Recent greenwashing inquiries, progress reports, consultation papers and studies in Australia, Europe, Asia and North America provide insights into the key drivers of greenwashing showing significant challenges facing asset owners and managers.

They are also food for thought for the Australian Sustainable Finance Institute (ASFI), as it develops Australia’s sustainable finance taxonomy, drawing upon work undertaken internationally on taxonomies, and for the Government when it consults further on its Sustainable Finance Strategy.

The European Union (EU) Sustainable Finance Framework is often cited as a best-practice guide for other regions and countries drafting sustainable finance roadmaps but there are questions about its efficacy and its ability to adequately address greenwashing.

Losing faith in the Articles

Most of these relate to the EU’s Sustainable Finance Disclosure Regulation (SFDR) that requires financial products making sustainability claims to disclose information to back up those claims to help combat greenwashing. The SFD’s Article 8 covers products promoting “environmental and/or social characteristics”; and Article 9 covers products having “sustainable investment” as an “objective”.

Last week the European Commission released consultation papers seeking views on the “potential shortcomings” of the SFDR, including in its interaction with the parts of the EU Framework such as the EU Taxonomy. The Commission is concerned that the SFDR – which was only intended as a disclosure regulation – is being misused by the financial services sector as product labelling regime and marketing tool. Article 9 products are being promoted as “dark green”; Article 8 products as “light green”’ and Article 6 products – those that do not have sustainability features – as “brown”.

The Commission says “The fact Articles 8 and 9 are being used as de facto product labels – together with the proliferation of national ESG/sustainability labels – suggests there is a market demand for such tools in order to communicate the ESG/sustainability performance of financial products”. However, the Commissions says “there are persistent concerns that the current market use of the SFDR as a labelling scheme might lead to risks of greenwashing”.

Both the SFDR and the EU Taxonomy introduce definitions of “sustainable investment” (SFDR) and “environmentally sustainable” economic activities (Taxonomy). While these definitions are similar they presented uncertainties. Fund managers had been “downgrading” their products from Article 9 to Article 8 to avoid greenwashing risk or accusations. To stem the Article 9 outflows, the Commission was obliged to issue a lengthy FAQ, clarifying that investments in Taxonomy-aligned “environmentally sustainable” activities automatically qualified as SFDR “sustainable investments”.

“Potential big changes have been flagged in the EU. The Commission says it is considering a more precise product categorisation system building on the distinction between Articles 8 and 9. It also says might look at a “different approach” to categorisation. This could be a more thematic investment strategy approach that might see the Article 8 and 9 concepts and distinctions “disappear altogether”.

Warning of even broader changes for the sake of transparency, the Commission also raises the possibility that all financial products – even those not claiming to fall under a sustainability product category – may be required to make sustainability disclosures.

Greenbleaching

One of the issues that may be forcing change is what the Securities and Markets Stakeholder Group (SMSG) of the European Securities and Markets Authority (ESMA) has described as “greenbleaching” (or what we might call greenhushing).

Responding to ESMA’s Call for Evidence (CfE) on potential greenwashing practices in the EU’s financial sector, the SMSG said greenbleaching – where fund managers invest in sustainable activities but refrain from claiming they do, to avoid greenwashing accusations – should be closely monitored.

“Greenbleaching can lead to a situation where a product is actually ‘greener’/‘more ESG’ than the product provider claims,” the SMSG said. But even if this might be considered misleading the SMSG’s view was that as long as there is no legal obligation to disclose how sustainable a product is, not claiming sustainability cannot be considered a “misrepresentation”.

However, The SMSG also warned that if greenbleaching is a widespread phenomenon – “the result may be an overly restrained market for sustainable products” and “less transparency and clarity” for investors regarding the ESG intensity or ESG strategy of different funds.

What fuels greenwashing?

The fundamental mismatch between demand for investments that can make a climate/sustainability impact and the supply of genuine sustainable investment opportunities is at the heart of the greenwashing issue.

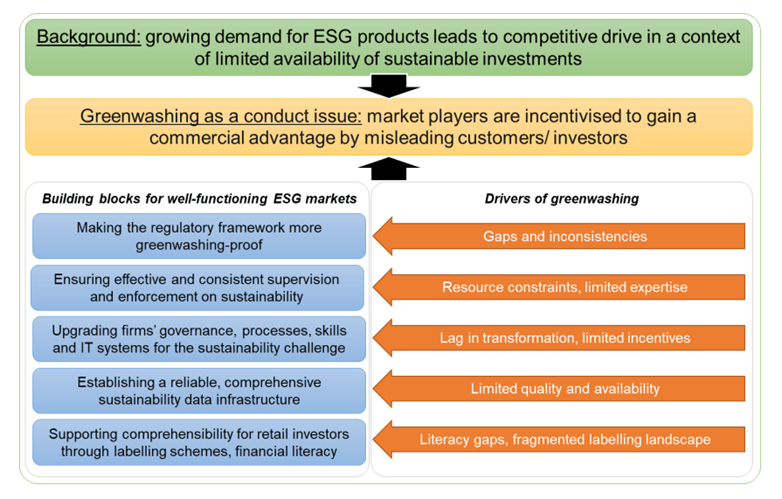

ESMA’s recent ‘Progress Report on Greenwashing’ notes “the competitive drive for market shares and revenue has led to both entity-level and product-level efforts at bolstering sustainability profiles”. The temptation to greenwash is therefore very high “in a context of very low levels of taxonomy-aligned assets, investment opportunities for which sustainability performance appears to be beyond doubt or disagreement are still scarce”, ESMA says.

