OPINION | The government should underwrite survivor-mortality bonds, or SM bonds, to help retirees worried about outliving their superannuation savings.

Australia’s compulsory super system has helped many people build up substantial lump sums prior to retirement. After retirement, most people simply roll their super into account-based retirement products.

These products are attractive because they give retirees control over their own savings; however, they provide no protection against longevity risk.

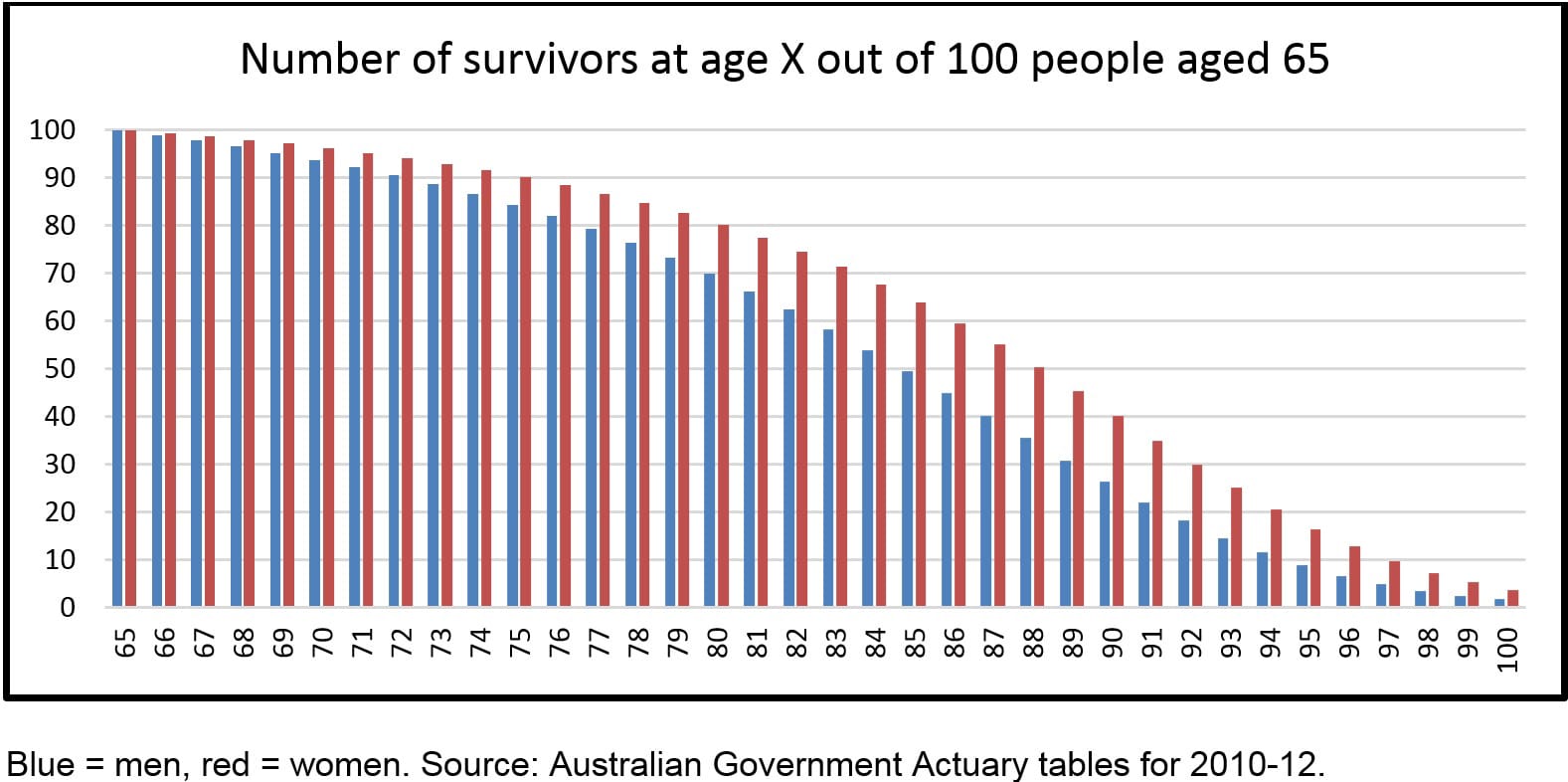

With care and luck (in the form of favourable investment returns), the account might hold enough money to last for 10, 15 or even 20 years. But many people are likely to outlive their savings. About half of all men aged 65, and two-thirds of women aged 65, will survive for more than 20 additional years.

