Seven per cent is the hottest metric in town! It seems that that is the percentage of members who have closed their accounts since funds sent out their YFYS performance test failure notification letter and has topped the number 13, which was how many MySuper options failed the performance test, on the unofficial metric billboard.

For all the management jargon around big data we still seem to prefer overly simple metrics to assess complex outcomes.

This was an issue during the debate about the design of the flawed performance test. Hopefully it won’t be the case when reviewing the policy outcomes achieved by that test.

When the Government cherrypicked from the Productivity Commission’s final recommendations for improving superannuation outcomes they chose the performance test but placed aside the (also controversial) best-in-show model. In doing so they positioned consumers as the primary mechanism for punishing funds deemed to be underperforming.

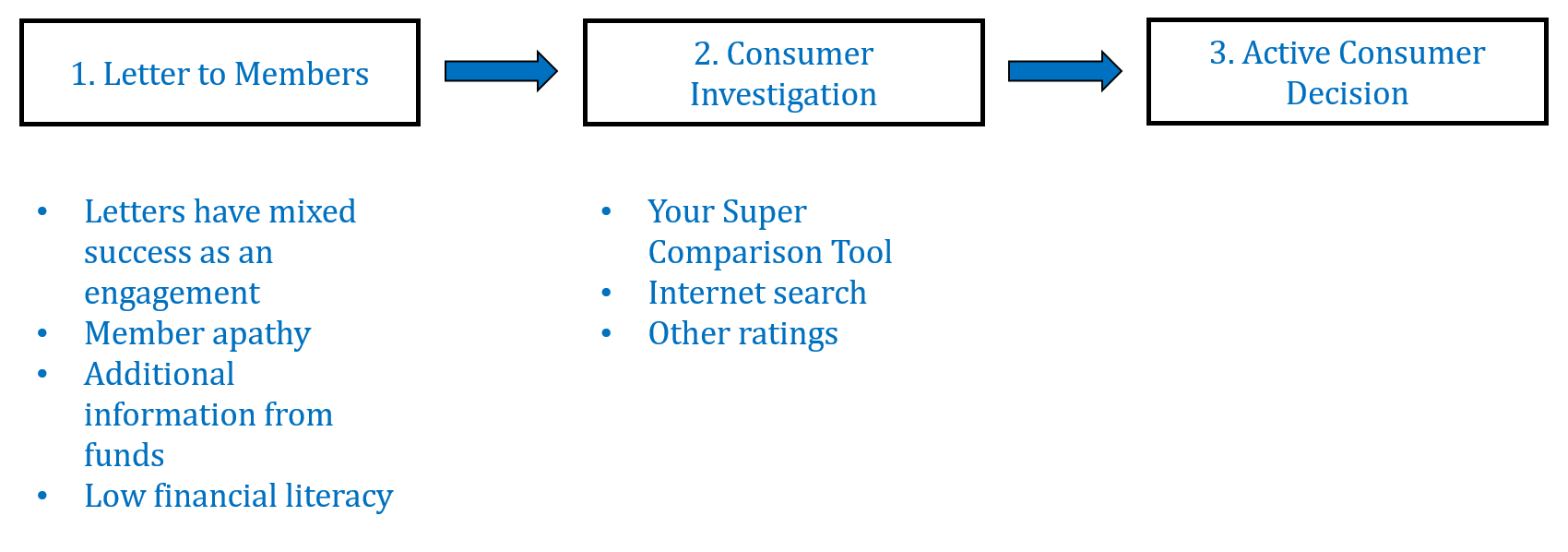

Relying on consumer engagement to make a financial services policy successful is risky. The diagram below sets out the possible consumer experiences associated with the performance test. Keep in mind that the design of the performance test has been controversial and heavily contested.

As we work through elements of the above diagram consider that the letters (if opened) may create some positive inertia to act. But every doubt created over the performance test result, and its connection to future performance, will dilute that inertia.

Consumer engagement on financial matters is low.

Here, another recent metric from the billboard: a recent KPMG survey found that 80 per cent of members in merged super funds didn’t know their fund had merged.

Letters are a weak engagement tool, but their impact can be improved. For example, the Swedish Pensions Agency sends out an annual letter in an orange envelope as part of a month-long engagement program.

Though the wording of the performance letter is standardised, funds can communicate further. This could credibly highlight the flaws of the performance test, how it may not align with what the trustee determined to be an appropriate strategy for their members and the steps taken to improve future performance. Funds could also take advantage of this situation, a concern raised by Super Consumers Australia.

It is likely that consumers will face competing information, and most confront this situation with low financial literacy. Australia’s financial literacy levels, as measured by leading academics Hazel Bateman and Susan Thorp, are poor, just like in most countries.

Now let’s consider the consumer who investigates further. They will probably want to understand some important issues:

- Is the YFYS performance test high quality?

- Are funds which failed the performance test poor funds?

- How should they choose an alternative super fund?

Engagement is insufficient. Engagement needs to be accompanied with a good decision. An engagement-based policy is only successful if consumers move to a better alternative fund.

The government recommends consumers visit the ATO’s Your Super Comparison Tool. The site is relatively easy to navigate and focuses on the important issues of performance and fees. But it has many flaws: it is risk agnostic and doesn’t consider other important issues such as insurance. There is a clear risk that consumers make a poor choice. One simple example: the range in levels of growth exposures amongst different MySuper options exceeds 30 percent.

If consumers search for verification that the YFYS performance test is a quality metric that informs future performance, they will discover substantial information to the contrary. Searching ““flawed” Your Future Your Super performance test” yields nine million results.

A savvy consumer, taking heed from long-held disclosures and messaging about past performance not being an indicator of future performance, might broaden their search. They might check whether these funds are rated externally. According to one ratings group three of the 13 funds had the highest possible rating and two the second highest rating.

Bringing this all together: seven per cent (thus far) sounds like a reasonable engagement level, but it is doubtful the number will ever become a substantial portion of fund membership. Simply put, letters don’t engage apathetic consumers, and any positive inertia generated by the letter will be diluted by other information, especially given low levels of financial literacy.

However, account closures is a poor metric for assessing the policy outcomes of the performance test. If we choose to run with this simple metric, we won’t ever know how well this policy really worked. Engagement can be a positive outcome but can also result in poor decisions which leave consumers worse off. The real question is: how many members went to a better fund with an appropriate risk profile and insurance arrangements? This is the question APRA or Treasury need to get data on. Hopefully this is work already being undertaken, and if not then it should start soon.

Leave a Comment

You must be logged in to post a comment.