Australian superannuation funds’ investment models have evolved considerably since the genesis of the system four decades ago, and they continue to adapt to suit changing markets and to cater to member demands.

But from an analysis of how funds have developed over 40 years, it’s clear that there’s no consensus on the “best” way to manage members’ money, let alone a model than can be described as “the Australian way”.

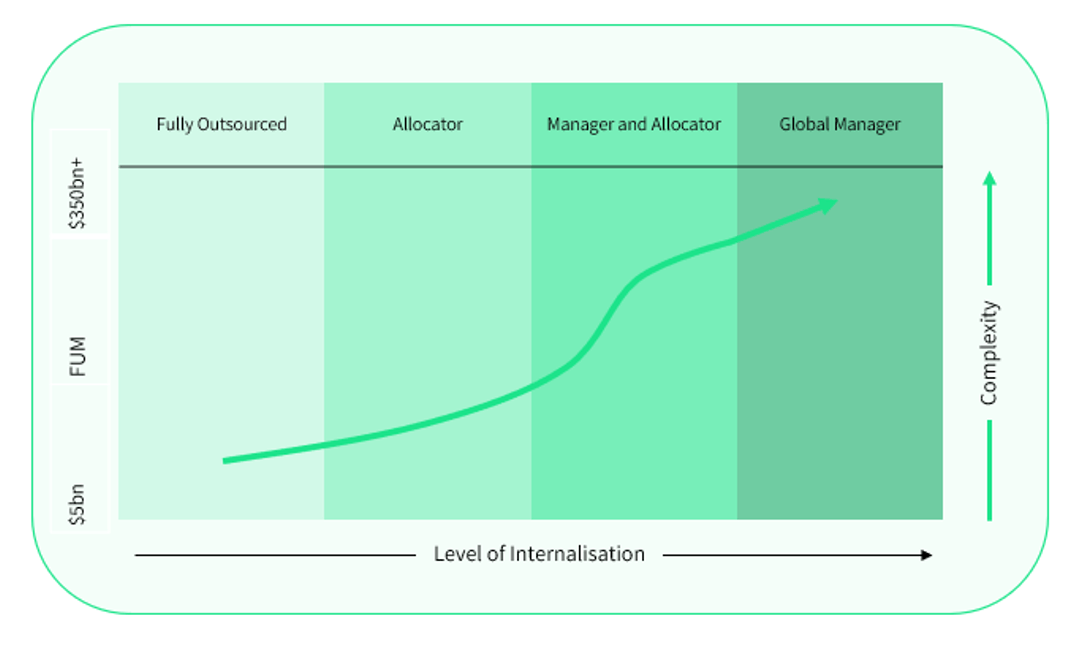

The paper, published by 1886 Consulting managing director Doug Talbot ahead of the Investment Magazine Fiduciary Investors Symposium starting tomorrow, suggests there are four principal investment models operating in the industry: fully outsourced; investment allocator; manager and allocator; and global manager.

“This paper is not intended to pit one against another but to simply show there are different characteristics to each model,” it says.

“We have looked to outline at a high level the governance, talent and technology complexities of insourcing functions, noting they should not be underestimated by trustee boards, CEOs or CIOs. There are multiple second- and third-order consequences of internalisation that, on the surface, may seem like simple decisions to make.”

The paper suggests funds trustees should consider a range of factors, including how engaged members are with the fund’s investment beliefs, strategy and model.

“What are they expecting you to do with their capital?” the paper says. “Are they financially literate enough to care, or do you just need to produce a return that is broadly competitive with peers?”

It says trustees should also carefully consider a fund’s approach to product innovation, operational excellence and customer intimacy, and determine just how real those points of difference are with other funds.

One size won’t fit all

Each of the investment models has strengths and weaknesses, the paper says, and “no one size fits all – each funds needs to be set up within its own context”.

The consulting firm says 10 to 15 years ago, most funds operated a fully outsourced model, some were building investment-allocator capabilities, and a few of the larger funds were moving towards the manager-and-allocator model.

A prominent feature of Australian funds’ evolution since then has been the growth of insourced asset management and a move to the global manager model, and in this respect at least the evolution mirrors the development of the Canadian pension fund market.

The 1886 paper says the Canadian model is “regularly considered the global pension fund benchmark of Investment models due to their size, scale, asset diversification and sophistication”. It adds that a 2017 World Bank study of the system distilled the model down to four principal characteristics: comparative advantage; in-house management; diversification; and managed risks and liabilities.

But there are some differences between Canada and Australia that trustees should be wary of and which put a different perspective on the global manager model for local funds.

For example, “the Canadian example suggests the global manager model prevails”, the 1886 paper says.

“However, fees are not a constraint in Canada; therefore, remuneration alignment to attract and retain top talent and establish global manager capabilities in-region is easier.”

Complexity is not linear

The paper says that its “experience-based thesis” suggests that as Australian funds in-source more capabilities, the “level of complexity in governance, talent management and data and technology grow significantly” – but that the relationship between in-sourcing and complexity is not linear.

The paper says the fully outsourced model has “minimal internal investment capability, with the trustee board more reliant on asset consulting services being provided throughout the Investment process”.

“Overall, the people, process and technology complexity and cumulative operational risk are relatively low in this model,” it says.

Meanwhile, investment allocators focus on selecting external managers, and the internal capabilities built by the fund are aimed at supporting manager selection and operational due diligence.

“This model continues to be very common in Australia and is not only in place for almost all smaller funds but some larger funds as well,” it says.

In this model, the people, process and technology complexity, as well as the cumulative operating risk, are moderate, although “this increases with diversity of asset allocation and FUM growth”.

“Many funds we today call “mega funds” moved into this stage more than 15 years ago,” the paper says.

The manager-and-allocator model is a hybrid in which the fund is manager of some asset classes and outsources others.

“Many funds in Australia when they reach approximately $60b see some scale benefits to moving to this model,” the paper says.

“Overall, the people, process and technology funding, complexity and cumulative operational risks increase substantially in this model.”

These risks increase again when a fund evolves to the global manager model and are broadly equivalent to the risks present in any large, multi-asset global manager.

“Global Managers not only build out deeper investment capability, but they do this on a global scale,” it says.

It’s at this point that “some of the megafunds in Australia have seen opportunity to emulate characteristics of the Canadian Model,” the paper says.

Leave a Comment

You must be logged in to post a comment.