The pathway forward for super funds in a Your Future Your Super world is challenging.

We’ve just finalised our research piece (available here) and on reflection we were a little too positive in our previous article (here).

The most significant negative impact of the flawed YFYS performance test is the way it will constrain the ability to construct portfolios to maximise member outcomes.

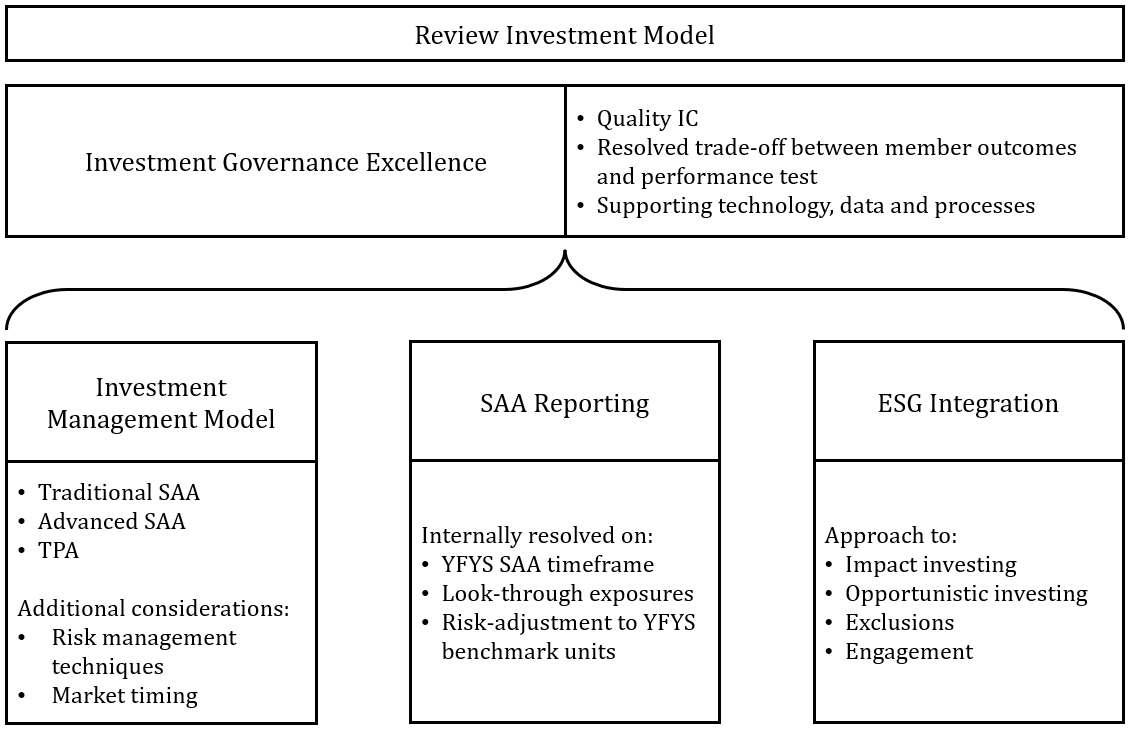

There are some positives: the most exciting aspect is that the investment governance of super funds will be sharper than it has ever been. Some funds will have never had such detailed investment discussions, and that will benefit outcomes.

Many funds will likely alter the way they report their SAA (strategic asset allocation). This could reduce the degree to which the constraints of the performance test impair the ability to manage for member outcomes.

Funds need to re-visit their approaches to managing portfolio risk. It may be that market timing becomes more common. Funds will also need to consider how they account for ESG issues in their investment strategy.

SAA reporting

Historically funds used SAA’s differently, dependent on their investment management model. Indeed, some investment approaches do not use an SAA at all (for example TPA – total portfolio approach). In a YFYS world the SAA is the foundation stone and will receive significant trustee attention.

Yet SAA is not particularly well-defined in regulations. We expect there will be three areas that funds look at closely:

- Timeframe of the SAA: timeframe is not formally defined beyond “long-term”, and any difference between current AA and SAA is penalised in the form of performance test tracking error. This creates an incentive for funds to shorten the time horizon of their reported SAAs.

- Look-through SAA: some funds are targeting asset class exposures and using alternative investment strategies to achieve that (which they can verify through their look-through reporting). This motivates funds to report the true asset class targets as their SAA, while their reported actual AA may list alternatives as discrete product exposures.

- Risk-scaled SAA: the situation may arise whereby funds are taking significantly different risk within an asset sector relative to the YFYS benchmark. This creates performance test tracking error. Funds may consider risk scaling their exposure into YFYS benchmark equivalent exposure (a common best practice risk management technique applied by many investment managers and investment banks).

During some initial socialising of this research a common concern was whether the use of look-through and risk scaling would be construed as gaming techniques. In our view the opposite applies: these techniques actually improve the accuracy of performance assessment while reducing the constraining impact of the performance test on the ability to maximise member outcomes. Sadly there are far easier ways to game the performance test.

It may well be that trustees of funds approve an SAA for YFYS reporting purposes but develop other internal AA targets that direct portfolio activity.

Reduced flexibility, more market timing

Over time we think funds will find they have less flexibility, particularly as they face into alternate investment scenarios. The oft-cited inflationary scenario is a good example: many of the investment strategies to deal with this scenario (such as inflation linked bonds, low duration bonds and specific equity sectors) incur high performance test tracking error.

In response some funds may undertake more market timing. We find this concerning: the evidence on market timing is mixed at best, and many Australian super funds haven’t applied this activity in size. This leaves a question mark around capability, culture, and governance. So we have a scenario where a flawed test drives activity to another activity which is not assessed.

ESG integration

Any activity that actively manages risk to member outcomes, beyond the SAA decision to the prescribed benchmarked-sectors, generates performance test tracking error. Managing ESG risks is no different. We think ESG activities will trend towards an engagement model with other techniques like impact investing, opportunistic investing and exclusions used to a smaller degree.

Pathway forward for super funds

We summarise many of the key considerations for super funds in the diagram below.

The diagram outlines many activities that need to be undertaken. The timeframe for the dust to settle on this transition period could be 12 to 18 months.

Unfortunately, we can only see funds being more constrained in their ability to manage portfolios to maximise outcomes for members. Funds may be able to reduce the degree of constraint by reviewing how they report their SAA. The constraints may prove problematic should other market scenarios evolve, creating the potential for the performance test to generate a significant implicit cost to consumer outcomes.

Looking forward there are some positives. The most significant uplift is likely to be in investment governance standards, as funds work through a review of their investment models to adjust to the constraints created by the performance test.

Leave a Comment

You must be logged in to post a comment.