With opposition leader Peter Dutton swinging his nuclear nunchuks there may be fresh brawling in coming months over the future of uranium mining in Australia.

The acrimonious debates over the decades about uranium have tended to generate more heat than light, and left a mining-reliant country that sits on 28 per cent of the world’s uranium resources producing only 9 per cent of the globe’s uranium. This is fantastic for some but frustrating for others.

But it will probably be events playing out on the other side of the uranium universe involving some small Australian companies that will be more intriguing – and perhaps informative and insightful – over the coming months.

Trump’s Greenland

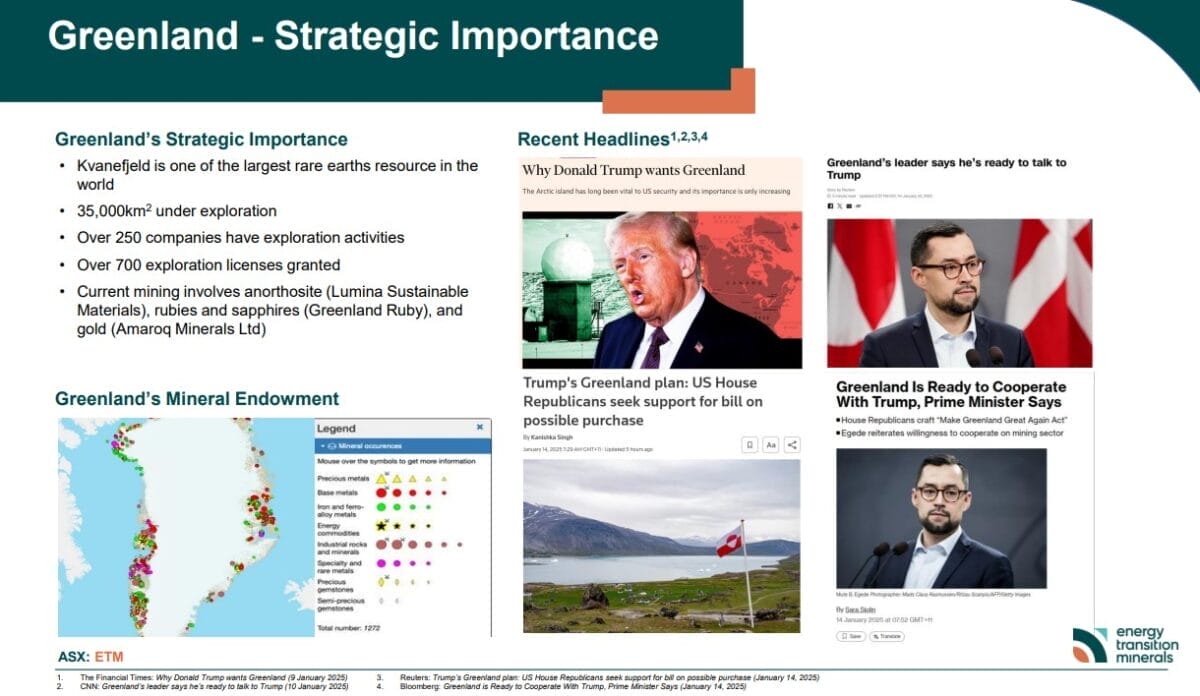

Last month ASX-listed Energy Transition Minerals (ETM) announced it had engaged Julie Bishop & Partners to help its advance Kvanefjeld Rare Earth Element Project in Greenland which hosts a world-class uranium resource.

ETM of course has been in the news because it is an Australian angle to US President’s Donald Trump stated desire to purchase Greenland – or to take control of it by some other means.

Greenland is an autonomous territory of Denmark. Greenlanders want independence from Denmark and don’t want to be controlled by the US. Denmark says Greenland is not for sale (and if it were to be, apparently Britain has a right of first refusal).

Danish politician Anders Vistisen put it succinctly in European Parliament “Let me put it in words you might understand. ‘Mr. Trump, f–k off’!”

Risky business

Asset owners with a history of investing in companies developing resource projects abroad are well aware of the political and other risks that can encountered.

But here we aren’t talking about the potential for a military coup, in say, a developing African nation, but the (hopefully improbable) prospect of a NATO country seizing a territory from another NATO member and a close ally.

