Ian Lundy, chief investment officer at RBF, has moved the Tasmanian super fund to a more conservative standing, focusing on operational efficiencies to improve performance. That said, some distinctive quirks remain.

Last year Tasmania had three super funds – now it has two, following the completion of the merger between Tasplan and Quadrant on November 30, 2015.

The other super fund, Retirement Benefit Fund (RBF) – which won Small Fund of the Year at the Conexus Financial Super Fund Awards 2015 – has been earmarked for a Tasmanian super merger too, but work on that is still in its early stages, according to its chief investment officer, Ian Lundy.

“It’s more complex than a normal merger as there is a third party involved – the Tasmanian government; that means there are more moving parts,” Lundy says, predicting the merger is unlikely to take place before late 2016.

However, RBF and Tasplan are already working closely together. “I wouldn’t say we are aligning our investment portfolios, but we are certainly discussing what we are doing in our portfolio, keeping in very regular contact,” Lundy says.

He adds that they are also assisting Tasplan in the areas in which RBF has expertise.

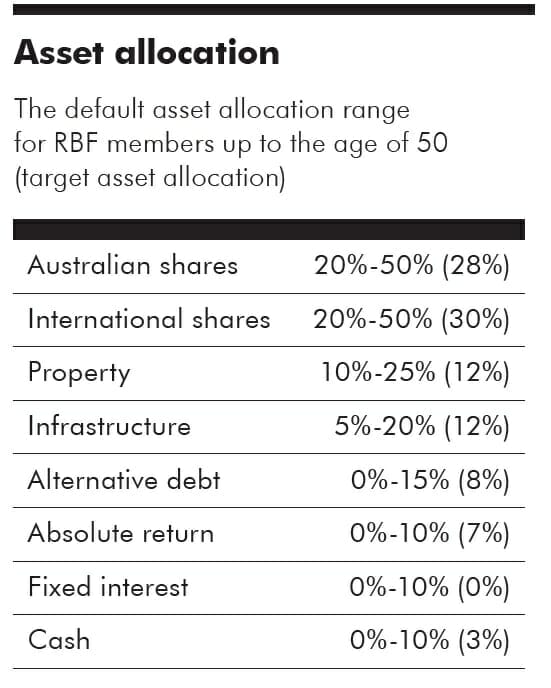

Since Lundy became chief investment officer five years ago, the portfolio at RBF has become more conservative, tilting from high-risk to mid-risk assets reflecting one of RBF’s investments principles: to provide a degree of downside protection. This has manifested, in part, as a shift from equity to infrastructure and property. He has also reduced the exposure to fixed interest and moved some assets to cash.

“We’re positioned relatively conservatively, and despite that we’ve kept up with other funds who had much higher growth asset allocations in what has been a fairly bull market until recently,” Lundy says.

Australian equities were completely “rejigged” in 2012 removing overlap between managers, moving large caps to more of an index plus focus, and the super fund became increasingly active in medium and small caps.

Rationalising the strategy, Lundy says: “Some parts of the market are more efficient than others, so why not dedicate your fee budget to the least efficient parts where you can add the most value, and for the more efficient parts look at something less active and cheaper?”

A lot of work Lundy has done has been on continuous improvement of the operational side of investments, improving governance and efficiency while reducing risk and costs. While been a steady of stream of improvements.

For instance, the fund moved from crediting rates to unit pricing in 2013, introduced a default lifecycle product in 2014 and insourced the management of cash in 2015.

JANA, the funds consultant, has played an integral role in these investment strategies, sitting down each quarter with Lundy to plan papers for the next investment-focused board meeting.

Together they present a unified position to the board. For things like asset allocation Lundy relies heavily on them, for manager appointments JANA gives a shortlist with the final recommendation made by the internal investment team, while Lundy and his team handle day-to-day implementation internally.

Property

As part of its move to a conservative strategy RBF has been shifting out of opportunistic property, as it did not fit with the aims of the fund.

“Property, for us, is a core part of the portfolio because it’s income generating, it’s stable. Opportunistic property didn’t fit that description, so we’ve slowly exited those investments and moved towards a very stable – I would even say boring – property portfolio.”

Direct property is one of three internally managed portfolios (the others being commercial mortgages and a direct cash portfolio launched six months ago to a large degree of success). Part of the direct property team’s role includes the refurbishment of existing buildings owned by the super fund.

