Brandolini’s Law – also known as the “Bullshit Asymmetry Principle” – states that the amount of energy needed to refute bullshit is an order of magnitude bigger than that needed to produce it.

So, late last month when the Bitcoin Policy Institute released a lengthy report titled “Brandolini’s Law in Action. An Analysis of the United Nations University’s Bitcoin Mining Commentary, it was making its view on the commentary clear.

The Institute took great exception to the university’s study The Environmental Footprint of Bitcoin Mining Across the Globe: Call for Urgent Action, saying it was yet another example of flawed research into Bitcoin mining’s energy usage and had “overlooked extant literature suggesting Bitcoin mining could be a benefit to electric grid reliability and the renewable energy transition”.

The Institute and other Bitcoin supporters argue that far from Bitcoin mining being a climate problem (e.g. the repeatedly reported assertion that mining produces higher emissions than many countries) it should be seen as an integral part of the climate solution.

In fact Bitcoin miners are now presenting themselves as climate and ESG champions, citing the many ways they are able to support investment in renewable energy projects, reduce GHG emissions and promote social inclusion around the world.

So, what are bitcoin miners’ claimed climate/ESG credentials? The Institute of Risk Management’s (IRM) Bitcoin and the Energy Transition: From Risk to Opportunity study and other similarly-focussed reports say Bitcoin miners promote a clean energy future by:

- Relieving the strain on grids when more electricity is generated than consumed by using the excess power for mining. Conversely, miners can also quickly and efficiently turn off their machines during periods of heavy demand, thus contributing to grid stability.

- Being a flexible load option Bitcoin mining helps solve the intermittency and congestion problems of wind and solar projects.

- Purchasing energy during the pre-commercial operation phase of a renewable energy projects. Integrating mining with planned renewable installations enhances their economics and ability to attract financing.

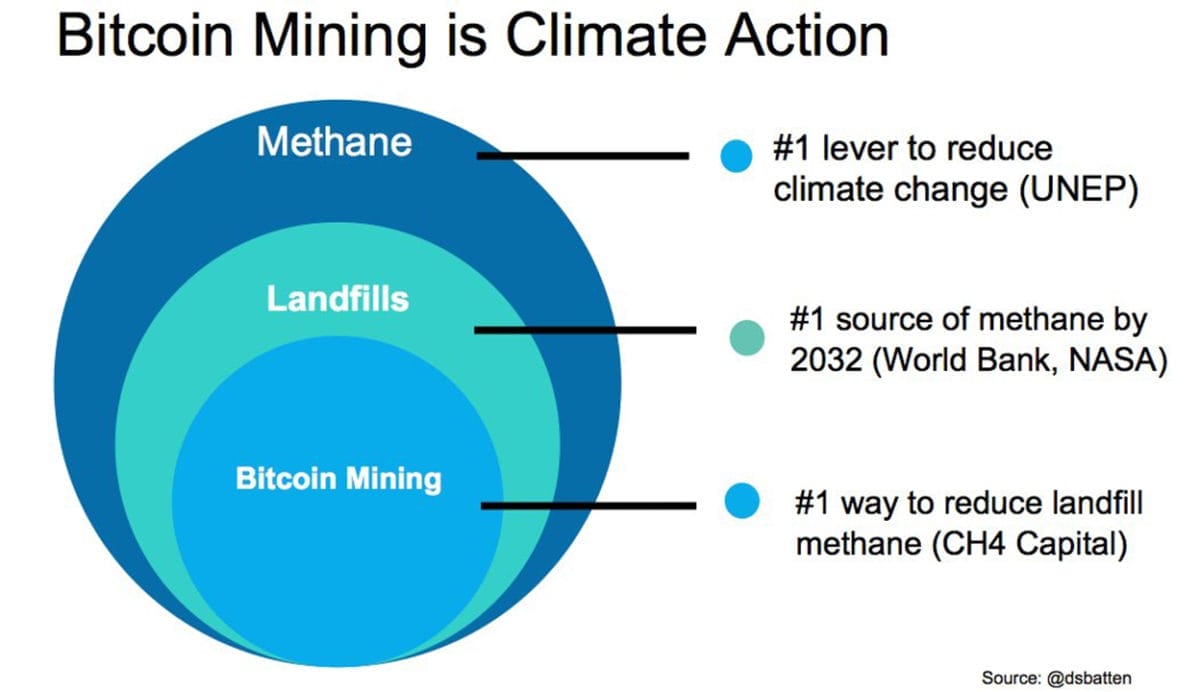

- Capturing methane from trash landfills (see graphics below) and converting it into biomass energy to mine bitcoin and/or power other data operations.

