Mercer’s evidence shows that while, as a group, active managers in emerging market equities will add value, the high fees associated with the managers means on a fee per unit of alpha basis, the proposition is not very attractive.

“When you look at global sovereign bonds you actually find the opposite. Global sovereign bond managers, as a group, often give quite decent alpha for the quite modest fees that they charge, which really bucks the conventional wisdom.

“And that has been our experience in our portfolio. We’ve had a lot of value in our global sovereign bond portfolio, in an alpha sense, and the fees are very low,” Clarke says.

He adds it can’t be a backward looking exercise. Mercer periodically updates the evidence to look at the environment going forward because there might be some particular reasons that managers, as a group, struggled in particular environment, or might have done well and that might not be the case going forward.

“You need to look at what the evidence has shown you historically and what the future environment might look like. When you marry those two together we then form some views whether this is a really fertile area for adding alpha per unit of fee.

“We then marry that with trying to optimise the overall cost of the portfolio. How it currently stands, and how to construct a portfolio at different price points.”

Aon Master Trust

In its consideration of the debate on fees, Aon Master Trust has decided on a “balanced approach” resulting in it being close to the median in terms of fee costs.

“We haven’t tried to drive fees down to try and compete on a pure fee basis because we don’t think this offers the best value to members,” says Janice Sengupta, chief investment officer and head at Aon Master Trust.

“We’re very conscious of fees, as the fund managers we work with can attest – that becomes a point in our negotiations.”

However, as part of a pragmatic strategy, Aon Master Trust has given its members a choice between active and passive options, so if fees are a member’s overriding concern they have access to an investment option that is cheap.

There are two avenues open to members wishing to pursue this route. They can use the passively managed funds through the main part of the fund’s menu – Vanguard is its index manager – or they can access exchange traded funds.

“We have constructed a menu where we have premixed funds in both flavours – active and passive – and the same with the sector options. For those individuals or advisors who might be serving as an intermediary for members [where] there might be a preference for a lower fee structure, or a lower MER from the manager, they have a choice of using those options,” Sengupta says.

Leave a Comment

You must be logged in to post a comment.