With care and luck (in the form of favourable investment returns), the account might hold enough money to last for 10, 15 or even 20 years. But many people are likely to outlive their savings. About half of all men aged 65, and two-thirds of women aged 65, will survive for more than 20 additional years.

This is a major worry for many older Australians. Most retirees manage their longevity risk by living frugally, trying to make their savings last as long as possible.

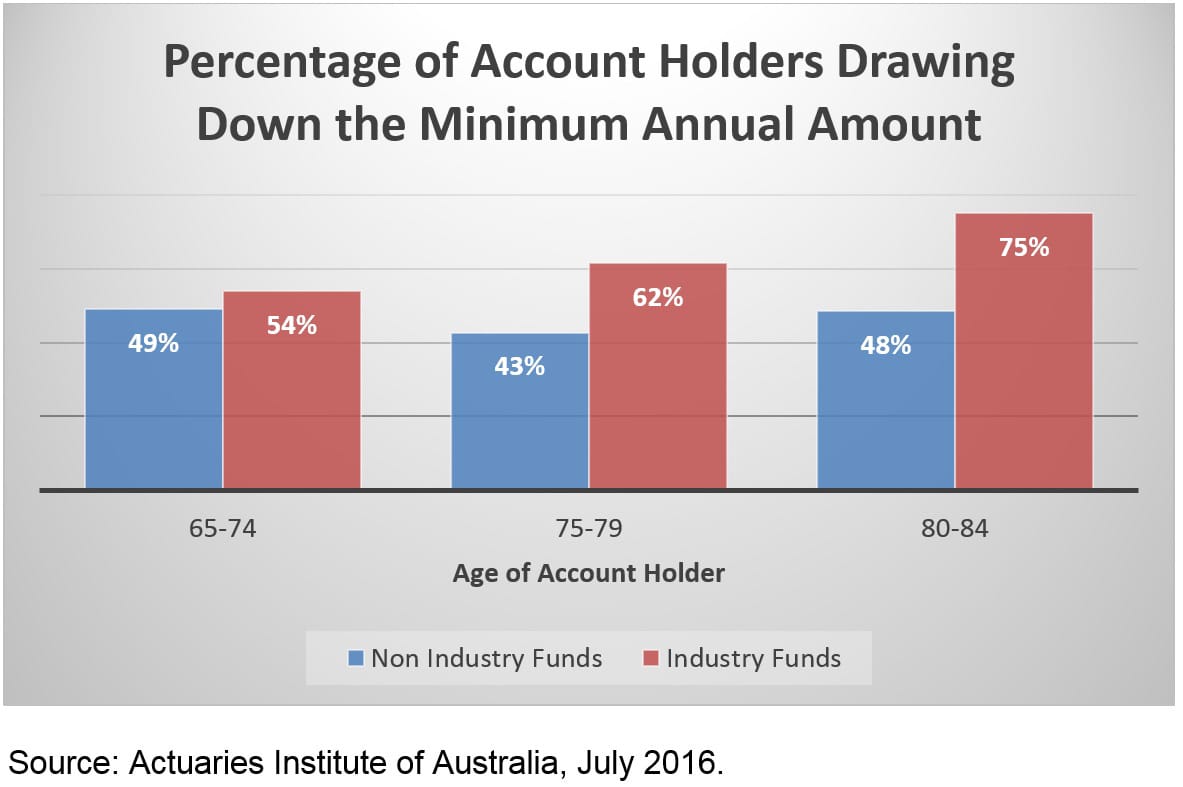

Recent studies indicate that about half of retirement account-holders withdraw the minimum permissible amount from their accounts each year. The minimum drawdown is 5 per cent for those aged 65-74, 6 per cent for those aged 75 to 79, and 7 per cent for those aged 80 to 84.

