The global architecture meant to keep asset owners and asset managers on the same page on net zero and climate change is crumbling.

At the start of 2025 the Net Zero Asset Managers (NZAM) initiative suspended its activities and launched a review to determine if it was still fit for purpose. NZAMI promptly removed its commitment statement and list of signatories from its website.

NZAM cited “recent developments in the US and different regulatory and client expectations in investors’ respective jurisdictions” for the decision.

NZAM’s suspension followed a series of asset manager departures, with the final straw being BlackRock who exited because its membership apparently “caused confusion regarding BlackRock’s practices and subjected us to legal inquiries from various public officials” in the US.

Before these developments asset owner networks like Paris Aligned Asset Owners (PAAO) and the Net Zero Asset Owners Alliance (NZAOA), and the 325 asset managers who had signed up to NZAM were being encouraged to use the recently updated Net Zero Investment Framework 2.0 (NZIF) to develop their net zero objectives and targets in a common language.

The NZIF was created by the Paris Aligned Investment Initiative (PAII) ,which is backed by the Investor Group on Climate Change (IGCC) in Australia, the Institutional Investors Group on Climate Change (IIGCC) in Europe, Ceres in North America and the Asia Investor Group on Climate Change (AIGCC).

But now that the shutters have pulled down on NZAM – which at its peak membership involved managers with more than US$57.5 trillion ($90.9 trillion) in assets under management – member interest in NZIF or similar frameworks will no doubt wane and be very difficult to track.

Little impact

But what NZAM had really been achieving is questionable. ShareAction’s recently-published report Voting Matters 2024: Are asset managers using their proxy votes for action on environmental and social issues? suggests it had not achieved as much as the Trump-abandoned Paris Agreement requires.

Voting data – a good proxy for engagement and action – shows that even prior to NZAM’s suspension, membership of NZAM appeared to have little impact on asset managers’ voting records on climate resolutions, according to ShareAction’s report.

NZAM members voted in favour of an average of 64 per cent of climate resolutions, compared to 55 per cent for non-members. However, this gap was inflated by the asset managers who departed NZAM (as at 16 December 2024) as they on average only voted for 35 per cent of climate resolutions and thus weighed down the non-member results.

These departees included Baillie Gifford, Goldman Sachs Asset Management, Nuveen Asset Management, and Vanguard (who actually left in late 2022). Northern Trust Asset Management has also since left NZAM.

Asset managers who had never been a member of NZAM voted in favour of 61 per cent of climate resolutions, a similar proportion to NZAM current members.

CA100+

Asset-manager departures throughout 2024 and into 2025 have also hit Climate Action 100+, the network of 600 or so asset managers and asset owners pushing the world’s largest corporate greenhouse gas emitters take action on climate change to mitigate financial risk and to maximise long-term asset value.

The managers that have abandoned CA100+ – which is also co-ordinated by IGCC, IIGCC, Ceres and AIGCC as well as the Principles for Responsible Investment (PRI) – in include abrdn, AllianceBernstein, Allspring Global Investments, Baillie Gifford, BlackRock (which withdrew its US business), Franklin Templeton, Goldman Sachs Asset Management, Invesco, J.P. Morgan Asset Management, MFS, Northern Trust, Nuveen Asset Management, Pacific Investment Management Company (PIMCO), State Street Global Advisors, Sun Life Financial and Vanguard.

Most of these are US asset managers apparently buckling under pressure from the conservative anti-ESG forces and threats of legal action.

ShareAction’s report says remaining CA100+ members showed stronger voting performance on resolutions flagged by CA100+ in 2024 than non-members, “suggesting members are taking their commitment seriously”.

