When it comes to high-emitting businesses, as an asset owner, ‘should I divest or engage’? The answer is that you are probably asking the wrong question.

You perhaps should be asking: ‘do I want to decarbonise the economy or just my portfolio? Is my goal reducing my financed emissions or the tougher task of financing emissions reductions? Am I seeking value alignment or real world impact?’

And, of course, divestment and engagement are not mutually exclusive. As the Principles for Responsible Investment’s Discussing Divestment report notes, “many investors favour a stewardship-first approach that includes divestment as the final step in an escalation strategy”.

Last month the Investor Group on Climate Change (IGCC) waded into the issue in a new discussion paper. The issue for asset owners is that if investees sell emissions-intensive assets, “it may maintain or even increase the systemic risks that climate change poses to overall financial returns,” IGCC says. And simply divesting doesn’t make those risks go away.

The IGCC paper says asset owners should consider supporting a managed phaseout approach that goes beyond a blanket exclusion of companies with emissions-intensive assets and instead, “interrogates the company’s asset and decommissioning expertise and the merits of corporate and asset-specific transition plans”.

Asset owners should also be encouraging ‘good sellers’ and ‘good buyers’ by engaging with the seller of an emissions-intensive asset, and the buyer if possible, “to ensure that the characteristics of responsible ownership and managed phaseout are considered in the transaction”.

In IGCC’s ideal world, both the asset seller and buyer would have published Climate Transition Action Plans in line with international best practice; the sellers would ensure that buyers have the resources necessary to run and decommission the emissions-intensive asset; and the buyers would commit to a “just transition” for workers and the community that would be “at least equivalent” to those of the sellers.

Unfortunately, today’s reality is a little different. IGCC cites recent Environmental Defense Fund research on oil and gas merger and acquisition activity that shows assets flowing at a significant rate from public to private markets that typically have lower public transparency and accountability. Assets were also moving away from companies with net zero and environmental commitments to those with” a less rigorous” approach to climate and environmental issues.

Phaseouts

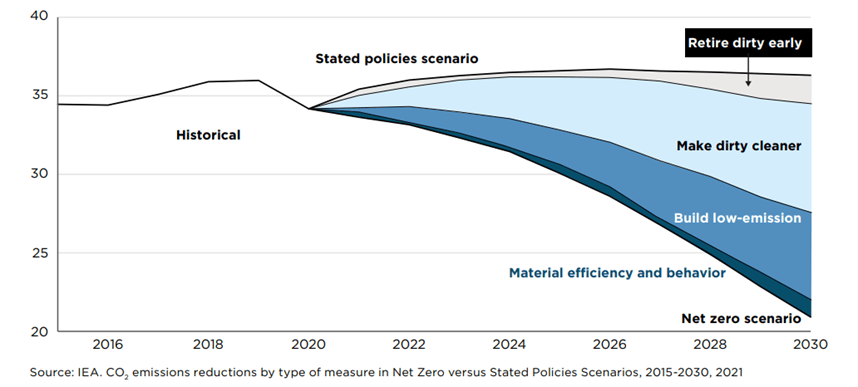

The IGCC discussion draws upon an earlier Glasgow Financial Alliance for Net Zero (GFANZ) report The Managed Phaseout of High-emitting Assets. The GFANZ report says achieving net zero involves developing new no/low-GHG emissions assets, decarbonising existing high-emitting sectors, and the phaseout of high-emitting assets before the end of their normal operating lives (i.e. “retire dirty early”).

GFANZ says managed phaseouts offer an acceptable alternative to divestment or withdrawing finance that could have the “unintended consequence of prolonging the life of high-emitting assets and even worsen their GHG emissions profile if they are transferred to those with less climate ambition, disclosure, or scrutiny”.

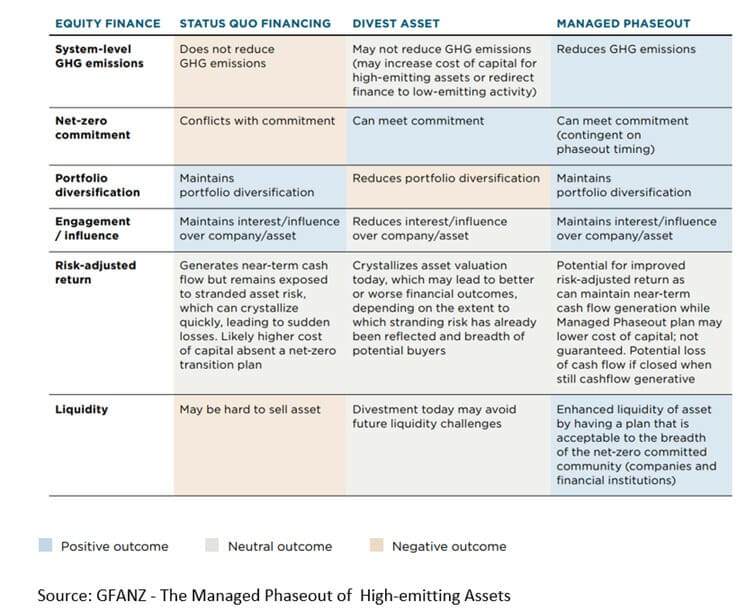

Managed phaseout provides the only approach for asset owners and other financial institutions that leads to a reduction in GHG emissions from the asset in question, according to GFANZ (see table below).