Work has just been completed on one property at 144 Macquarie Street in Hobart, which has made the building more efficient and improved the energy rating. The goal is to achieve a four-and-a- half star (out of six) National Australian Built Environment Rating System (NABERS) rating from the government, which can be assessed once there is 12 months of energy consumption data.

One example of savings was replacing the 40-year-old lift motors, which reduced energy consumption by 85 per cent.

“We have also upgraded air conditioning plant at two of our other buildings and one was recently awarded a four-and-a-half star rating. We are hoping all three of our buildings can achieve that once this [upgrade] process is finished. Direct property has been a very strong investment for us over a long period of time,” Lundy says.

Distinctively, RBF also internally manages a commercial mortgage strategy, as part of its fixed-interest portfolio.

Essentially, the fund lends money to owners of commercial properties (such as office buildings, shopping centres and hotels) who can offer a moderate to low valuation ratio and good cash flow generation. In each case, the internal team look for asset coverage and cash flow coverage. This portfolio has been going for approximately 20 years and the conservative lending strategy means it has never had a default where it has lost money.

“It’s one of those things that if we didn’t have it, we probably wouldn’t start doing it,” Lundy says. “But we do have it and it’s done very well over a long period of time. We have a very strong team managing the portfolio and we will maintain it.”

Absolute returns

When the fund is more adventurous, Lundy is employing complex strategies in absolute returns, as he sees strong opportunities in the space.

Specifically the fund is looking for strategies with higher alpha potential while giving downside protection against a major market correction and/or rising interest rates. The trade-off is more volatility, which has led Lundy to place the products into the diversified options, because they don’t easily stand alone.

“We call this asset pool absolute return, but I would almost prefer to call it “uncorrelated strategies” as, to me, it describes what we are looking for here. We are looking for strategies that are really uncorrelated to everything else. Not duration, not equity beta, but something else.”

As part of this, back in June 2015, RBF invested $100 million in the GAM Absolute Return Bond Defensive Fund. Lundy adds that in a low-return environment investors need to go looking for other sources of return and these products, based more on alpha and less on beta, are “really quite interesting”.

“We had some managers in the portfolio that probably had too much beta in the product; it’s meant to be uncorrelated. The idea is that you employ strategies that are uncorrelated but still generate really good returns, well above cash. The holy grail is to find strategies where the low correlation also holds when other markets fall.”

Costs

Like most in the industry, the important thing for Lundy is the return to members after fees and taxes, made even more pertinent by the low-return environment.

As well as looking for innovative strategies in places like absolute returns, Lundy has been working on how to bring fees down, with some success.

The base fee of the balanced option has been lowered by 12 basis points in the past five years. Lundy says this was achieved through a combination of restructuring asset classes (as some were more expensive than others), changing asset allocations and negotiating lower fees with managers.

So far this financial year, in his drive for efficiency, a further 1.4 basis points have been taken out at a fund level. Some of that has been from fees and some of it has been the “little costs” that sneak in. For example, Lundy has been changing the fund’s approach to foreign exchange transactions, which he says has saved a meaningful amount of dollars.

“Going back to absolute returns, the biggest fees we see, by a mile, are with absolute return managers. The fees are hard to justify. These people are not just well paid, they are really taking it too far.”

In Lundy’s opinion performance fees need to have an appropriate hurdle above cash before kicking in, as the risk profile is greater than cash.

“We need to be compensated for that, otherwise we are giving a free option to the manager,” he says. “Fees should depend on the capacity of the product and how labour intensive it is to run, but generally a lot of fees are still too high.”

Improving the industry

For Lundy, one of the most important things a chief investment officer can do for fund members – and an area where super funds need to make a greater effort – is ensuring good governance of external funds and investments, particularly in unlisted investments.

“One of our goals is to participate actively in every fund governance body that we can. Investor review committee, unitholder committee, boards of these investments, we have a goal to be in each of these and actively participate,” he says.

“We believe it’s one of the single biggest things you can do to improve returns for members. Particularly, I am thinking of unlisted property and unlisted infrastructure because a lot of these funds have material conflicts and related party transactions issues. You need to be there watching them closely and asking the right questions to make sure these funds are being managed for the benefit of the investors and not for the benefit of the fund manager. We’ve devoted a significant amount of resources to that as a fund.”

Leave a Comment

You must be logged in to post a comment.