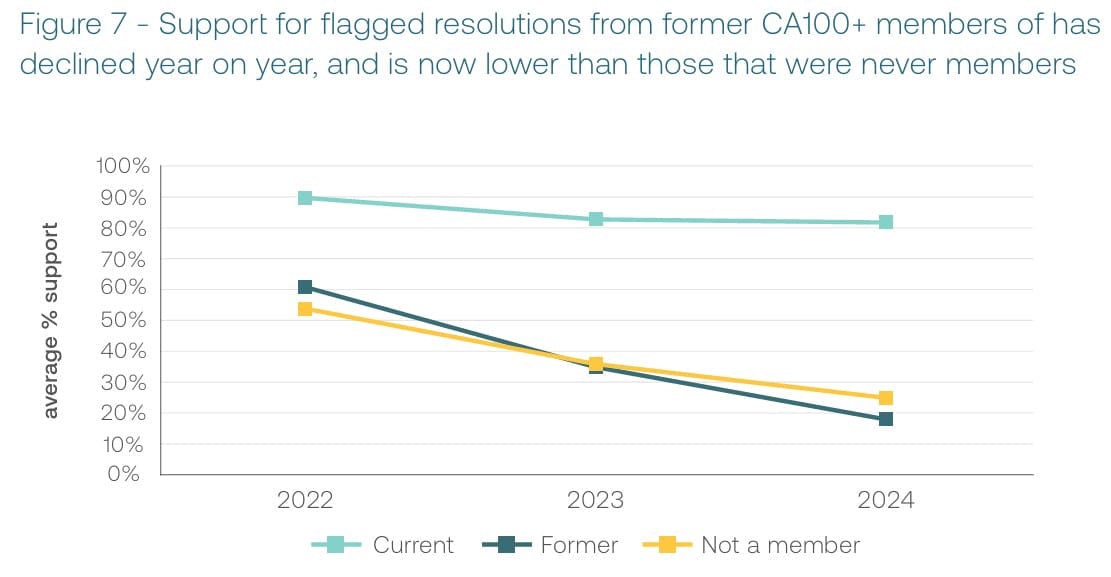

Remaining CA100+ members are probably thinking ‘good riddance’ to those who have exited as they have been a drag on their efforts. The former members voted for considerably fewer flagged resolution in both 2022 and 2023 compared to the remaining members, according to the report (see Figure 7 below).

“Shockingly, the departing members are now supporting fewer flagged resolutions (22 per cent on average) than the institutions who have never been members, who voted on average for 38 per cent of resolutions,” ShareAction said.

This data suggests the departing asset managers may never have had their hearts in it when signing up; had joined because it was the expedient thing to do; had viewed CA100+ membership purely as a marketing exercise; and/or had a relaxed attitude to greenwashing.

Poor performance

ShareAction also called out some remaining CA100+ members, including Australian industry funds-owned IFM Investors, who “continue to show poor performance”.

“Eight current members voted for less than half of flagged resolutions and one, Mackenzie Investments, did not vote in favour of a single resolution,” according to the report” (see Figure 8 below).

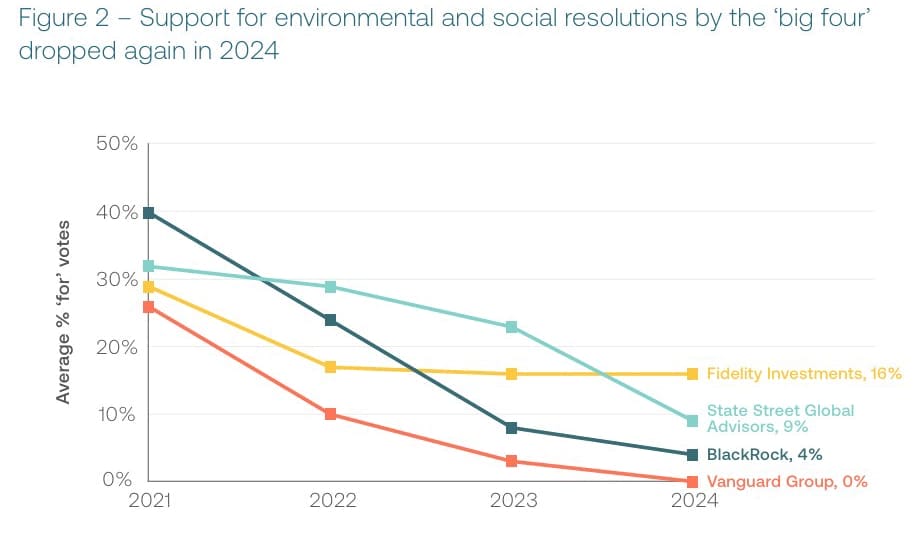

Big 4 failure

The report points an accusatory finger at the world’s biggest asset managers BlackRock, State Street, Vanguard and Fidelity Investments who have combined assets under management of US$23 trillion.

In 2024 they voted for fewer shareholder proposals than ever, with all four managers placed in the bottom ten positions in ShareAction’s ranking of asset manager voting performance.

Vanguard performed the worst of all the managers ShareAction assessed, voting in favour of zero per cent of environmental and social shareholder proposals (Figure 2 below).

ShareAction noted that while BlackRock, State Street and Vanguard predominantly use passive investment strategies this was no excuse for inaction.

UK-based passive asset manager Legal & General Investment Management, for example, backed 90 per cent of resolutions.