This is not a satisfactory way of managing longevity risk.

A bet on longevity

The current push for super funds to develop comprehensive income products for retirement (CIPR), as recommended by the 2014 Financial System Inquiry, is good policy. If we could make products that provided a guaranteed annual income for those who survive the longest, then retirees would have the confidence to spend more. This would empower them to enjoy both a better standard of living and greater peace of mind.

The big challenge for the industry is how to design flexible, secure, efficient products for managing longevity risks.

In May 2016, along with my colleague professor Piet de Jong from the Actuarial Studies Department at Macquarie University, I published a report that argued SM bonds play an important role as an innovative solution to this problem:

SM Bonds: A Proposal to Manage, Price and Transfer Longevity Risk

SM bonds could be underwritten as a long-term, government-guaranteed debt instrument to provide higher payments to bond-holders who survive to the redemption date. These benefits would be funded by reduced payments to the estates of those who die early.

Essentially, each investor who purchases one of these bonds is betting on their own longevity, and those who live the longest win the highest returns on their investment.

Essentially, each investor who purchases one of these bonds is betting on their own longevity, and those who live the longest win the highest returns on their investment.

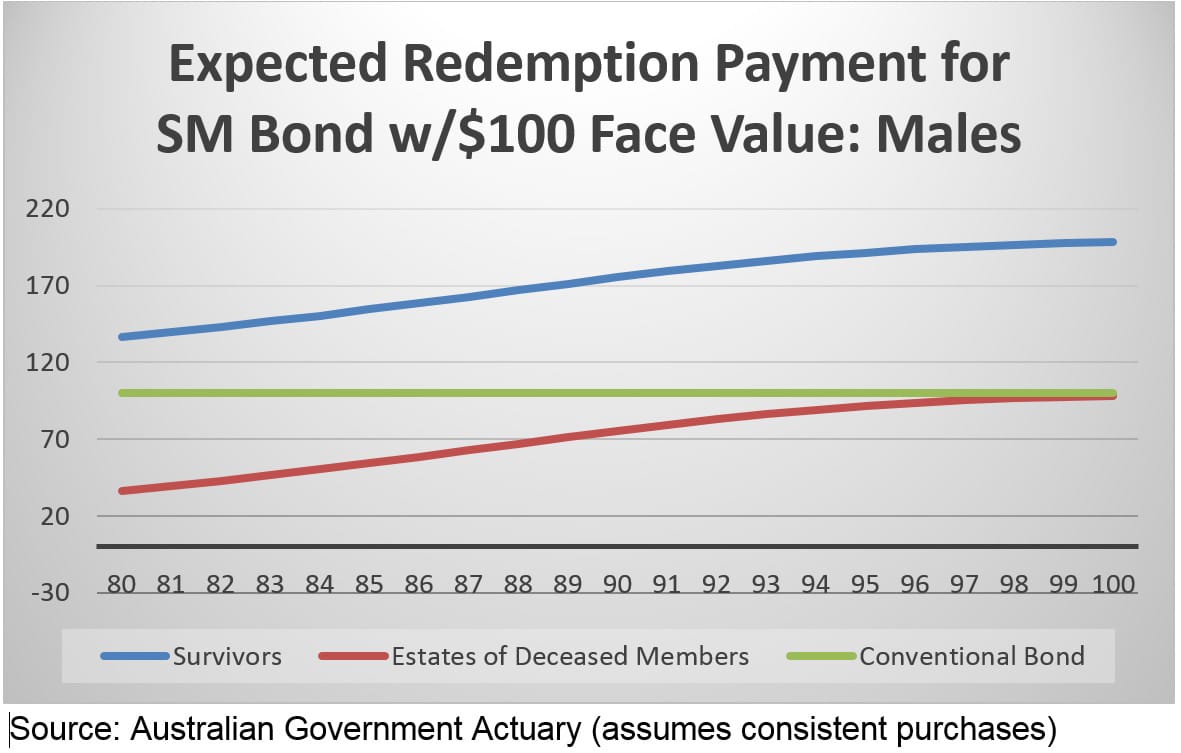

Suppose there were 100 super fund members who each bought 35-year term SM bonds each year, from age 45 to age 65. These bonds are held by the super fund, on behalf of each member, as a separate asset class.

The investors receive annual interest payments on these assets into their super savings account. At the end of the term, (in 35 years) they will receive the redemption values. These redemption payments provide an income stream from ages 80-100.

Not your average government bond

If this were a conventional government bond, the redemption payment would be the face value of the bond. But SM bonds produce a different income stream, which varies depending on the survival of each investor and the survival rates for the group overall.

The cost to the government is not affected by the number of deaths, because the longevity risks are pooled and the costs are shared among all the retirees who invest in these bonds.

As an example, suppose that a group of men aged 50 all buy 35-year SM bonds for $100. Suppose that at age 85, 50 per cent of them are still alive. Each survivor would receive $150. The heirs of the deceased investors would receive $50.

The survivorship premium increases with age. Suppose a group of men aged 60 all buy SM bonds. At age 95, suppose that only 10 per cent survive. The survivors would receive $190, while the heirs of the deceased members would receive $90.

