Australia and most of the ex-China world need to urgently undertake a collective reality check when it comes to building vital global supply chains for critical minerals, Including rare earths.

Prime Minister Anthony Albanese and Federal Resources Minister Madeleine King both have been suggesting that the critical minerals we have in the ground are a bargaining chip we can use in tariff discussions with the United States.

Earlier this month Albanese said the government would establish a “critical minerals strategic reserve”, in an announcement that contained no detail but presumably involves some sort of stockpiling of critical minerals that would be made available to favoured countries.

Last month King was apparently saddened the US did not accept an offer of a more reliable supply of critical minerals in return for steel and aluminium tariff exemptions.

At the recent US Super Summit, Treasurer Jim Chalmers boasted Australia can supply about three-quarters of the 50 minerals that the US lists as critical and our Ambassador to the US, Kevin Rudd, claims “Australia equals the periodic table [and] we stand ready to assist.”

Deluded

However, the government seems to be deluding itself here.

Critical minerals projects in Australia are owned by private sector companies – whether they be Australian or overseas-owned corporations.

So of course the government should not be promising the commodities that may be extracted from them to overseas governments or any other parties. The minerals will go to whoever sign offtake agreements with the project owner.

The Minerals Council of Australia says a strategic reserve would be adding “domestic political risk to the numerous hurdles that miners already face in getting projects off the ground”.

And claiming Australia is a “periodic table” may be overlooking the fact that a large of the number of the critical minerals projects being pursued by Australian companies are in fact developing deposits in other countries.

For example, Syrah Resources – which is 33 per cent-owned by AustralianSuper and accounts for a big chunk of the super fund’s critical minerals portfolio – relies on its Balama graphite mine in Mozambique to feed its downstream active anode material (AAM) facility in the US (unfortunately Balama is currently shutdown due to ongoing political unrest in the African nation).

China syndrome

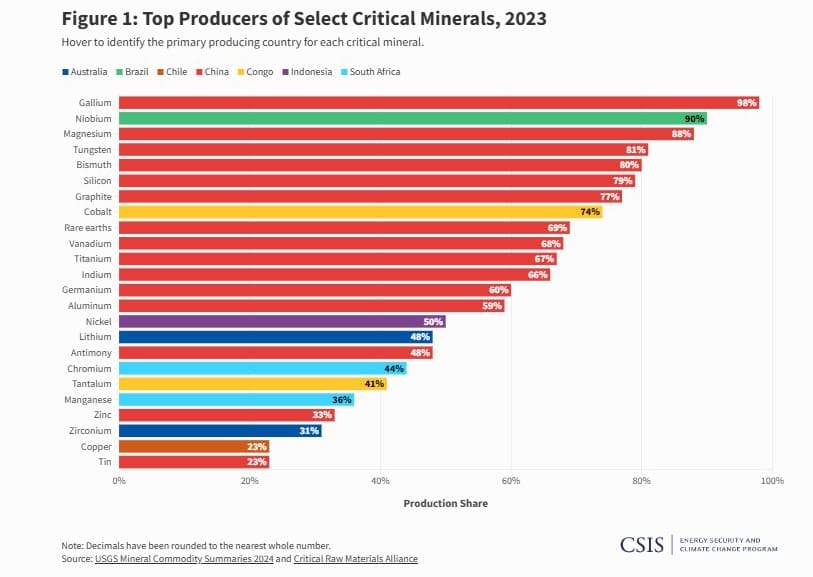

Existing critical minerals supply chains are dominated by China (see Figure 1 below), and the US is particularly vulnerable.

China is the chief import source for about 20 of the US’s 50 critical minerals and for some commodities this import reliance is more than 90 per cent, according to the Center for Strategic and International Studies.

For those concerned by China’s dominance, Figure 1 does indeed look alarming – but the ex-China world has been doing very little about it.

And this situation has just got worse with China placing export restrictions on rare earth elements in response to the US Trump Administration’s “reciprocal tariffs”.

Back in 2022 the then US-led Minerals Security Partnership (MSP) was launched with much fanfare.

The MSP currently has 15 partners: Australia, Canada, Estonia, Finland, France, Germany, India, Italy, Japan, Norway, the Republic of Korea, Sweden, the United Kingdom, the US and the EU.

There are another 15 countries that are members of the more recently-established MSP Forum: Argentina, Ecuador, the Democratic Republic of the Congo, the Dominican Republic, Greenland, Kazakhstan, Mexico, Namibia, Peru, the Philippines, Serbia, Türkiye, Ukraine, Uzbekistan and Zambia.