Going easy on escalation

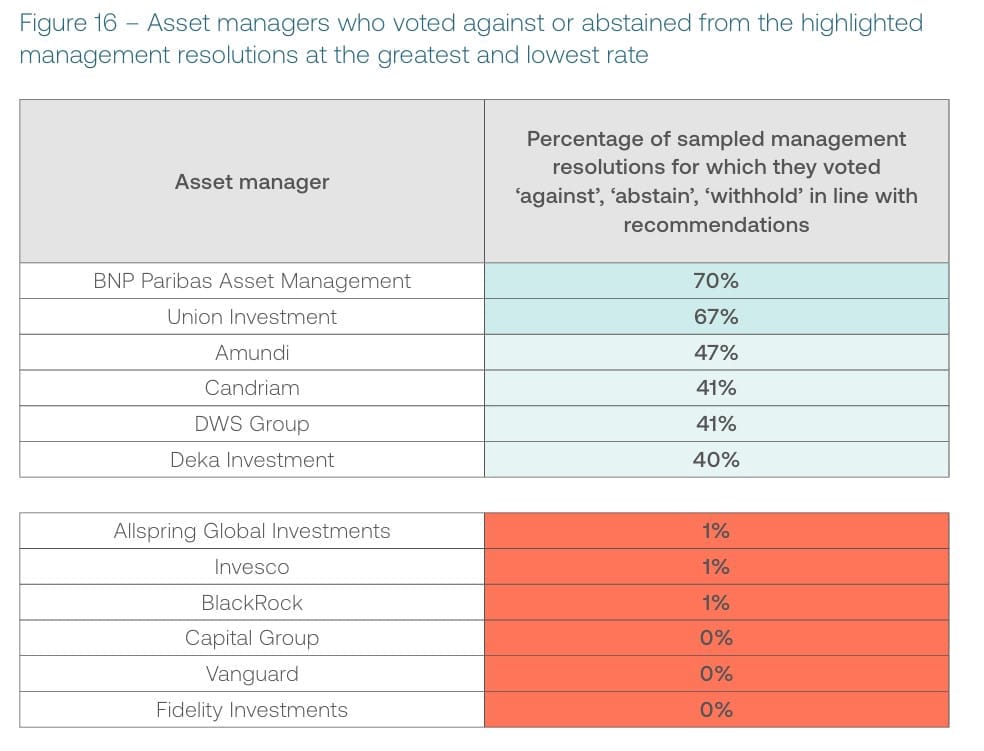

ShareAction says many asset managers are not making effective use of votes against management items as an escalation tool.

The NGO said it “compiled robust, public recommendations for votes against or to abstain on management items in sectors associated with high greenhouse gas emissions in the 2024 AGM season” and found that only 11 asset managers voted in line with more than 20 per cent of these recommendations.

ShareAction also found it “concerning that the poorest performers include three of the four largest asset managers in the world, BlackRock, Fidelity and Vanguard” (see Figure 16 below).

Asset owner statement

Last month a coalition of assets owners from the UK, Europe, Australia and the US, representing USD$1.5 trillion in funds management published an Asset Owner Statement on Climate Stewardship.

The statement – endorsed by the likes of The People’s Pension, Brunel Pension Partnership , Church of England Pensions Board ,Nest and Australian Ethical Investment – sets out their climate stewardship expectations.

The signatories are seeking to address the “ongoing and material divergence between asset owner expectations and implementation of climate stewardship that limits progress towards a net zero world and better outcomes for beneficiaries”.

They expect managers to commit to aligning their climate engagement activities with the goals of the Paris Agreement, with appropriate governance and oversight, and transparency and reporting to their client base.

“Whilst recognising the importance of individual engagement, collaborative engagements enable investors to have a more impactful voice across issues of prime importance. Initiatives such as CA100+, can therefore, be a positive indication that the manager seeks to leverage partnerships for additional impact and expertise,” the statement said.

Asset managers should also have robust escalation processes in place and articulate how different types of escalation are used within what timeframes when climate expectations are not met.

The statement warns “for some asset owners, poor or misaligned stewardship activity could contribute to a downgrade in asset manager ratings, a reassessment of the mandate, or the selection of asset manager/s demonstrating greater alignment with the pension scheme’s objectives”.

Soon after the statement one of the signatories, The People’s Pension, the UK’s largest commercial master trust, announced that £28 billion (%57.7 billion) in funds previously managed by State Street had been moved to two other managers.

Amundi, Europe’s largest asset manager, will now manage £20 billion in passive developed market equities, while Invesco takes on about £8 billion in fixed income investments for its defined contribution scheme.

