When unsuccessfully railing against New York-based News Corp’s dual-class share structure late last year activist US investor Starboard Value argued that “one-share, one vote” is “a widely accepted foundational principle of corporate governance”.

Starboard claimed dual-class structures “represent worst-in-class corporate governance, as they enable certain stockholders to have voting rights that are vastly disproportionate to their economic interests”.

However, the News Corp board said it believed “there is no ‘one size fits all’ model of governance” and that its dual-class structure allowed it “to focus on long-term objectives and pursue strategies to enhance the company’s creation of sustainable value for all stockholders”.

For media companies particularly, the board argued, “dual-class capital structures provide important protections for editorial integrity, which is essential to maintaining the reputation, brand, and long-term value of these assets”.

Stealth dual-class

While dual-class shares will continue to be the subject of much debate, a recent Council of Institutional Investors (CII) paper said it was “important for investors to understand that companies can deliver substantially similar entrenchment mechanisms without creating multiple classes of common stock”.

The paper, Misalignment Under the Radar: Stealth Dual-Class Stock (James Crowe, 2024), examined a spectrum of arrangements that are categorised as ‘stealth dual class’.

These include identity-based voting power; side agreements with favoured shareholders; stock pyramiding/cross-ownership; umbrella partnerships and C corporations (Up-Cs); non-equity voting shares; and vote caps.

The paper says that “with attention on dual-class structures from investors, index providers and proxy advisors” company insiders are incentivised “to accomplish the same disproportionate influence without adopting a traditional dual-class structure”.

“By taking this approach, they may receive the private benefits of outsized decision-making power without receiving the negative attention and stock price discount accompanying dual-class stock,” it says.

The Australian Securities Exchange (ASX) remains one of the last bastions of shareholder democracy, resisting a global trend for bourses to embrace dual-class shares to make themselves more desirable listing venues.

However, with Australian asset owners increasingly investing abroad, most already have investments in big dual-class stocks like Meta Platforms, Alphabet, Apple and Berkshire Hathaway and exposure to many other companies with disproportionate voting rights.

Special rights through contract

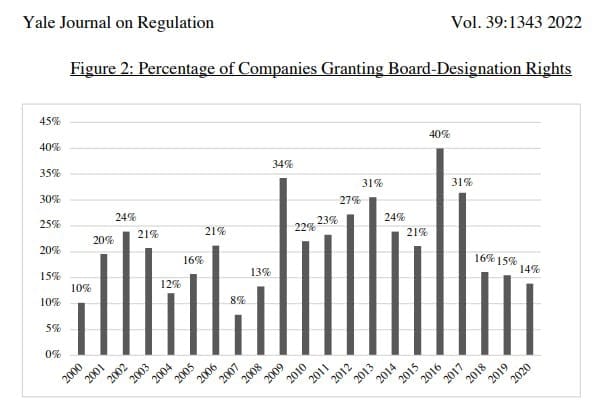

The CII paper references an earlier academic paper, The Dual-Class Spectrum (Shobe G & J, 2022), that argued the dual-class debate “has too narrowly focused on voting rights in dual-class companies and has failed to account for the myriad ways insiders obtain control rights”.

The paper – which studied the IPO documents of companies that went public from 2000 to 2020 – found companies were much more likely to grant insiders special rights through contract than through a dual-class structure, with nearly one-third of companies granting at least one special contractual right.

These included contractual rights contained in stockholder (or similarly named) agreements relating to board nomination (see diagram below); information rights; shareholder meetings; written-consent rights; and veto rights over company actions.

Bumble

Online dating app Bumble is a great example of where company insiders have gone to great – and quite innovative – lengths to ward off unwanted advances from suitors; to maintain a friendly board; and not have to build too much of a relationship with minority shareholders.

Bumble has an ‘identity-based’ voting structure within a single class of stock. Its Class A common stock carries one vote per share, unless the stock is owned by a “Principal Stockholder” – i.e. company founder Whitney Wolfe Herd and/or Bumble’s primary financial sponsor, Blackstone. When they hold common stock they are entitled to 10 votes per share.

The Delaware-incorporated Bumble also has an Up-C structure which sees Herd and Blackstone hold “common units” (that are exchangeable for Bumble A shares) in an unlisted partnership, Buzz Holdings, that provides them with taxation benefits not available to other shareholders.

As part of this arrangement Bumble also issued Class B common stock to Herd and Blackstone that through a complicated formula also entitles them to 10 votes on Bumble matters for every Buzz common unit they hold.