ETM is not taking sides but it has noted that Greenland is “geographically part of North America” and that Greenland’s capital, Nuuk, “is closer to New York than Copenhagen”.

Usually, political risk issues would have a negative impact on the share prices of companies operating in the risk zone but in this case the opposite has been happening.

No doubt this reflects speculation/expectations that a Trump-led US government would be keen to see Greenland’s minerals wealth exploited – and without much concern for environmental and other issues (the melting ice in southern Greenland caused by climate change makes it easier to access the country’s minerals wealth).

ETM has been in dispute with the Greenlandic authorities since December 2021 when the Greenlandic Parliament passed Act. No. 20 (the Uranium Act), preventing ETM from further developing Kvanefjeld or progressing its application for an exploitation licence.

The Uranium Act prohibits exploration for or production of uranium above a 100 ppm threshold and Kvanefjeld deposit is over 300 ppm. So this means the entire project is stalled.

China syndrome

Another complicating factor that may come into play given Trump’s ambitions is that one of ETM’s largest shareholders in China’s state-owned Shenghe Resources, which has an offtake agreement for Kvanefjeld’s output.

So, while if Trump were to grab Greenland he may be keen to exploit its minerals wealth – which boasts most of the critical minerals the US desires – he may be less keen on supporting projects that may not be seen as helping to break China’s stranglehold on critical minerals.

ETM says Bishop’s “profound grasp of international and geostrategic affairs will enable her to provide invaluable support and counsel to the Board of ETM in negotiating a win-win solution for all stakeholders and addressing the challenges faced in advancing” the Kvanefjeld project.

However, it is fair to say Trump is not really a “win-win” sort of guy but someone who needs to be able to identify the loser(s) in a transaction.

Sweden lifts ban

Meanwhile, ASX-listed Aura Energy is celebrating the news that Sweden is moving in the opposite direction to Greenland and is lifting its ban on uranium mining.

One of Aura’s assets – apart from having former ALP President and recent Liberal Party candidate – Warren Mundine on its board – is the Häggån project, a polymetallic resource containing a lot of uranium.

Aura, which has been focused on developing its Tiris Uranium Project in Mauritania, estimates that based on Sweden’s current uranium usage, the Häggån resource “could fuel Sweden’s existing nuclear reactor fleet for over three centuries”.

Aura says “Sweden has a rich geological endowment that can be harnessed to provide zero emissions nuclear power for both its own domestic use, as well as for export”.

Sweden’s Ministry of Climate Change and Enterprise says “more than a quarter of Europe’s known resources of uranium are in Sweden’s bedrock. Being able to mine uranium is absolutely necessary for our work with the climate transition”.

Sweden’s Minister for Climate and Environment Romina Pourmokhtari says “I want us to mine and make use of the mineral found in Sweden, where the Swedish mining industry is among the most environmentally friendly and safe in the whole world”.

All parties in the governing coalition, which holds a majority of the seats in Parliament, have expressed support to overturn the ban. There are still a few steps in the legislative process including wide consultation but the aim is for the lifting of the ban to come into effect on 1 January 2026.

Sweden’s nuclear history

The political history of Sweden’s nuclear industry, which provides about 40 per cent of the country’s electricity is interesting.

In 1980, the government decided to phase out nuclear power. But in June 2010 this policy was repealed and replaced with a policy to begin replacing the country’s old reactors.

In June 2023 Sweden changed its energy target of ‘100 per cent renewable’ electricity by 2040 to ‘100 per cent fossil-free’ electricity

The country now proposes to construct two large-scale reactors by 2035 and the equivalent of 10 new reactors, including small modular reactors, by 2045. These timelines show how long it takes to bring on new nuclear capacity, even in a country that has an established nuclear industry.