- Using methane that would otherwise be flared from oil wells to power mobile, on-site containerized computers performing Bitcoin mining.

- Being an economic enabler to marginal hydroelectric, geothermal, and nuclear energy projects, acting as a buyer of first or last resort.

- Recycling the significant heat generated by mining rigs for heating purposes in homes, commercial buildings, greenhouses etc.

IRM says “as Bitcoin and energy markets continue to converge it is likely that the energy infrastructure owners and miners will vertically integrate. The emerging synergy between Bitcoin mining and energy production continues to gain traction and instead of being seen as a villain by those who advocate for a sustainable green future, it will instead come to be seen as an enabler of that future”.

Bitcoin miners are also broadening their horizons. For example, Singapore-based and Nasdaq-listed Bitcoin miner Bitdeer Technologies and the Bhutanese government’s commercial arm Druk are jointly developing “environmentally sustainable, carbon-free digital asset mining operations” in Bhutan.

They are establishing a US$500 million ($760 million) fund to invest in “hydropower, green ammonia and the hydrogen fuel economy” an also “blockchain, artificial intelligence, machine learning systems, carbon credit platforms and the metaverse”.

Bitdeer is run by Chinese entrepreneur Jihan Wu who co-founded Bitmain , the world’s largest manufacturer of cryptocurrency mining hardware.

Disputed credentials

If all the above sounds too good to be true, it probably is. It should come as no surprise that all of Bitcoin’s claimed climate/ESG credentials are disputed or doubted by various groups. For example, capturing methane from oil wells has been branded as ‘greenwash’ supporting the fossil fuel sector. Oil majors such as Exxon Mobil and ConocoPhillips are reportedly looking at Bitcoin mining to extract further profits from their operations.

The claimed power grid benefits are largely based on miners’ involvement in the Electric Reliability Council of Texas (ERCOT) program where they have been accused of negotiating cheap wholesale energy contracts and then reselling energy at a premium to Texans needing to stay warm in winter.

Ruthless profit-maximising entities

Arcane Research’s report How Bitcoin Mining Can Transform the Energy Industry says because miners are location agnostic they are the perfect customers of previously stranded energy resources being able to set themselves up at the energy source.

Bitcoin miners produce a commodity that can’t be differentiated and can only compete on costs and “ruthless competitive forces will gradually erase miners’ profit margins, except for those with access to exceptionally cheap electricity”.

“As profit-maximizing entities, miners will leave no stone unturned in their hunt for cheaper electricity,” Arcane notes.

“By getting paid to stabilize the grid, selling waste heat, or offtaking stranded natural gas or renewables, a miner can achieve significantly lower electricity costs than a miner who passively draws energy from the grid.”

Bitcoin’s ‘halving’

Staying profitable is about to get a whole lot harder for Bitcoin miners.

In April this year the next much-anticipated ‘halving’ of Bitcoin is estimated to occur. Bitcoin halving refers to a planned reduction of the mining reward on the Bitcoin network that occurs each time 210,000 blocks are mined. Halving happens as part of the Bitcoin’s proof-of-work (POW) protocol’s design and is a key mechanism to control the supply of new Bitcoin.

When Bitcoin first launched in 2009, the mining reward was 50 Bitcoins per block. The April halving will cut the reward down to 3.125 per block (This halving continues until the block reward becomes less than one Satoshi, the smallest Bitcoin unit (0.00000001 Bitcoins).