There is also a MSP Finance Network that includes more than 35 government export credit agencies (ECAs) and other funding vehicles, including US International Development Finance Corp, Export Finance Australia, European Investment Bank, Nordic Investment Bank, Japan Organization for Metals and Energy Security, Korea Trade Insurance Corp, and UK Export Finance (UKEF).

The MSP’s goal is to “accelerate the development of diverse and sustainable critical energy minerals supply chains” and the above groupings suggests it has plenty of firepower. However, the now South Korea-chaired MSP seems to have achieved very little in terms of reducing the amount of red that appears in Figure 1.

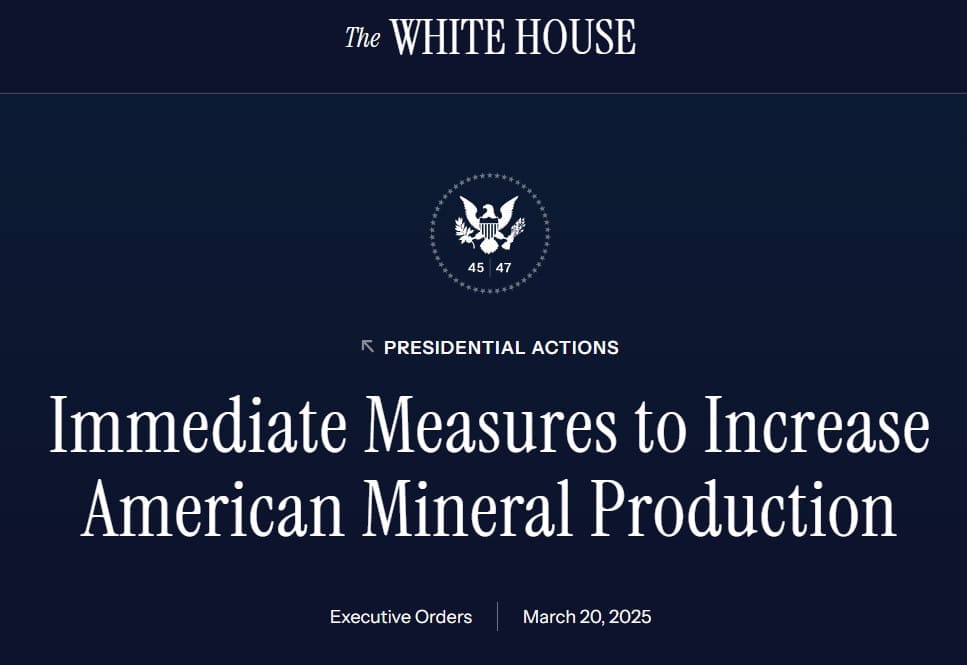

Another Executive Order

So how is the US dealing with critical minerals supply chain crisis (apart from wanting to grab Greenland, consume Canada or bully Ukraine into handing over its resources)?

On March 20 President Donald Trump signed an Executive Order invoking the Defense Production Act to increase domestic minerals production for national security.

In the order Trump laments “the US was once the world’s largest producer of lucrative minerals, but overbearing Federal regulation has eroded our Nation’s mineral production.

“Our national and economic security are now acutely threatened by our reliance upon hostile foreign powers’ mineral production. It is imperative for our national security that the US take immediate action to facilitate domestic mineral production to the maximum possible extent”.

The order expands the US’s critical minerals list to include copper, uranium, gold, and potash – and allows the new National Energy Dominance Council (NEDC) to add others at its whim.

Trump seems to think domestic production can be quickly cranked up if the NEDC is simply given a “priority list” of projects located on Federal lands “that can be immediately approved or for which permits can be immediately issued”.

And to further speed things along for those applying for government funding, it seems project proponents won’t have to provide much information as to the viability of their projects.

