It is not hard to see why sustainability-linked bonds (SLBs) have an image issue.

Unlike green bonds or sustainability bonds – where capital must be directed to specific “green” projects-or activities – funds raised by SLBs can be used by companies (and other issuers) for any purpose.

A fossil fuel producer could refinance its existing debt through SLBs to demonstrate its commitment to “sustainability”. By choosing a sustainability performance target (SPT) – such as reducing its greenhouse gas (GHG) intensity – the company could be, say, expanding its coal business and generating higher total emissions while still being rewarded for is sustainability efforts.

If the GHG intensity SPT is unambitious enough the company may have little trouble meeting it. And if it looks like it may not, there is typically plenty of scope to manipulate the original target.

In any event, if it fails to meet the SPT probably not much harm will be done. If the company is large and robust enough, paying the typical “step-up” bond coupon penalty of 25 basis points may not be particularly onerous (especially if it had already quietly budgeted for it).

Greenwashing concerns

Earlier this month the Luxembourg Green Exchange (LGX),which is run by Luxembourg Stock Exchange, released a study of the “entire SLB universe” .

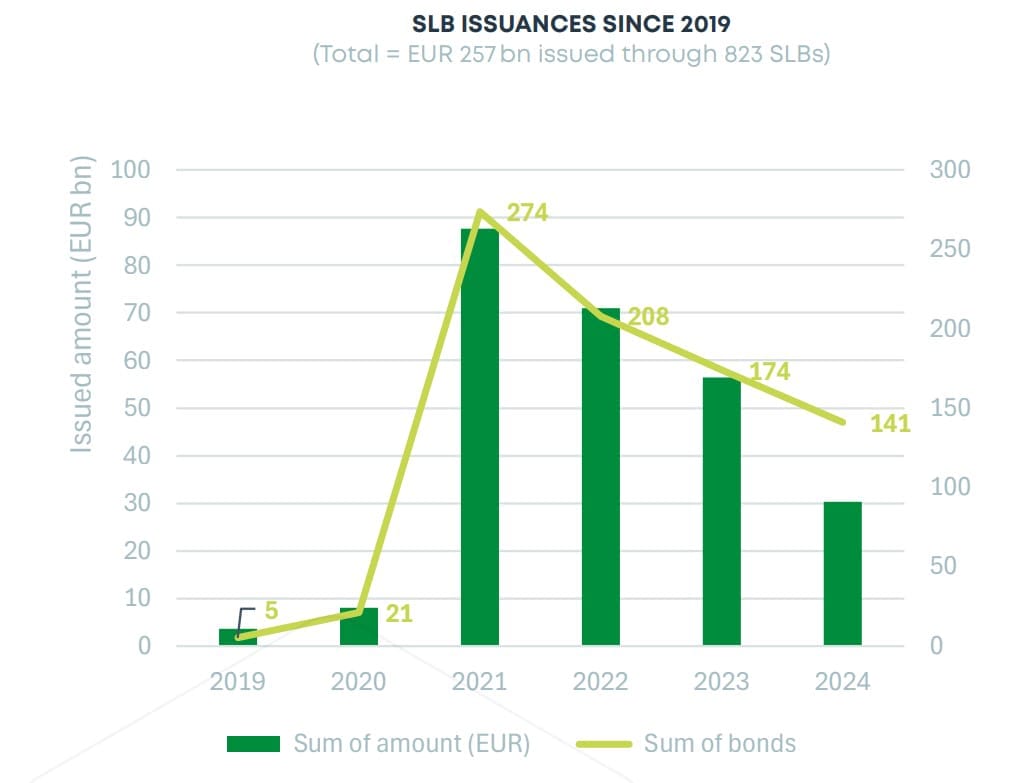

The report Targeting Transition: Exploring the Evolution of Sustainability-Linked Bonds shows why SLBs account for only 5 per cent of all green and sustainable bonds issued and listed worldwide and why issuances have been waning (see chart below).

“Issuers face the challenge of setting targets that are ambitious enough to demonstrate credibility in their sustainability journey, yet realistic enough to be achievable,” the LGX says.

LGX also notes that the “share of SLB issuances from hard-to-abate and fossil fuel sectors is well above other sustainable bonds, highlighting the critical need for a robust target-setting system and effective monitoring”.

While acknowledging that financing the transition of high-emitting companies “raises concerns about reputation and greenwashing” LGX argues “these are exactly the industries that require substantial investment to successfully transform their business models”.