Of course, this assumes that the investor buys the same amount of bonds each year. In practice, each investor would be able to make his or her own decisions about how many bonds to purchase annually.

Super funds would play a key role in the process and SM bonds would be just one component of a broader financial plan. This would normally necessitate some input from financial advisers.

Super funds would play a key role in the process and SM bonds would be just one component of a broader financial plan. This would normally necessitate some input from financial advisers.

There would be some restrictions on the sale of the SM bonds once purchased. They would be divided into two components, the survivor ‘S’ component and the mortality ‘M’ component.

The investor would not be allowed to sell the S component (otherwise anyone in poor health would try to sell their bond). However, the investor would be able to sell the M component at any time, creating some additional liquidity in the event of an emergency. The trading of M components would also facilitate the development of a market for longevity risk, making it easier for financial institutions to provide other useful post-retirement products.

One drawback to overcome

Widespread purchases of SM bonds would improve the financial security of retirees who survive to advanced ages, which might provide some relief for the families of retirees, since that is when healthcare costs are the highest.

One feature of SM bonds that would be unattractive to some retirees is that in the event they die young there would be less capital free for bequests. This objection has to be overcome, as the current retirement savings system is not fiscally sustainable.

As the population ages, the deficiencies of the existing post-retirement products will force more and more people to rely on the already-overburdened social security system. This may well create pressure for tighter means testing and reductions in benefits, leading to an erosion of living standards for elderly Australians.

There is a strong incentive for the government to consider seriously innovative solutions, such as this proposed SM bond system. By encouraging people to manage their own longevity risks with SM bonds, the government could reduce its own exposure to longevity risk.

The system will work only if the government takes the initiative to solve the problem – by issuing long-term SM bonds and setting up systems to administer the longevity risk pool (by keeping track of the number of deaths among SM bond owners).

Taking the longer-term perspective, it might be in the public interest to provide some incentives for the purchase of SM bonds, such as excluding the value of SM bond holdings from the Age Pension asset test.

Shauna Ferris is a senior lecturer at the Macquarie University Department of Applied Finance and Actuarial Studies.

Leave a Comment

You must be logged in to post a comment.