Permitting

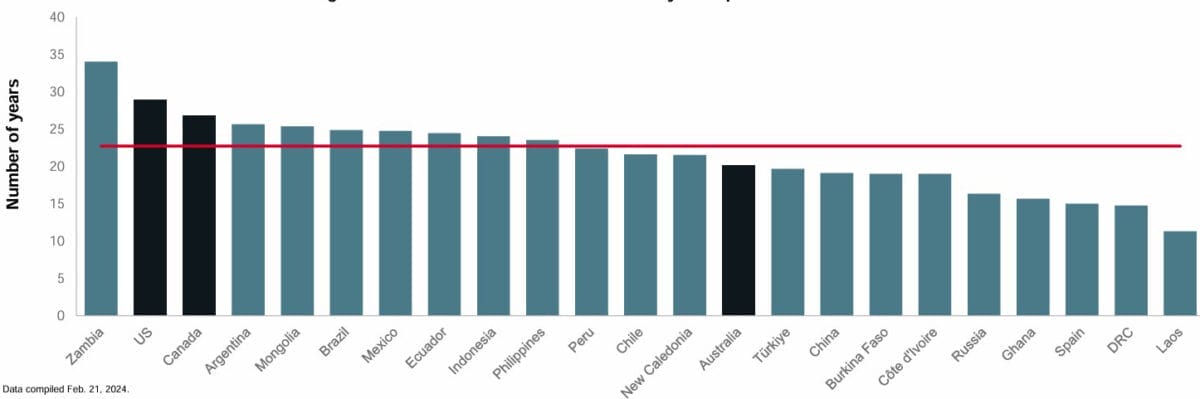

Permitting on Federal lands in the US has been one of the biggest barriers to developing domestic mineral projects.

Permitting delays is one of a number of factors that have contributed to the US having the second-longest lead times in the world to develop a mine (based on data that includes mines that have not begun operating yet).

An S&P Global report Mine Development Times: The US in Perspective found that it takes an average of 29 years for mines to go from discovery to production, longer than any other country except Zambia (see chart below).

S&P noted that the long US lead times stand in contrast to the country’s sizeable resource base. For example, the US copper endowment is comparable to those of Canada and Australia combined and is sufficient to satisfy domestic demand for the foreseeable future.

The US endowment of lithium is also more than twice that of Australia, which accounts for half of the world’s lithium production.

Another list

The Europe Union also thinks publishing a list will solve its critical minerals problem.

The European Commission has just adopted a list of 47 “strategic projects” to boost the EU’s domestic strategic (critical) raw material capacities.

These projects will “be able to benefit from coordinated support by the commission, member states and financial institutions to become operational, notably regarding access to finance and support to connect with relevant off-takers”.

They will also benefit from streamlined permitting provisions. The permit-granting process will not exceed 27 months for extraction projects and 15 months for other projects. Currently, permitting processes can last from five to 10 years.

The Commission dubiously claims that approvals timelines can be dramatically reduced “while safeguarding environmental, social and governance standards”.

Offtake mistake

The required reality check is really about offtake agreements.

Before providing equity and debt for a project investors, bankers and other financiers want to see offtake agreements in place. However, before signing a binding offtake agreements customers want proof the minerals project has definitely secured financing.

A solution to this Catch-22 situation would be for governments – either alone or in partnership with other countries – tounderwrite or sign offtake agreements.

Ideally, these would include minimum revenue guarantees given the opaque pricing of many critical minerals and China’s ability to hurt new competitors by temporarily depressing prices by lifting its exports.

Discussing Greenland’s critical minerals resources, Bank of Greenland chief executive officer Martin Kviesgaard recently said that “without guaranteed buyers, commercial extraction of critical raw materials remains so risky that investments may not get off the ground”.

“What we’re missing is the EU or the US stepping up and saying, ‘We’ll take these raw materials,’” he said.

Kviesgaard said “China has built its dominance in the sector by doing exactly that. We need a new way of thinking about how to become independent from China, and that could be by making concrete buyer agreements.”

This where the countries involved in the MSP should be genuinely be working together to ensure offtake agreements are put in place.

However partnerships can be slow to deliver outcomes. Countries typically have multiple bilateral partnerships – for example, Australia has separate critical minerals agreements with Japan, Korea, Canada, India and the US – and are members of a range of multilateral partnerships. This often complicates matters.

Typically, when ECAs from different countries are asked to support a project they want to see the other ECA make the first move. Different governments also often set different goals for their ECAs.

Super solution

Treasurer Chalmers told the US super summit audience that “Australia’s superannuation sector has the size, scale and presence to play a big role driving new American industries and creating jobs”.

Chalmers talked about super funds investing in US stockmarkets, in data centres in Las Vegas, in toll roads in Indiana and in container terminals in Long Beach.

Investing in another toll road is unlikely to ingratiate us much further with Trump. But there is a way we could use as leverage the US$600 billion ($953 billion) that Australian super funds are effectively promising to invest in the US over the next decade.

Our super funds might consider keeping some of this money at home to invest in advanced critical minerals projects in Australia to help fund them into production.

This would be on the proviso that the US government is prepared to underwrite binding offtake agreements for the projects on behalf of US industry.

All it should take at the US end is just one more Executive Order

Leave a Comment

You must be logged in to post a comment.