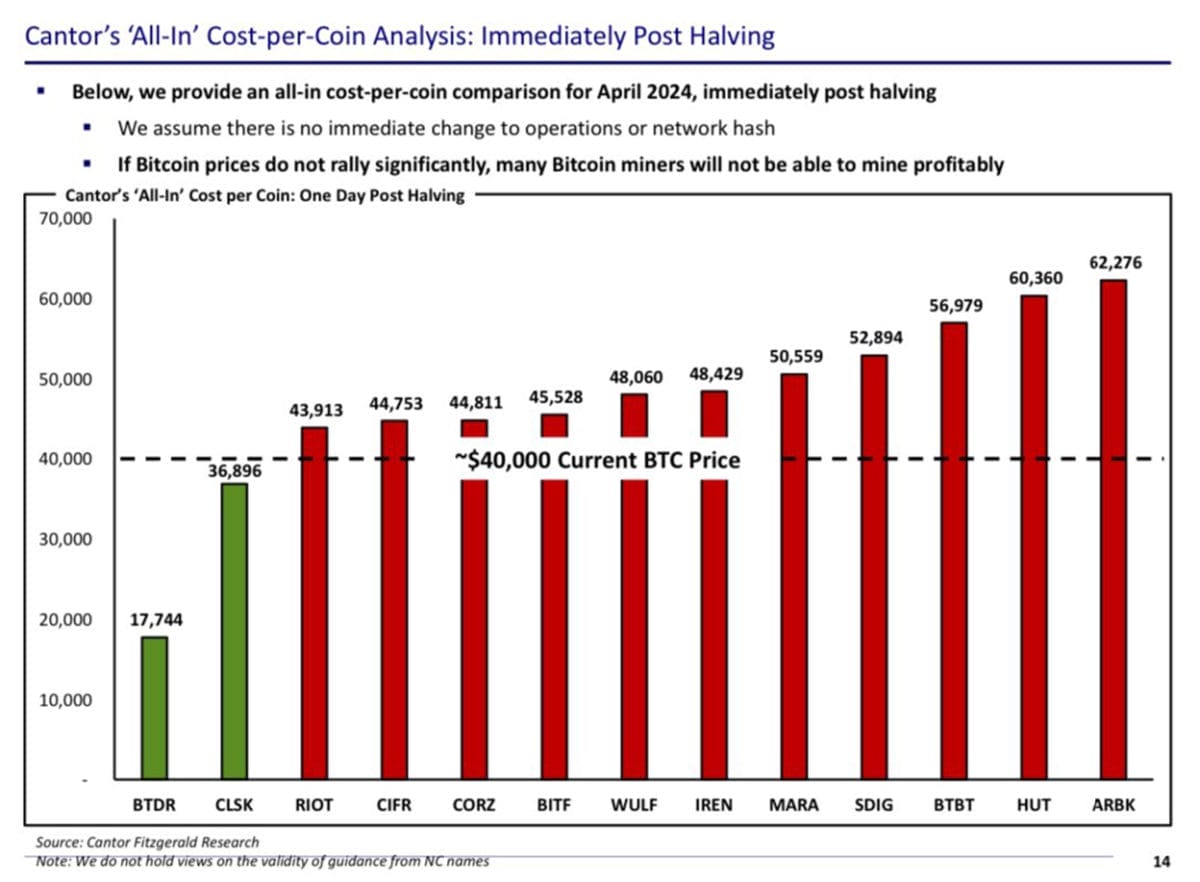

Latest research from US brokerage firm Cantor Fitzgerald (see below) suggests that most of the major listed Bitcoin miners will not be able to operate at a profit after the next halving based on Bitcoin’s current price.

Miners will be hoping that because halving restricts the supply of new Bitcoins this will boost Bitcoin’s price.

Jeopardising the network

This also has much broader ramifications that could threaten the entire Bitcoin network.

BlackRock’s prospectus for its recently approved Exchange-Traded Fund (ETF) in the US explains the problem. The prospectus says this reduction in mining rewards means miners may no longer be incentivised “to continue to perform mining activities, thereby jeopardizing the security of the Bitcoin network”.

The resultant “reduction in the processing power expended by miners on the Bitcoin network could increase the likelihood of a malicious actor or botnet obtaining control”.

If miner rewards are no longer sufficient to ensure profitability, miners may demand higher transaction fees for recording transactions in the Bitcoin blockchain which means the cost of using Bitcoin would rise “and the marketplace may be reluctant to accept bitcoin as a means of payment”.

The prospectus says “any widespread delays or disruptions in the recording of transactions could result in a loss of confidence in the Bitcoin network”.