ESMA said the risk is exacerbated by inadequacies in the regulatory framework such as unclear, ambiguous definitions of certain concepts; lack of standardised calculation of metrics; minimum standards failing to support the ambition level, such as for climate benchmarks; and the absence of regulation for certain widely-used concepts such as “impact investment”.

Drivers of Greenwashing

Source: European Securities and Markets Authority (ESMA)

For the investment management sector, ESMA says identified high-risk greenwashing areas include impact claims, statements about engagement with investee companies; and material relating to a fund or asset manager’s ESG strategy and ESG credentials (such as ESG labels, ratings or certifications).

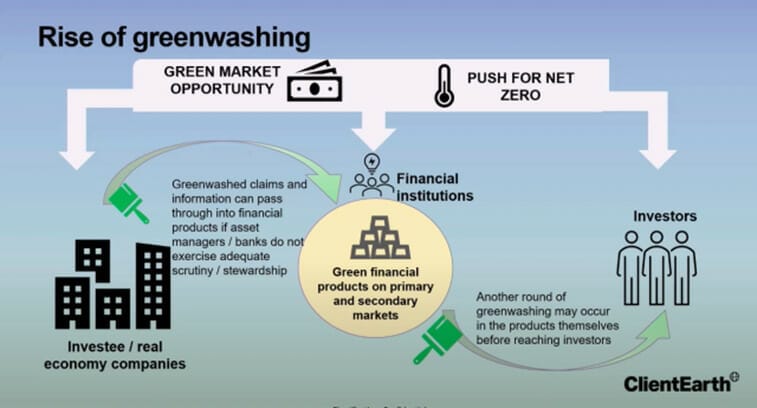

The Asia Investor Group on Climate Change’s (AIGCC) recent ‘Greenwashing and how to avoid it’ report notes that in the investment chain, there can be two rounds of greenwashing. There is the greenwashing flowing from the claims by – and (mis)information from – investee companies that can pass through into financial products if asset owners/managers do not exercise adequate scrutiny/stewardship. And then there can be the greenwashing of the financial products themselves through the way they are promoted by financial institutions.

Source: AIGCC and Client Earth

State-sponsored greenwashing?

Last year the European Commission agreed conditions under which gas activities can be included as transitional activities under the EU Taxonomy. This created much outcry from asset owner groups such as the Institutional Investors Group for Climate Change (IIGCC) who said it undermined the Taxonomy’s credibility. Earlier this year four NGOs filed a case in the EU Court of Justice seeking a reversal of this decision, arguing “labelling fossil gas as ‘sustainable’ is as absurd as it is unlawful”.

In June the ‘ASEAN Taxonomy for Sustainable Finance, Version 2′ report included provisions that included coal-fired power plants in the process of early retirement as eligible for green financing. The ASEAN Taxonomy Board said it hopes the “coal phase-outs (CPO) criteria, a unique feature and a global first for a regional taxonomy, encourages early action to reduce the region’s reliance on coal as a major energy source”. While the Board’s position is arguably defendable it seems to have inspired Indonesia to push the envelope further.

It was reported earlier this month the Indonesian Financial Services Authority (OJK) was thinking about revising Indonesia’s green taxonomy to grant a green label to coal-fired power plants if they are seen as helping the energy transition or being part of a larger green value chain. For example, a coal-fired power station might be labelled green if it supplied electricity to an electric vehicle (EV) car manufacturer or an EV battery maker. Some may say this sounds dangerously close to state-sponsored greenwashing. At home, meanwhile, the Australian Government’s Climate Active carbon-neutral certification scheme has also been accused of greenwashing.

More regulation

Asset owners and managers around the world have typically been calling for more guidance rather than more regulation or legislation to deal with greenwashing. However, they may not get what they want.

The UN High‑Level Expert Group’s ‘Integrity Matters: Net Zero Commitments by Businesses, Financial Institutions, Cities and Regions’ report said if greenwash premised upon low-quality net zero pledges is not addressed it may result in “a failure to deliver urgent climate action”. The Expert Group said “to effectively tackle greenwashing and ensure a level playing field, non-state actors need to move from voluntary initiatives to regulated requirements for net zero”.

Given the high stakes the Expert Group believes “ultimately, regulations will be required to establish a level playing field and ensure that ambition is always matched by action”.

Meanwhile – despite all the taxonomies, report and papers – everyone is still waiting for a consensus definition of greenwashing that can be used no matter the market you are operating in. The Association for Financial Markets in Europe (AFME) stated the obvious when it said “it is important to avoid coming up with a definition that, despite being all encompassing, does not help – either authorities or market participants – develop targeted measures to fight greenwashing”.

Leave a Comment

You must be logged in to post a comment.