The Panguna mine was one of the world’s largest copper and gold mines until civil war broke out in Bougainville, closing the mine in 1989.

Each quarter ASX-listed Bougainville Copper (BCL), which was handed ownership of the mine in 2016 by former owner Rio Tinto, dutifully reports that “there has been no production since 15 May 1989”.

In May this year the Panguna Mine Action group launched class action proceedings against both BCL and Rio on behalf of Bougainville residents over the devastating environmental and social harm caused by Panguna.

Meanwhile, earlier this month, the governments of Papua New Guinea and the Autonomous Region of Bougainville appointed former New Zealand governor-general Sir Jerry Mateparae as independent moderator for Bougainville’s drawn-out push for full independence.

ESG and the JORC Code

There is probably no better – or sadder – example than Panguna of how environmental, social and governance (ESG) factors are just as important to the development and ongoing viability of a minerals project as the size and grade of its mineral deposits.

Of course, ESG factors are important for investors in assessing every mining project. This is why the long-awaited proposed changes to the Australasian Joint Ore Reserves Committee (JORC) Code will see all ASX-listed minerals explorers and producers having to report more explicitly on how ESG factors are impacting/influencing their projects.

The Committee says the new draft code “reflects evolving societal and regulatory expectations with respect to progression of new projects through to development”.

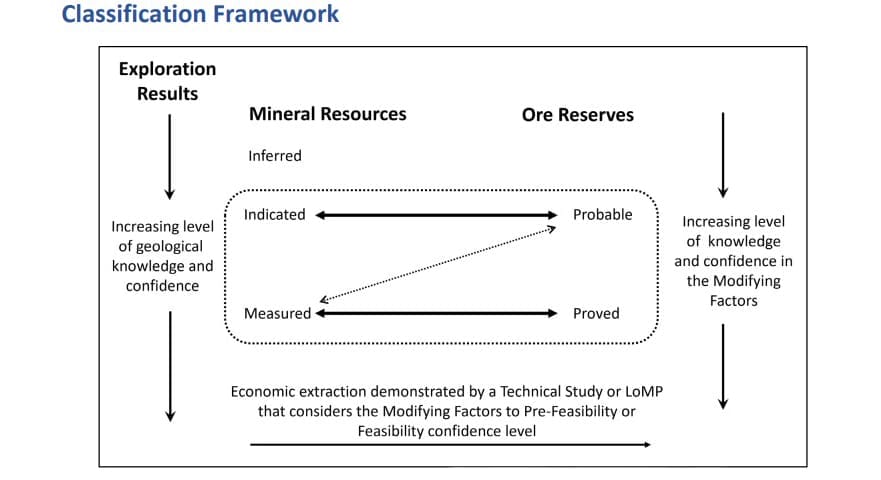

Under the proposed updated code “equal prominence” will now need to be given to ESG factors alongside other “modifying factors” such as mining, processing, metallurgical, infrastructure, economic, marketing, legal and regulatory factors that are used to assess and estimate exploration targets, mineral resources, and ore reserves. The proposed JORC Classification Framework is shown below.

Code Guidance

The guidance provided on the draft code says “all modifying factors must be treated as potentially equally important to project development”.

“While geological data develops necessarily ahead of many other elements, it is not appropriate to leave out from consideration emerging material data across the modifying factors in a company’s public reporting,” it says.

The guidance says the reporting requirement “does not presume mature knowledge for early-stage projects, and only requires available and material data to be considered, as it is for all other modifying factors”.

“While the yet unknown cannot be considered, the material known must always be assessed,” it says.

For example, the guidance says, “an environmental risk may be clear from day one of an exploration project. An example would be, if the northern one third of your lease is a prescribed wetland then you have to manage and disclose that from the very beginning”.

As a mining project progresses (matures) the JORC Code will be expecting more detailed reporting on risks associated with “social licence” including land owner and stakeholder engagement; proposed energy sources; greenhouse gas emissions; access to water; waste disposal, mine closure and mine rehabilitation.

Reasonable prospects for economic extraction (RPEE)

There is one small proposed change in the draft that could have big ramifications for mining projects.

It is proposed that the word “eventual” be removed from the code’s existing terminology “reasonable prospects for eventual economic extraction”.

This is because some companies have been relying too much on the word “eventual” to justify the mineral resources and ore reserves they have reported, without putting any timeline on what “eventual” means and not adequately explaining why they think their reporting is “reasonable”.

Some project proponents have viewed “eventual” as meaning some time in the next 50 years – a timeline beyond the investment strategy of even the most long-term investor.

The Committee says stakeholder feedback “saw the need for greater consistency as to how RPEE is communicated in public reports’ and the proposed code change “attempts to clarify that the intention was not to allow unreasonably long delayed starting points”.

A tailings tale of woe

The current woes of ASX-listed explorer Regis Resources highlight the importance of ESG factors and perhaps also how companies address RPEE.

In July, Regis released the Definitive Feasibility Study (DFS) for its McPhillamys Gold Project showing it to be a “long-life, low operating cost, organic growth opportunity with robust financial metrics”.

But in August Environment Minister Tanya Plibersek shocked the company with her decision to make a Section 10 declaration under the Aboriginal and Torres Strait Islander Heritage Protection Act 1984 that prevents construction of the planned tailings dam for the project.

