The rivalry between retail and industry funds may make more headlines, but the biggest competitive threat to the non-profit superannuation sector remains the appeal of self-managed funds – particularly to members with higher balances. Some of the country’s biggest funds share how they are responding.

In the wake of harsh losses from the global financial crisis (GFC), Australia’s major superannuation funds saw an exodus of capital, as some of their most valuable members left to set up their own self-managed super funds (SMSFs).

That trend has now passed its peak, and a growing number of SMSF owners are returning to prudentially regulated funds. But the do-it-yourself sector remains a significant competitive threat to even the nation’s biggest and most sophisticated funds.

A growing body of research provides some insight into what motivates people to leave their default super fund and set up an SMSF, as well as the reasons a growing number then retrace their steps.

SMSFs can have between one and four members and are regulated by the Australian Taxation Office (ATO), while larger pooled funds are overseen primarily by the Australian Prudential Regulation Authority (APRA). An SMSF is more responsibility, but provides more flexibility.

Analysis by actuarial consulting firm Rice Warner shows that over the past five years, the growth in the number of new SMSFs has slowed. According to the latest ATO data, establishments peaked at 41,000 in 2012, and declined to 31,000 in 2016.

Investment Magazine canvassed a range of experts on what is bringing SMSF owners back to APRA-regulated funds. The consensus is that while some members have executed on a formal plan – using an SMSF for a specific investment purpose such as purchasing business premises or residential property – they are the minority. Most come back because their expectations have been dashed, often because the benefits of an SMSF were overstated or misrepresented

by their adviser, usually an accountant.

There is a clear link between the dissatisfaction among returning members and the size of the SMSF they operated. The smaller the fund the less satisfying the experience, which raises questions about the quality of advice they received in setting one up.

Do-it-yourself funds appeal to individuals who think they can do a better job of managing retirement savings than the big players.

The first edition of The SMSF Report, jointly published earlier this year by the SMSF Association and the Commonwealth Bank of Australia, shows that 59 per cent of SMSF owners said they set up their fund to achieve better investment returns, while 39 per cent wanted “to be more agile to take advantage of investment opportunities”, and 43 per cent wanted to cut costs. The emotional appeal of SMSFs to older members with higher balances is a particular challenge for industry funds. The number of individuals who leave industry funds each year to set up SMSFs is dwarfed by the number of members who leave to join retail super funds, but they have a disproportionate impact on the funds they leave behind.

Stemming the flow

A Rice Warner report found that only 6 per cent of all members who leave industry funds go to SMSFs, but they account for 22.5 per cent of the assets that leave – 3.5 times the value of funds taken by the 42 per cent of members who leave industry funds to go to retail funds.

It is not entirely clear why SMSF establishments have fallen from the peak of 2012, but Rice Warner notes that retail, industry and corporate super funds have all made “a significant effort to stem the leakage of assets to SMSFs over the last few years”.

“This includes member direct investment, improved advice models, reduced fees, transition-to-retirement accounts and hugely improved account-based pension offerings,” the Rice Warner report stated.

Anne Fuchs, Sunsuper’s general manager of advice and retail distribution, says the SMSF sector is still the $45 billion not-for-profit fund’s largest source of outflows. “If I think of historical roll-out trends, we had a lot of money go to retail funds, and that trend has pretty well stopped,” she says.

Fuchs says that when Sunsuper analyses rollovers into SMSFs, the quality and the motivation of the advice is sometimes questionable, particularly in relation to fund size. But Fuchs says SMSFs can work well when the right sort of individual sets one up with enough assets and full knowledge of the cost and effort involved.

Fuchs says if a member contacts Sunsuper about setting up an SMSF, the fund’s call-centre staff will explain the responsibilities of being a trustee – including the likely administrative workload and cost – before referring the member to the fund’s national panel of financial advisers. Better-informed members often decide not to leave.

Fuchs says Sunsuper recognises SMSFs meet a need that larger funds can’t satisfy for some members, but it is unlikely to develop new investment offerings to convince those members to stay.

“There’s a lot to be said, sometimes, for the power in saying no, recognising what you’re great at and what is your core business,” she says.

“We’re not trying to be all things to all people. That’s the power of our proposition.”

Members returning

Tim Anderson, executive manager of marketing and product for Unisuper, a $58 billion academic sector fund, says his fund did “a lot of research into the benefits of direct investment options a number of years back” to help address the peak in demand for SMSFs just after the GFC.