So when Bumble listed on Nasdaq (see picture above) in early 2021, Herd and Blackstone had combined voting power of 95 per cent while only holding about 40 per cent of Bumble stock.

Since listing, Blackstone and Herd (who set up Bumble after a high-profile break-up with Tinder, which she co-founded) have been big sellers of Bumble stock.

But even if they were no longer to have majority voting control they would still be able to significantly influence or effectively control the board and/or its decisions.

For example, if their combined voting power were to fall to 30 per cent then shareholder votes would then need a two-thirds majority to succeed, meaning Herd and Blackstone would get their way unless 95 per cent of minority shareholder votes were cast differently.

The principal stockholders’ outsized voting rights are scheduled to end on 16 February 2028, or when Herd/Blackstone own less 7.5 per cent of the Class A common stock – but who knows what other arrangements may be negotiated by then?

Fumble

So have IPO subscribers or those who bought Bumble post-IPO received anything in return for not having any voting sway at Bumble? The answer is no (unless they were IPO subscribers who exited fairly quickly).

Bumble’s IPO shares were offered at US$43 ($68.60) a share and soared above US$80 on debut. However, they are now languishing around US$8, more than 80 per cent below the issue price.

Bumble reported a US$849.3 million net loss for the September 2024 quarter. The company decided it was necessary to “perform an interim impairment test” given the “sustained decline in the company’s stock price”.

This led to US$892.2 million in non-cash impairment charges to “indefinite-lived intangible assets”, the Fruitz asset group and goodwill in Q3 2024. (Fruitz is a Gen Z dating app that uses “playful fruit metaphors” to communicate dating intentions).

Despite this, Herd and Blackstone (which bought its stake in Bumble back in 2019 from controversial Russian billionaire Andrey Andreev) still have something to smile about.

In late 2023 the Delaware Court of Chancery swiped right on Bumble’s right to assign different voting rights for the same class shares based on the identity of the owner of those shares.

In Colon v. Bumble Inc the plaintiffs argued Bumble’s stock structure violated Delaware General Corporation Law (DGCL) because it resulted in disparate voting rights among holders of the same class of stock.

However, the Court of Chancery upheld Bumble’s voting structure as valid, noting there were a number of precedent cases where companies had a provision in their certificate of incorporation allocating voting power to stockholders based on a specified formula.

Moelis

Separate Delaware litigation and legislation last year relating to New York-listed investment bank Moelis highlighted the impact stockholder agreements can have on corporate governance – and how the board-centric model of governance may be under threat.

Before the Moelis IPO back in 2014, its board signed a stockholder agreement with Ken Moelis that effectively handed the company’s founder most of the rights and powers that traditionally are held by a board.

Early last year in West Palm Beach Firefighters’ Pension Fund vs Moelis the Delaware Court of Chancery found that a number of the provisions in the agreement were invalid.

The Court of Chancery noted that under the agreement’s terms, the company had to obtain the founder’s written consent before taking eighteen different categories of action that “encompass virtually everything the board can do”.

In his decision, Vice Chancellor J. Travis Tasker asked “what happens when the seemingly irresistible force of market practice meets the traditionally immovable object of statutory law?”.

“A court must uphold the law, so the statute prevails,” Tasker said.

“The immovable statutory object is Section 141(a) of the DGCL. That provision famously states that ‘the business and affairs of every corporation organized under this chapter shall be managed by or under the direction of a board of directors, except as may be otherwise provided in this chapter or in its certificate of incorporation”.

The prescient Tasker then went on to say, “of course, the (Delaware) General Assembly could enact a provision stating what stockholder agreements can do. Unless and until it does, the statute controls”.

Market practice usurps law

A concerned Delaware State Bar Association immediately drafted a proposed amendment to the DGCL that was soon adopted by the Delaware legislature, effectively reversing the Moelis decision.

In July 2024, the Governor of Delaware signed a new bill allowing agreements that shift power away from the board to founders or large shareholders, amending Delaware law to better match current “market practice”.

This gives Delaware corporations the green light to enter into Moelis-type arrangements with stockholders without the need to amend their charters.

This is very significant given almost 60 per cent of Fortune 500 companies and almost 80 per cent of US IPOs are incorporated in Delaware. The Nasdaq-listed News Corp is also incorporated in Delaware.

Leave a Comment

You must be logged in to post a comment.