Regis said the Section 10 declaration meant the DFS outcomes could no longer “be relied upon by investors when making investment decisions”, as the project may no longer be viable.

The company said “the McPhillamys ore reserves have been reassessed resulting in the withdrawal of the 1.89 million ounces ore reserves previously associated with the project”.

Having undertaken a review of the reasonable prospects of eventual economic extraction of the deposit, Regis has concluded that “while the risk profile has changed considerably, for the purposes of establishing a Mineral Resource Estimate the key assumptions remain valid and unchanged”.

Regis is investigating other tailings storage options but says “it is reasonable to consider a timeline of five to 10 years for these studies to achieve permitting when a suitable option is identified”.

It is very unlikely the ESG requirements of the new code would have led to the tailings dam issue being flagged earlier.

Given the various approvals and consents Regis had received, the Minister’s late-stage declaration was genuinely unexpected and probably could not have been reasonably foreseen.

Confidence

The experience of Regis – whose substantial shareholders include Australian Retirement Trust, First Sentier Investors and State Street – is also a reminder that project risk does not necessarily decrease as more time, effort and money is poured into a project.

JORC’s Classification Framework and also its Risk and Opportunity Guidance Matrix are based on the “general relationship between exploration results, minerals resources and ore reserves”.

They assume technical and sustainability risk decreases as knowledge of and confidence in the modifying factors increases. What they don’t allow for is when this ‘confidence’ proves to be misplaced.

Sticking point

The draft code’s requirements for reporting ESG modifying factors more systematically and transparently do not represent any sort of “woke” or “green” agenda but are something that should help both investors and their investees.

It should make it easier for investors to more holistically assess the risk factors associated with a mining project, while explorers should see it as an opportunity to better understand their own projects.

But some in the mining community are questioning why reporting on ESG factors has to happen in document that is about estimating and updating mineral resource and ore reserve estimates.

King & Wood Mallesons (KWM) notes that the code’s “proposed additional requirements, centred on ESG factors, are causing concern among some mining and exploration industry bodies” such as the Association of Mining and Exploration Companies (AMEC).

This is because the inclusion of such factors for consideration by the “competent person” who has to prepare public reports “may be extending the JORC Code beyond its intended function, and overlapping with the relevant entity’s governance and other obligations to consider and manage ESG risks”.

KWM says “our sense is that this set of proposed changes, and the extra responsibility that it imposes on a Competent Person, may be a key ‘sticking point’ in ensuring that the updated Draft JORC Code secures broad acceptance across the industry”.

More support for the juniors?

It will be interesting to see if the more detailed ESG reporting requirements will help the ASX’s very long list of junior explorers attract more capital from institutional investors.

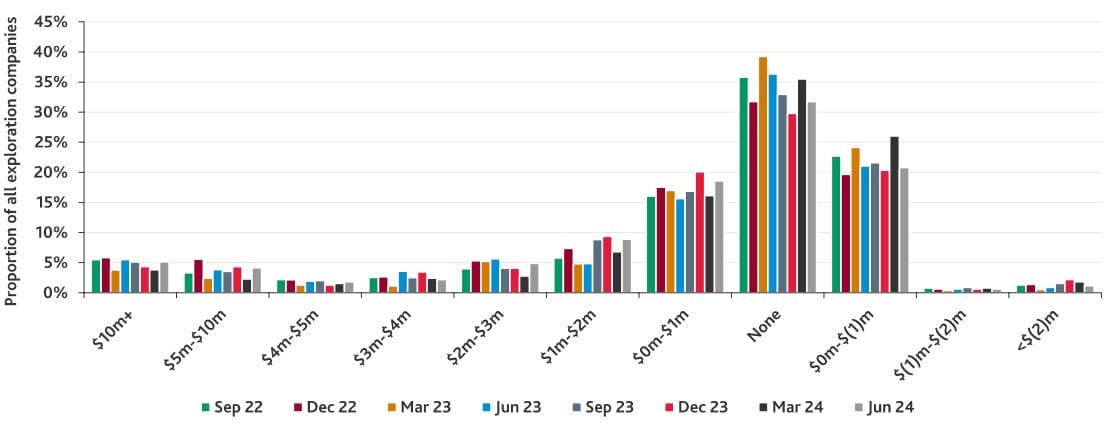

BDO Australia’s latest Explorer Quarterly Cash Update showed that in the June quarter a total of $2.95 billion in debt and equity was raised by the ASX’s 775 mineral and petroleum explorers.

However, BDO’s report showed that just 47 companies – or just six per cent of all the explorers – raised 77.9 per cent of this funding. The standout was De Grey Mining whose $600 million equity raising was strongly supported by institutional investors.

The diagram above shows that just over 50 per cent of junior explorers reported either no – or less than $1 million in – net financing inflows in the June 2024 quarter.

In the June quarter more 60 per cent of junior explorers spent less than $500,000 on exploration, while the proportion of companies reporting nil investing cash flows (that is, expenditure on project development excluding exploration) was only 41 per cent.

This indicates junior explorers are taking a conservative approach, focusing on preserving cash and deferring investments in an inflationary and uncertain economic environment.

A number of these companies own highly prospective deposits with minerals that are in high demand but which risk not being developed in a timely way if institutional and other investors continue to shun most of them.

Leave a Comment

You must be logged in to post a comment.