Managed phaseouts “promote an orderly transition by reducing the risk of sudden value destruction from stranding” and “mitigate financial marginalization for companies that have high-emitting assets but with credible transition plans for their retirement,” the GFANZ report says.

Getting real

A recent report from the Columbia Center on Sustainable Investment urges financial institutions to communicate clearly and accurately about their climate-related pledges and commitments.

“Current approaches to net-zero pledges are inconsistent about whether their purpose is to drive global climate goals, to mitigate financial risks for financial institutions, or to align with transition trajectories – which are different objectives with different implications for strategy and metrics.

“The current range of climate-related pledges, alliances, frameworks, and tools at times confuse or conflate risk mitigation with climate action, relying on targets and metrics that may not be fit for purpose,” the CCSI report says.

Equity portfolios constructed with no or low carbon-intensive assets may have lower exposure to climate risk than a portfolio with high-emitting assets, but they have no climate effect in the real economy. A focus on decarbonising portfolios shifts ownership of existing shares “with no impact on real economy emissions,” according to the report.

CCSI says with the biggest challenge being mobilizing the trillions of dollars needed to achieve the Paris Agreement climate goals the emphasis needs to be “on how new finance is being directed and whether new finance is contributing to and not undermining a rapid and just transition”.

Too much of the focus of ‘climate alignment’ by investors has been on secondary markets, where securities already sold by a company are traded among secondary purchasers. CCSI argues ‘sustainable finance’ has mainly been a “taxonomic exercise” labelling existing equity and debt finance as responsible/green/ethical etc.

“However, divestments and labels do not influence the capital stock of the target companies. What does, is access to new capital (or capital available on better terms) on primary markets, through initial public offerings … and new debt capital for established publicly listed companies,” CCSI says.

Asset owners should focus net-zero’ commitments and initiatives “on the reduction of real-economy emissions and on reducing demand for fossil fuels throughout other sectors in the economy”. They should “look to each company’s strategy, investments, and operational plans to assess decarbonization progress along science-based pathways”. Absolute science-based emissions targets should be prioritised over emissions-intensity targets and offsets should be limited to residual emissions.

Ticking time bomb

The IGCC discussion paper was published just a week after the Federal Resources Minister Madeleine King launched a road map to establish an Australian decommissioning industry issues paper. As Australia moves to reduce its emissions and its reliance on fossil fuels, the country needs to build capability to undertake the estimated $60 billion decommissioning of our oil and gas infrastructure between now and 2050.

In response, the Australasian Centre for Corporate Responsibility (ACCR) warned that the Australian oil and gas industry “has been sitting on a ticking time bomb of decommissioning liabilities for decades, and has not been honest with the government or investors about the true extent of the costs and risks”.

Also last month environmental group Market Forces claimed Australia’s largest super funds are failing to rein in the expansion plans of oil and gas companies such as Woodside and Santos. Market Forces is urging super fund members to directly write to their super funds asking them to immediately escalate pressure on the companies; publicly demand the end to fossil fuel expansion; and publish their timelines for divestment if they do not comply.

Kicking off the blankets

The European Corporate Governance Institute’s recent Socially Responsible Divestment working paper looks at the divest or engage question in a novel way. In the EU, regulations and directives can pressure asset owners and managers to divest or exclude ‘brown’ stocks even if they may be ‘best-in-class’, the paper says.

“Even if a firm is in an irremediably brown sector, where externalities are always negative, the manager may be able to take corrective actions to mitigate these externalities. Blanket exclusion fails to reward such actions because the firm is divested no matter what,” according to the ECGI paper. There would be better outcomes if a ‘tilting’ strategy was pursued that tilts away from a brown industry but is able to hold stocks that are genuinely taking corrective action.

Rather than punishing sustainable funds that include brown stocks “regulators should police the opposite behaviour in sustainable funds that claim to be actively managed but blanketly exclude certain sectors”.

A tilting strategy could also be employed for ‘green’ stocks where managers overweight green industries but avoids ‘worst-in-class’ companies within such sectors. The ECGI says this “may be more effective than blanket inclusion”.

“An investment strategy that tilts away from brown sectors and towards green sectors will require similar amounts of capital to one that automatically excludes the former and includes the latter. While tilting requires capital to hold best-in-class brown firms, it also saves capital by avoiding worst-in-class green firms,” the paper says.

Leave a Comment

You must be logged in to post a comment.