ASFA has cast doubt around claims made in the Retirement Income Review (RIR) that many people are not spending down their retirement savings, being too frugal and preserving large account balances which are ultimately bequeathed. Here I present some basic modelling which further endorses the findings of the RIR while emphasising the need for better retirement solutions.

The Retirement Income Review explored this issue and considered a variety of research. It is a difficult area because the retirement system is not fully seasoned. Importantly some of the research available to them was longitudinal which means it tracked individuals through time. The issue identified, underspending in retirement resulting in a large bequest, is problematic for policymakers because the level of SG is a heated debate and savings in superannuation are heavily tax incentivised (for middle and high-income households). The RIR suggested that if better retirement products are available, supported by improved guidance along with greater awareness of the ‘social transfers’ in place to support them, then retirees may live less frugally in retirement.

ASFA’s research largely fails to track the path of spending and retirement balances through time, nor account for any sensible measures such as debt reduction at the point of retirement.

What is well-known (Igor Balnozan at UNSW has done some great research on this) is that many people draw down their account-based pension at minimum draw down rates. Some basic modelling based on this identifies that the end outcome would naturally be the outcomes noted in the RIR.

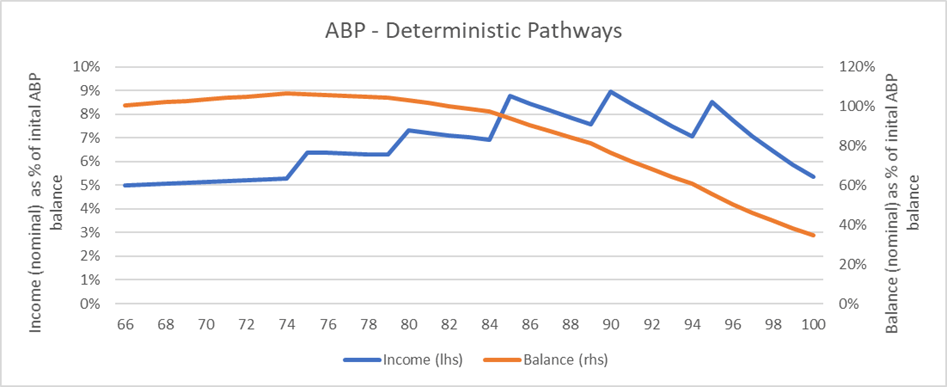

Consider an account which draws down at minimum drawdown rates and earns a constant 6 per cent nominal return. The chart below illustrates nominal income and balance as a percentage of starting balance through time.

The claims made in the RIR can be easily verified: if people are drawing down at minimum drawdown rates, then we can readily reconcile the high balances at death quoted by the RIR and politicians: see the orange line which links to the right-hand side axis.

There is another strange observation in this case study. Nominal income increases significantly as we age (until we are very old). This is due to the life expectancy probabilities incorporated into the design of minimum ABP drawdowns rather than what would be an appropriate consumption pattern for consumers.

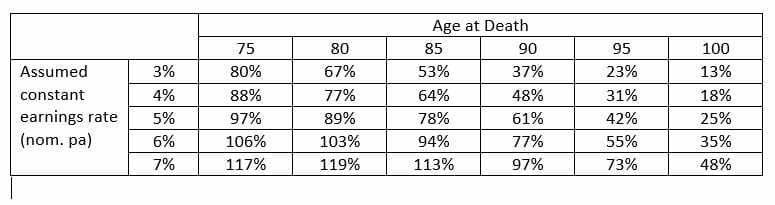

Let’s focus in on the issue that was capturing most of the headlines: balance at death. To explore further I consider different earnings rates. Each cell in the table below represents the percentage of initial retirement balance for a combination of assumed return and age at death.

The main observation to draw from the table is that even under lower return assumptions people who draw down at minimum drawdown rates are still likely to have sizable balances when they die.

Of course much more detail could be added to this analysis. For instance, we don’t do any stochastic modelling to consider the range of outcomes which acknowledges issues such as sequencing risk.

This little reality-checking project reinforces the findings on the RIR. You can link it back into the RIR’s SG recommendation if you like. But for me the primary reflection is the need for better retirement solutions which provide regular payments which last for life. Many people follow the ABP minimum drawdown rules but these aren’t a great guide to maximisation the retirement experience. The ABP drawdown rules incorporate a degree of personal risk management.

The need for personal risk management drops away in an environment where risks are pooled through better retirement solutions. The Retirement Income Covenant is on its way and that will hopefully bring with it pooled products that enable consumers to have more confidence in their retirement finances.

Leave a Comment

You must be logged in to post a comment.