Without mentioning State Street, The People’s Pension said “both appointments represent a step forward in achieving greater alignment with The People’s Pension’s stewardship approach and priorities”.

Aussie asset owner dilemma

According to a report commissioned by IFM Investors Australian pension fund investment in the US is expected to skyrocket over the next decade – from US$400 billion to over US$1 trillion ($1.6 trillion).

This may pose some big challenges for Australian asset owners in deciding who should be managing these funds.

How difficult is it going to be find managers who will invest and engage in line with their expectations, if those expectations include sustainability and/or ESG considerations.

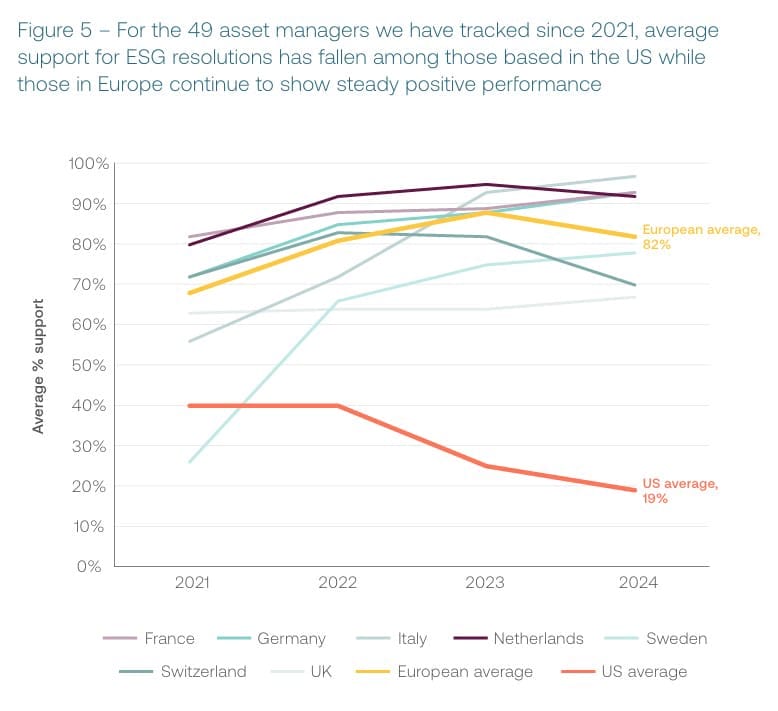

The ShareAction report also shows that for the 49 asset managers it has monitored in recent years, average support for ESG resolutions has nosedived among those based in the US while Europe-based asset managers are still showing good support (see Figure 5 below).

State Street’s just-released Global Proxy Voting and Engagement Policy 2025 highlights the challenge. The US asset manager makes it clear not to expect too much from it when it comes investor engagement.

State Street says “we believe that company boards do right by investors” and so “we generally do not support shareholder proposals that appear to impose changes to business strategy or operations”.

It also does “not expect or require companies to adopt net zero ambitions or join relevant industry initiatives” and when it comes to diversity, equity and inclusion (DEI) “we believe nominating committees are best placed to determine the most effective board composition”.

And how about BlackRock, the former (self-proclaimed) undisputed ESG heavyweight world champion who has since revealed it has a glass jaw?

BlackRock’s 2025 Investment Stewardship guidelines says that while it considers the transition to a low carbon economy “as one of the several mega forces reshaping the markets” it does not regard the question of whether a company should have a transition plan as a “voting issue”.

Not surprisingly given the anti-DEI crusade in the US, BlackRock also no longer refers to ‘board diversity’ but only to ‘board composition’, and has removed previous references to numerical gender and racial/ethnic diversity thresholds.

SEC Guidance

The US Securities and Exchange Commission’s (SEC) latest guidance also gives the big asset managers further reasons to back track on ESG and to treat their investees with kid gloves.

The SEC guidance suggests that asset managers will be required to complete more onerous documentation on their investments if it is deemed the securities they hold were acquired and are held “for the purpose of or with the effect of changing or influencing the control of the issuer.”

Examples of what might be covered here include a manager recommending an investee change its executive compensation practices, or undertake specific actions on a social, environmental, or political policy.

More onerous disclosure will be required if an asset manager discusses with an investee’s management “its voting policy on a particular topic and how the issuer fails to meet the shareholder’s expectations on such topic”.

It may be the case that as Australia’s super funds shovel more of their members’ money into the US they will need to dial down their own sustainability rhetoric if their asset managers cannot deliver on it.

Leave a Comment

You must be logged in to post a comment.