Australia’s retirement income system has again been graded a B+ by the Mercer and CFA Institute’s Global Pension Index in 2023 – a status it has struggled to shake since the ranking’s establishment in 2009.

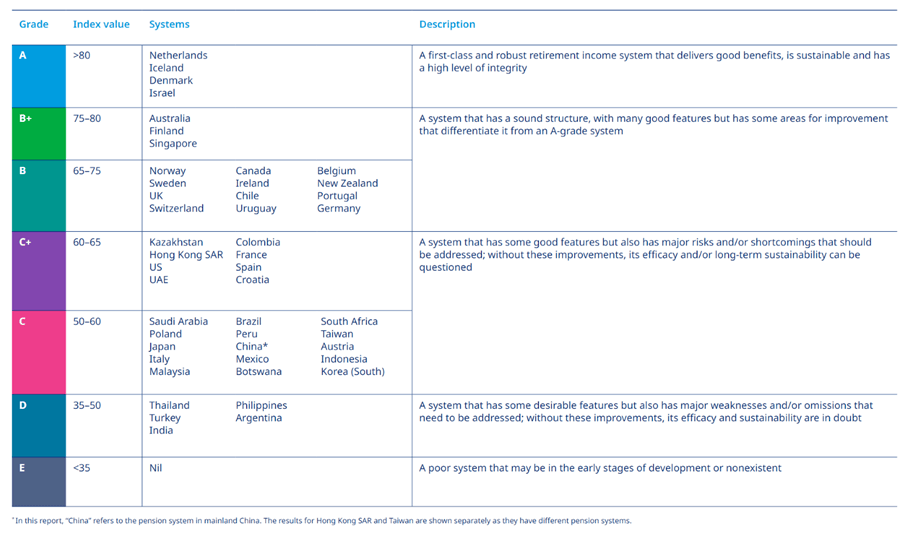

Netherlands, Iceland, Denmark and Israel were all deemed to have superior pension systems, despite the advent of legislation such as the retirement income covenant and a heightened focus on retirement policy from regulators and think-tanks such as the Conexus Institute.

Speaking to Investment Magazine, David Knox, senior partner at Mercer and lead author of the report, said the Australian superannuation system has been great at accumulation.

However, while it retained its B+ rating, Australia’s overall index score increased this year off the back of the rising superannuation guarantee and the sector’s growing contribution to the economy.

Nonetheless, he reiterated his longstanding position that Australia’s system was not sufficiently geared towards decumulation.

“The top four countries that are A-grade – Netherlands, Iceland, Denmark and Israel – all of them require that most of your benefit be taken as a pension or income,” Knox said.

“We don’t have that requirement. Whenever you’re retired, we say: ‘Here’s your money. You can take it as an income if you want, or you can go and spend it on the horses.’”

The Global Pension Index compares 47 retirement income systems around the globe with three new countries introduced this year –– Botswana, Croatia, and Kazakhstan. It covers around 64 per cent of the world’s population.

It examines “adequacy”, defined as the system’s design features and how well it caters to people with different levels of income and wealth, and “sustainability”, defined as whether it can continue to perform over the long term, and “integrity”, which is how well governed the system is.

‘It’s that simple’

The results come on the heels of a scathing report from regulators ASIC and APRA, which said there is “a lack of progress and insufficient urgency” as super funds scramble to meet their new obligations under the retirement income covenant. Knox said it’s because the covenant’s implementation is still in the early stages.

“I think some trustees are treating this very seriously. But it also has to be recognised that developing a new product cannot be done within a six- or 12-month period.”

He said while these legislative developments in the retirement income space are the right steps, they are not the final steps, as he called for a “compulsory income stream for all retirees with a reasonable super balance”.

The industry can argue what that exact “reasonable” figure is, but Knox suggested it should be $200,000 or above.

“That [compulsory income stream] should be introduced very gradually, so we’re not suddenly affecting people who are going to retire next year. Because these people have made plans under the current rules.

“It also wouldn’t mean that everybody could do what they like with the first $200,000. If that’s all they had, they’re probably getting the full-age pension… But I would argue that most of the money above that level should be in an income stream.

“For most people, that means a regular income. You may call it a pension, an annuity, or spending money. In other words, we need a system that delivers income.

“The purpose of superannuation is to provide people with money in retirement. It’s that simple.”

Leave a Comment

You must be logged in to post a comment.