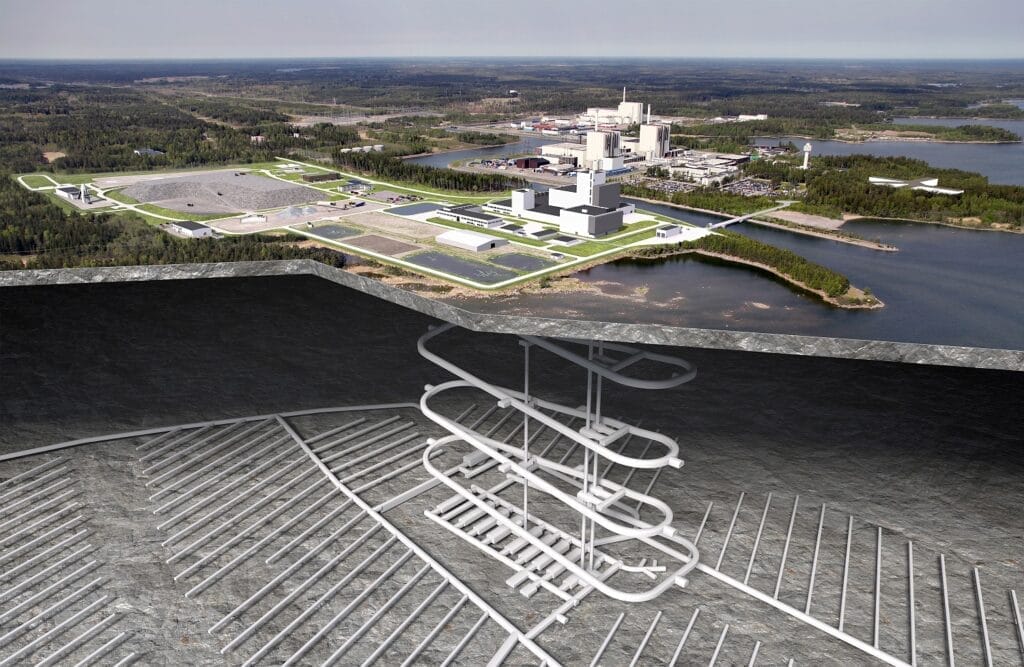

In a related development, construction has just begun on the Swedish Spent Fuel Repository which will be ready to receive initial waste in the 2030s and be fully developed in the 2080s.

The final repository will be a vast underground project that will bore 500 metres deep into a 1.9 billion year-old rock. When completed, it will store 12,000 tonnes of spent fuel in 6,000 canisters, placed along 60 kilometres of tunnels (see diagram below).

It is worth noting here that the site selection process (which was initiated via a voluntary response approach) began way back in 1992, again highlighting the very long lead times.

Australia’s policy minefield

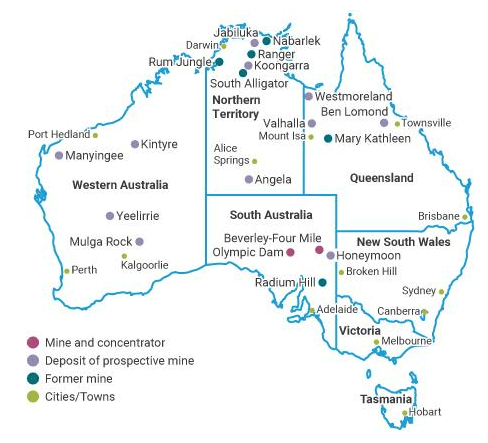

As the Minerals Council of Australia (MCA) notes “in Australia, uranium is subject to a myriad of state-based policy and legislation”.

Mining is currently allowed and is occurring in South Australia. Mining is allowed in the Northern Territory, however, due to its constitutional status, the NT must follow the advice of the Commonwealth Government before approving mine.

Last year the Commonwealth government advised the NT government that the Jabiluka Mineral Lease should not be renewed, and the site is now being incorporated into Kakadu National Park, in line with the wishes of the Mirarr Traditional Owners.

There is a policy ban on new mines in Western Australia. However, four projects previously approved for future production are allowed to proceed (although only one has significantly advanced).

Queensland and New South Wales do not allow uranium mining but a little bizarrely do allow exploration. No exploration or mining is permitted in Victoria. The map below captures the state of play.

Naturally the MCA supports “nuclear energy’s inclusion in Australia’s energy mix” and says “uranium is the essential fuel that powers nuclear energy, and Australia’s abundant reserves position it as a critical player in the global transition to clean energy”.

Naturally the MCA supports “nuclear energy’s inclusion in Australia’s energy mix” and says “uranium is the essential fuel that powers nuclear energy, and Australia’s abundant reserves position it as a critical player in the global transition to clean energy”.