Target shooting

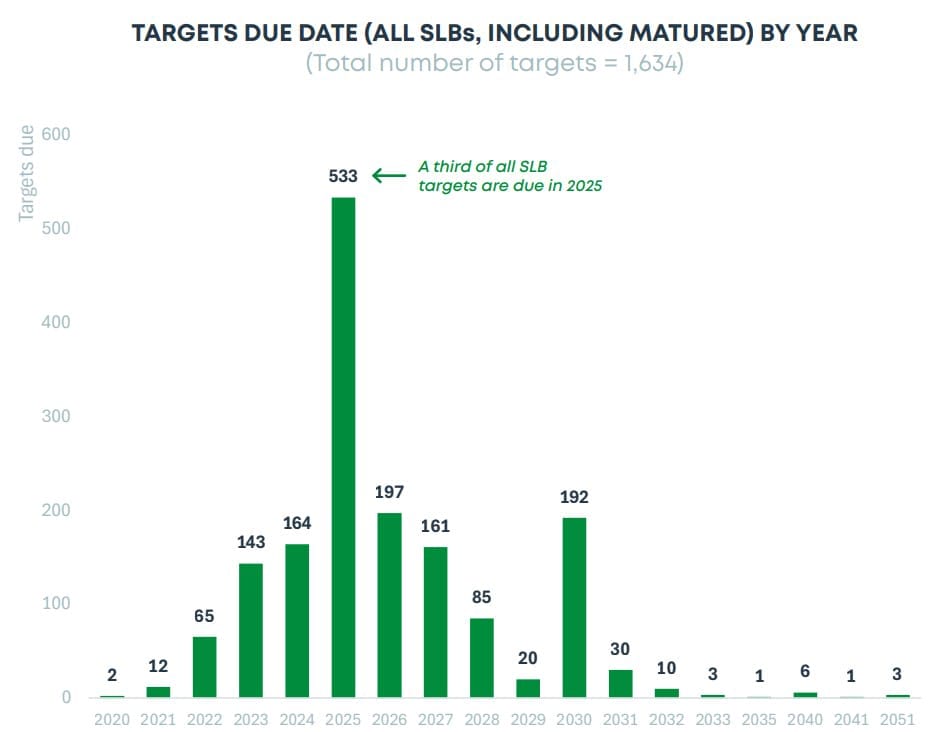

This year will be a crucial one for SLBs. LGX estimates one-third of all the SPTs for all the bonds that have been issued are due in 2025 (see chart below).

LGX says the majority of SLB targets to date have successfully been met and claims most of “the relatively few missed targets are attributable to exceptional and often geopolitical circumstances”.

An alternative explanation is that this just reflects how unambitious many of the SPTs are, and the ease with which targets can be revised and manipulated.

The first SLB was issued in January 2009 by Italian multinational energy company Enel, which is also the largest SLB issuer, accounting for 14 per cent of the total outstanding SLB volume through around 50 issuances.

So it was a big deal for the SLB market when Enel revealed early last year that it had not met its 2023 Science Based Targets Initiative (SBTi)-certified Scope 1 Power Generation Intensity target relating to ten SLBs.

In its 2025 Sustainability-Linked Financing Framework, Enel explained that it did not meet its target because “the recent global energy crisis, exacerbated by the Russian-Ukrainian conflict, led to European governments mandates requiring Enel to maximize coal-fired electricity production”.

Enel confirmed that a 25 basis point penalty rate would apply to these bonds, resulting in what is estimated to be an additional €25 million ($41 million) in annual interest expenses for the company.

This event was viewed by SLB supporters as proof the SLB market was functioning as intended, with ambitious SPTs being set and with issuers actually paying “step-ups” if they were not met.

Enel said “the activation of the step-up mechanism proved that the Sustainability-Linked format is robust and meaningful, challenging companies to adjust their trajectory to the committed sustainability targets”.

Enel has since issued further SLBs which have been well received by investors and the company says it is on-track achieve its decarbonisation goals.

Wesfarmers

Australia’s first SLB was launched in 2021 by Wesfarmers, which now relies on sustainability-linked financing for almost 80 per cent of group funding.

Under its first $1 billion SLB (issued in two tranches) Wesfarmers committed to running its Bunnings, Kmart Group and Officeworks retail businesses on 100 per cent renewable energy by the end of 2025 and limiting the average emissions intensity of its ammonium nitrate production plant. Each of these SPTs has a 12.5 basis point step-up if not met.