Big asset managers back the miners

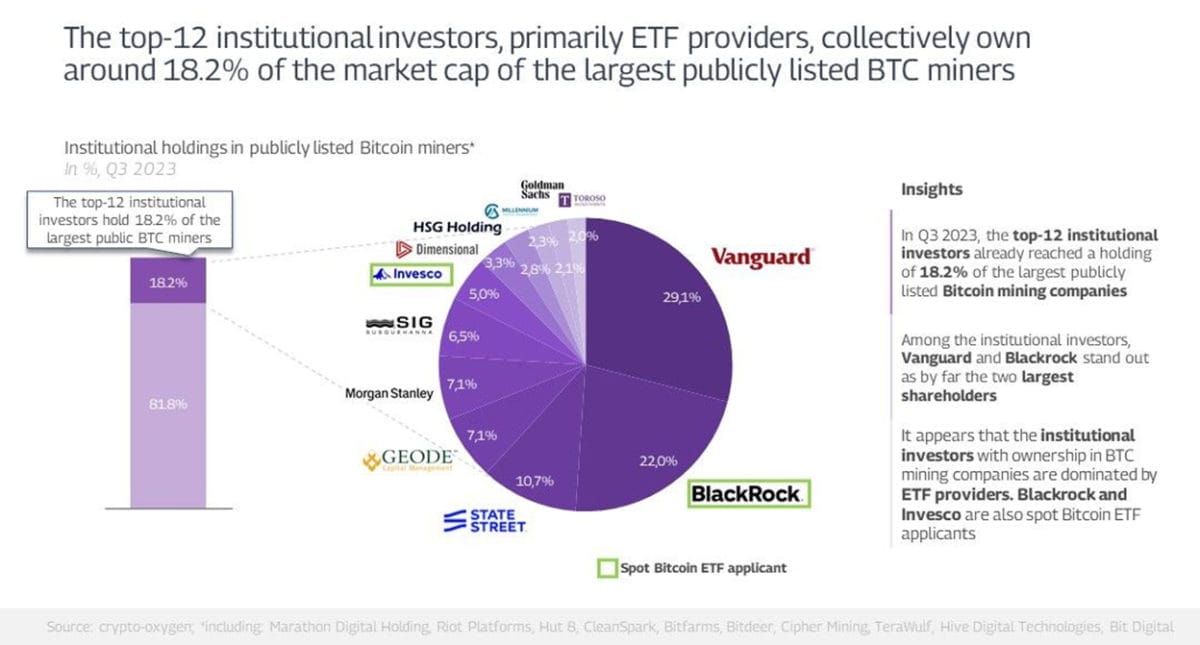

Despite all these risks some of the world’s largest asset managers such as BlackRock and Vanguard are large shareholders in the biggest listed Bitcoin miners (see graphic below).

In Vanguard’s case this seems a little bizarre. Vanguard has significant shareholdings in miners such Marathon Digital, Rio Platforms, CleanSpark and Terawulf.

However, unlike BlackRock, it did not launch its own Bitcoin ETF. Explaining why, Vanguard said last month that “when deciding what investment products to offer, we consider a range of factors, including whether we believe they have enduring investment merit”.

“In Vanguard’s view, crypto is more of a speculation than an investment,” it said.

“While crypto has been classified as a commodity, it’s an immature asset class that has little history, no inherent economic value, no cash flow, and can create havoc within a portfolio.”

So why is Vanguard a big investor in companies that are rewarded in Bitcoins but less enamoured with Bitcoin itself. The answer appear to be that passive index tracking has led to them accumulating these mining stocks.

Brandolini’s Law

Vanguard’s concerns are shared by US SEC chair Gary Gensler.

In his Statement on the Approval of Spot Bitcoin Exchange-Traded Products (ETPs) Gensler said that “though we’re merit neutral, I’d note that the underlying assets in the metals ETPs have consumer and industrial uses, while in contrast Bitcoin is primarily a speculative, volatile asset that’s also used for illicit activity including ransomware, money laundering, sanction evasion and terrorist financing”.

Given what the Bitcoin community no doubt thinks of Gensler’s and Vanguard’s statements we may soon see Brandolini’s Law in action again.

Leave a Comment

You must be logged in to post a comment.