He says the cost to the fund couldn’t be justified, and “under the best-case scenario, we would hope to have retained a maximum of 50 per cent of the outflows to SMSFs”. The fund focused instead on improving general advice, personal financial advice, its contact centre, and its administration and digital channels.

Anderson says that as a result, outflows from Unisuper to SMSFs in 2016–17 were 32 per cent below the 2012 peak, and inflows to Unisuper from SMSFs increased 300 per cent in the last financial year.

Hostplus, the $24 billion industry fund for the sport and hospitality industries, is tackling the SMSF issue in a different way. The fund’s chief investment officer Sam Sicilia says it is developing options to lure SMSFs to Hostplus, to “invest directly and take advantage of the fund’s investment expertise and scale”.

“SMSFs have discovered that investing money is easy, but making a good return from their investments is very hard,” Sicilia says. SMSF trustees will get a better result by “using investment experts and holding them accountable for the service quality and the price paid, rather than DIY”.

“That’s what we do when we use a doctor, dentist, plumber or electrician,” Sicilia says. “Why is investing for retirement different?”

Analysis by Australia’s largest industry fund, the $110 billion AustralianSuper, suggests that the flow of members back into APRA-regulated funds has reached as much as a third of the number who depart to SMSFs each year.

Harder than it looks

The analysis shows about 65,000 members leave APRA-regulated funds each year to set up an SMSF, and take $15 billion with them. But the amount being rolled back into APRA-regulated funds has been increasing.In the 2013–14 financial year (the latest data analysed), rollovers from SMSFs into APRA-regulated funds exceeded $5 billion, from 20,000 members.

David Short, AustralianSuper’s head of customer analytics and insights, says that a majority of that fund’s returning members reported a poor SMSF experience.

As that realisation dawns, Short says, members are returning. In the past financial year about $480 million of assets left AustralianSuper headed to SMSFs, but about $405 million came in from SMSF members heading back into the fund.

A May 2016 white paper published by AustralianSuper, When the dream goes sour: SMSF members returning to APRA funds, found that in many cases SMSF members were sold an idea, “typically of geared real estate, usually by their accountant”.

“But most were never able to implement it, often because their balances were too small, something that should have been obvious from the start,” the report states. “They were left with a small SMSF, stuck in cash, with unsustainable costs.”

Short says that of members who returned to APRA funds after a dissatisfying SMSF experience, 40 per cent had received advice on how and when to set up their SMSF, typically from an accountant rather than a financial planner.

Less than 10 per cent of returning members who had a dissatisfying experience had received any advice at all.

“It suggests that people who are highly financially literate and know what they’re doing… had a long-term plan and executed that the way they wanted to,” Short says.

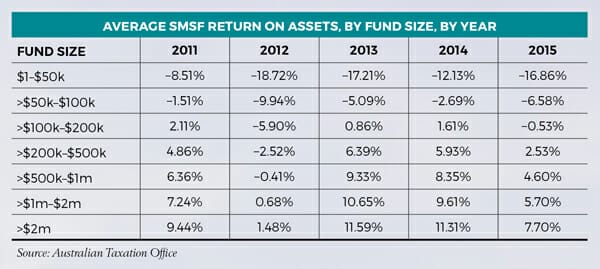

Doug McBirnie, a senior actuary with SMSF administration business Accurium, says a drop-off in performance – and hence a lower retirement income – isn’t necessarily a given for members who set up their own fund.

McBirnie says SMSF investment results can be distorted by the impact of establishment fees hitting returns in early years, and by fixed administration and operating costs, which hurt smaller funds disproportionately hard compared to larger funds that can absorb the expense. For that reason, the Australian Securities and Investments Commission (ASIC) suggests that SMSFs have assets of at least $200,000 from day one – or very shortly after establishment – in order to be viable. This recommendation is backed up by ATO data.

Right for some

Whatever the required minimum, it is undeniably important that members leaving APRA-regulated funds to set up SMSFs are fully aware of the potential costs involved. With full information, and when a sound investment plan is defined and executed well, even the competitors acknowledge that SMSFs are an important part of the full range of retirement savings options.

AustralianSuper’s Short says that if a member is “in a position where an SMSF is genuinely the best option for them in terms of their retirement planning, we are not going to actively try to suggest that’s not a direction they should go”.

Unisuper’s Anderson says SMSFs play an important role “for some members in the right context”.

“In the right scenarios we will recommend them via our financial advice channel. However, it’s really important that members understand the pros and cons, what they are getting into, the fees they will pay and the level of commitment required to manage one. They definitely don’t suit everyone, and education is critical.”

Leave a Comment

You must be logged in to post a comment.