MCA argues that Australia’s uranium exports, which avoid 200 million tonnes of global carbon emissions annually, “demonstrate the crucial role this resource plays in global decarbonisation” and says “expanding production could see that figure rise to 600 million tonnes, further solidifying Australia’s reputation as a trusted global supplier of clean energy solutions”.

Investors need to look abroad

The uncertainty over Australia’s attitude to uranium means most of the funds raised by ASX-listed companies actually go towards uranium exploration and development in countries such Namibia, Malawi and Canada.

According to BDO’s latest Explorers Quarterly Cash Update, uranium stocks had financing inflows of $160 million in the September 2024 quarter to advance their projects (see below).

However, nearly all of this ($150 million) was raised by just two companies for their respective projects in Namibia.

Bannerman Energy secured $85 million through a two-tranche equity placement to advance its Etango-8 project while Paladin drew down about $65 million from a debt facility for its Langer Heinrich mine.

BDO notes that “uranium’s exposure on the ASX remains relatively limited, primarily due to the ongoing stance of Federal and State Governments toward uranium mining. As uranium’s place in Australia’s energy mix remains a contentious issue, uranium explorers with operations outside of

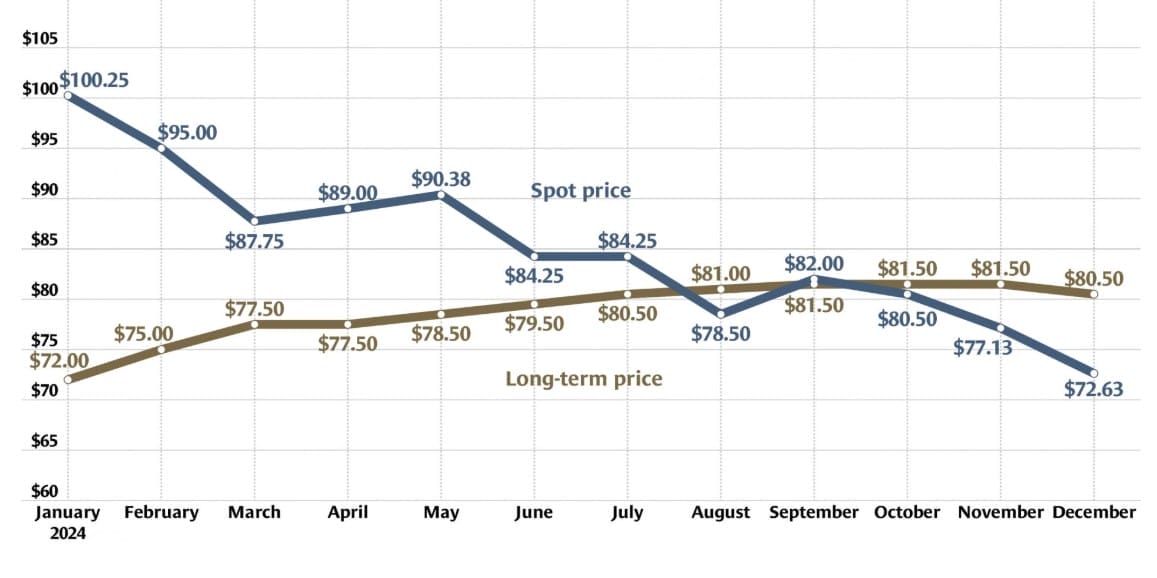

Uranium price needs to glow

It seems more countries around the world are embracing nuclear – and there has been much reporting of how the likes of Meta and Google are turning to nuclear to power the energy-hungry data centres they claim artificial intelligence (AI) requires. While this signals increased demand for uranium, the price of uranium remains subdued (see graph below).

ASX-listed Deep Yellow, whose flagship project is the Tumas uranium project in Namibia, believes “the projected uptake of nuclear power far exceeds global uranium supply expectations” and that there “are limited greenfield uranium deposits available for start-up globally over the next 10 years to satisfy projected demand”.

But despite this situation, Deep Yellow laments that “unless uranium prices increase to appropriate levels and large amounts of capital become available to the supply sector, greenfield projects will remain in limbo”.

Meanwhile, the company will also be hoping its Mulga Rock uranium project in Western Australia can find a way out of its limbo.

Leave a Comment

You must be logged in to post a comment.