Wesfarmers seems to have met the ammonium nitrate SPT, but investors will be waiting for its SPT progress report to see if it is on track to meet the renewable energy target.

In an unfortunate aside, investment bond scammers have been impersonating Bunnings. Earlier this month the Australian Securities and Investments Commission (ASIC) warned consumers that scammers were offering fake “Bunnings Sustainability Bonds”.

Enbridge

North American energy infrastructure company Enbridge is a good example of why SLBs have an image problem.

Back in 2023 Enbridge, whose core business is petroleum pipelines, processing and storage facilities, issued US$2.3 billion in sustainability-linked senior notes due 2033 (see image below).

When issuing the notes Enbridge set itself a target of a 35 per cent reduction in GHG intensity by 2030 per cent compared to a 2018 baseline year.

However, by the end of 2021, Enbridge had already achieved a reduction of 27 per cent relative to the baseline year, making its SPT seem a little unambitious.

The GHG intensity SPT covers only covers scope 1 and 2 emissions, whereas the great bulk of Enbridge’s emissions would be scope 3 (combustion by end users).

When issuing the SLB, Enbridge made it clear that it did not intend to direct proceeds to “projects or business activities meeting environmental or sustainability criteria”.

True to its word, last year Enbridge announced a US$700 million investment to build, own and operate crude oil and natural gas pipelines in the Gulf of Mexico (or the Gulf of America for those who acknowledge US President Donald Trump’s executive order to “restore names that honor American Greatness”).

JBS

Another big SLB issuer with highly dubious sustainability credentials is Brazil’s JBS, the world’s second largest food group and largest meat processor. Since April 2021 JBS has issued three SLBs, raising US$3.5 billion.

Over the last couple of years NGOs (such as Forests & Finance, Mighty Earth and Greenpeace), US senators and other groups have been targeting JBS for its highly questionable net zero emission claims; links to deforestation in Brazil; labour rights violations; and governance issues (including past bribery and corruption scandals involving its controlling shareholders).

JBS says it is committed to achieve net zero across its global value by 2040 but makes the rather preposterous claim that will accomplish this by (amongst other things) “eliminating deforestation in the Amazon (and illegal deforestation from our supply chain in all Brazilian biomes) by 2025”.

JBS’ detractors question why investors such as Fidelity, BlackRock and Vanguard have been supporting the company’s SLBs and how the SLBs can credibly sit in their “sustainable” investment portfolios.

Sustainability-linked loans

Meanwhile, sustainability-linked loans (SLLs) are also under the microscope. SLLs operate much the same as SLBs but instead of being issued to investors, loan funds are provided by banks. Often the interest rate adjustment on an SLL can be up or down, depending on whether targets are met.

In the UK, the Financial Conduct Authority (FCA) has been reviewing the SLL market for some time because of “credibility, market integrity and greenwashing concerns”. The FCA is worried that most SLL transactions were not fit for purpose and that KPIs were not robust enough.

An FCA report said there is “a general sentiment among banks that the ‘relationship’ may matter more than the borrower’s sustainability credentials – the former may therefore disproportionately drive the bank’s decision to participate in the loan”.

“Stakeholders observed that a number of banks seem keen to promote SLLs – in some cases additionally incentivised by remuneration linked to achieving ESG financing targets,” it said.

“This may give rise to a potential conflict of interest, encouraging the bank to accept weak SPTs and KPIs.”

ISPT

Australian groups with SLLs include ISPT, Ramsay Health Care, Cromwell Property Group and Inghams.

Last year property fund manager ISPT arranged a $1.5 billion sustainably-linked syndicated term loan, lifting its total SLLs to $5.75 billion. The latest SLL is tied to ISPT’s existing sustainability performance targets covering metrics in GHG emissions intensity, waste reduction, water consumption and labour certification.

ISPT (co-founded in 1994 by AustralianSuper, Cbus and HESTA) was acquired by IFM Investors via a scheme of arrangement in December 2024. IFM in turn is owned by 16 Australian industry super funds and is now welcoming major UK pension fund Nest as a 10 per cent shareholder.

IFM itself has also been dabbling in SLLs. Its 2024 Sustainability Report says IFM gave an SLL to a “provider of safety services to offshore vessels in the North Sea” (believed to be North Star).

The SLL is linked to the company transitioning away from the oil and gas sector by “increasing the company’s revenue from offshore wind in the UK” and adding “vessels dedicated to offshore wind servicing”.

Leave a Comment

You must be logged in to post a comment.