Around three million Australians have already dipped into their super under the early release provisions. With the value of withdrawals now expected to double from some of the earlier estimates, it is clear superannuation is become an important leg of the government’s post-COVID stimulus agenda.

While the quantum of super withdrawals may not be great for individual balances, this moment in history provides an unprecedented opportunity for super funds to engage with members.

Amid all the posturing, fear mongering and guilt tripping in the media and in campaigns run by both sides of politics around early release, the data shows that individuals are feeling more vulnerable and financially stressed than ever before, but it also turns out they have a high degree of trust with their superannuation funds.

The trust members have with their super funds has actually grown as this pandemic has played out, based on data I’ll highlight in a moment.

Given where we are in relation to the crisis and the broader superannuation industry’s maturation journey, now is the time for funds to convert the relevance and trust they have with members to help them build confidence.

Financial stress compounded by COVID-19

Australians worry about money more than anything else. That financial stress bleeds into other areas of life, negatively impacting their broader mental and physical wellbeing. It affects how much they drink, their quality of sleep and even their personal relationships.

People feel financial stress when they are struggling to meet their short-term financial obligations. Those who feel most financially stressed have the most trouble meeting their immediate expenses – like utilities bills, as well as rent or mortgage payments.

A quarter of Australians are currently worried about losing their jobs, and three quarters are fearful of the economic impact of COVID-19 on their personal finances, according to data collected by CoreData. Already one-third of people are characterising their household’s financial position as ‘not great’, ‘bad’ or ‘dire’, according to a survey of super member based on 3,520 respondents undertaken between 25 March and 28 May, 2020.

Now, more than ever, super funds are uniquely placed to help their members. The early release scheme has changed things for super. With so many Australians having accessed their super to date, something new is happening. For the first time ever, super has relevance to the lives of younger members, not just those approaching retirement.

In super we trust

Super funds are not just becoming more relevant, they’re also becoming more trusted, the data shows.

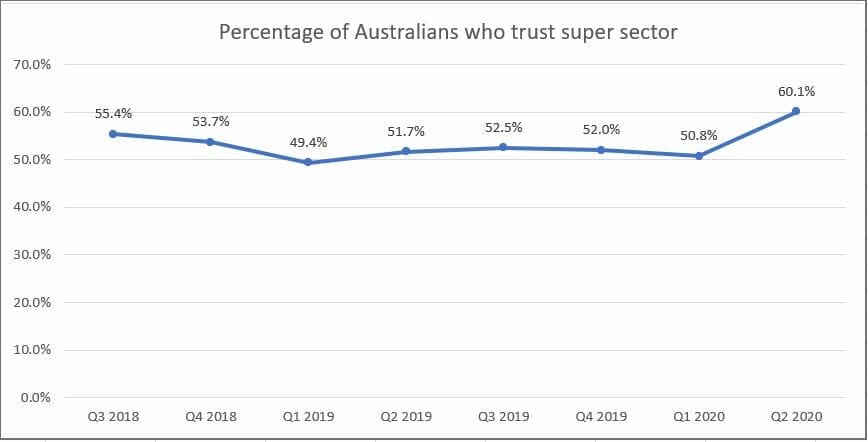

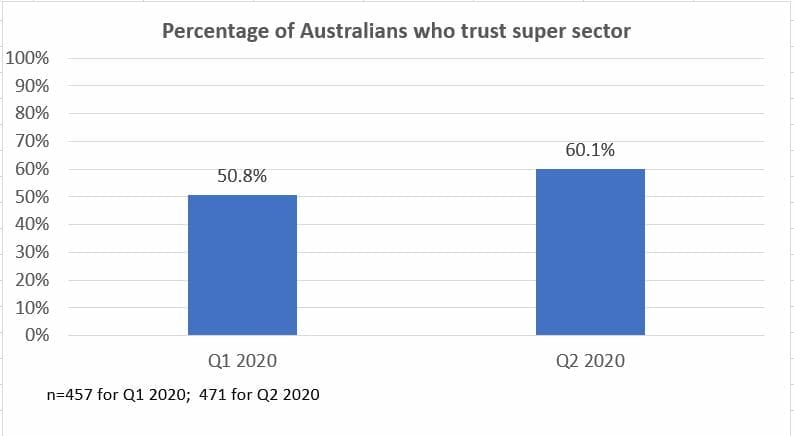

In fact, consumer trust in the super industry has rebounded during the June quarter, back to a level not experienced since the start of the Royal Commission.

In the June quarter around 60 per cent of everyday Australians had at least mild trust in the super sector. When asked to rate their level of trust in super on a scale from one to ten, this group gave it a six or more. That’s significantly higher than the March quarter, when only half the respondents had at least mild trust in super.

Trust in the government has skyrocketed in the June quarter. In June 55 per cent of general population Australians had mild trust or stronger in the government, up from 29 per cent in the March quarter.

So, what’s behind this improvement in consumer trust? Well, when we unpack the trust research, we see that around three in four Australians rate the super sector as reliable. And reliability is one of the main statistical drivers of trust.

Fortunately for the super industry, its actions have spoken louder than words. According to APRA, super funds have paid 96 per cent of early release applications within just five days.

It’s clear that super funds have been there for members when they have needed them most. And that diligence is being repaid with a trust dividend.

Now that super is relevant, and trust has returned, the real work begins. There is an unprecedented opportunity to positively engage members and help them build confidence.

Making the most of a new platform

Confidence through engagement is commonly achieved through “nudging” which demands only small, non-threatening changes in people’s behavior at any point in time. The cumulative effect of repeated nudging produces a significant end result.

Historically, super funds have been poor at this. Funds sometimes write to their members and advise them that in order to have a comfortable retirement they will require an amount, say $60,000 or more a year to live on, and to fund that, they will require a balance at retirement of more than a million dollars.

They provide a projection, advise on the gap, and then expect their members to act. But the only problem is their members usually don’t.

That’s because they experience cognitive dissonance; a term that refers to the discomfort someone feels when their behaviour is disconnected from their values. Sure, members want a comfortable retirement, but they don’t have anywhere near the amount of money the super fund says they will need. It all feels too hard and uncomfortable, so they disengage from the decisions.

Super funds would be better off harnessing social influence and communicating to their members what other people, people just like them, are doing. And by helping members to understand that it takes only small changes to behaviour to enhance financial outcomes.

The advantages of nudging are cumulative. As members grow in confidence, they will feel better about themselves and their circumstances. They will be encouraged to engage with their decisions and as a result they will feel more prepared. A virtuous circle is then created, with each action building confidence and improving retirement preparedness.

EDITOR’S NOTE: This is the first in a series of columns Andriessen will contribute exclusively for Investment Magazine on the topic of member engagement. Future contributions will explore barriers to engagement, behavioural biases, the role of super in advice and models for enhancing and funding engagement programs.

Leave a Comment

You must be logged in to post a comment.