Around the world, there is growing divergence and misalignment between asset owners’ expectations and asset managers’ actions when it comes to voting and investee engagement on ESG issues.

Asset managers are backsliding on supporting climate and other ESG-related issues and some are accused of masking this through greenwashing.

NGO ShareAction’s recently released ‘Voting Matters 2023: Are asset managers using their proxy votes for action on environment’ report found some asset managers are hiding behind their net-zero commitments while failing to take action.

“Many asset managers have set net zero targets, however failed to translate this rhetoric into action when it came to voting,” the report said.

Late last year the UK Asset Owner Roundtable – concerned that the short-term interests of asset managers were trumping the long-term interests of pension funds – commissioned a report to try and get to the bottom of the problem.

The report came up with a list of reasons why asset manager stewardship and proxy voting at major oil and gas companies in the UK, Europe and the US was not aligned with asset owners’ needs. However, it was short on solutions.

Last month, another group of UK asset owners led by the London CIV Local Government Pension Scheme signed an open letter to asset managers lamenting the divergence and disconnect between the voting behaviour of appointed managers and “our investment principles and the expectations of our beneficiaries” on ESG issues.

To solve the problem, their letter urgently called for more of their asset managers to offer ‘pass-through voting’ on pooled funds so that the asset owners could take back control and cast their own votes when they desired.

Earlier this month, the Institutional Investors Group on Climate Change (IIGCC) released its Net Zero Voting Guidance to help asset owners and managers get on the same page, noting “alignment between asset owner and manager on climate stewardship and how this is integrated into investment decision making is critical to achieving net zero targets”.

Conceptual issues

The ‘UK Asset Owner Stewardship Review 2023: Understanding the Degree & Distribution of Asset Manager Voting Alignment’ research paper commissioned by the roundtable (whose members include Church of England Pensions Board, Scottish Widows and Brunel Pension Partnership) came up with five reasons for the misalignment:

- Cultural/political misalignment – the participating asset owners were all UK based while most participating asset managers were not;

- Fundamental misunderstanding as to the relevance of stewardship and voting itself or the urgency of climate change as a key priority theme within stewardship;

- Conceptual misunderstanding of fiduciary duty itself;

- Conceptual disagreement as to the most effective combination of stewardship processes. From the voting rationale review, some asset managers appear to see voting and engagement as mutually exclusive while others viewed it as much more complementary; and

- Asset managers and/or the financial firms owning them tend to have many more commercial relationships with the issuers/investees than the asset owners whom the asset managers serve.

Voting rationales

The roundtable review conducted a series of studies using anonymised voting data that asset managers such as Blackrock, JP Morgan, Lazard and Legal & General Investment agreed to provide.

The review noted some managers had developed procedural standard responses – such as “the request is either not clearly defined, too prescriptive, not in the purview of shareholders, or unduly constraining on the company” – to explain why they would be voting against an ESG-related proposal.

Given that this standard response “links four different potential voting rationales in an either/or structure, it essentially provides a voting rationale response which circumvents the request to provide one specific rationale. It might be worth reflecting if voting rationales could be phrased in a less opaque manner,” the report said.

The report also said some proxy advisory firms “provide institutional investors with carefully worded, carefully balanced voting rationales, which weight the merits of both sides of the argument but eventually favour corporate management over asset owners. In this sense, asset manager misalignment may – to some extent – be outsourced”.

Many asset managers appear “to conceive voting and engagement as conflicting or mutually exclusive activities” as they, for instance, perceive ‘greater value in engaging with the company’ rather than voting for a climate resolution endorsed by 100 per cent of the participating asset owners.

Greenwash

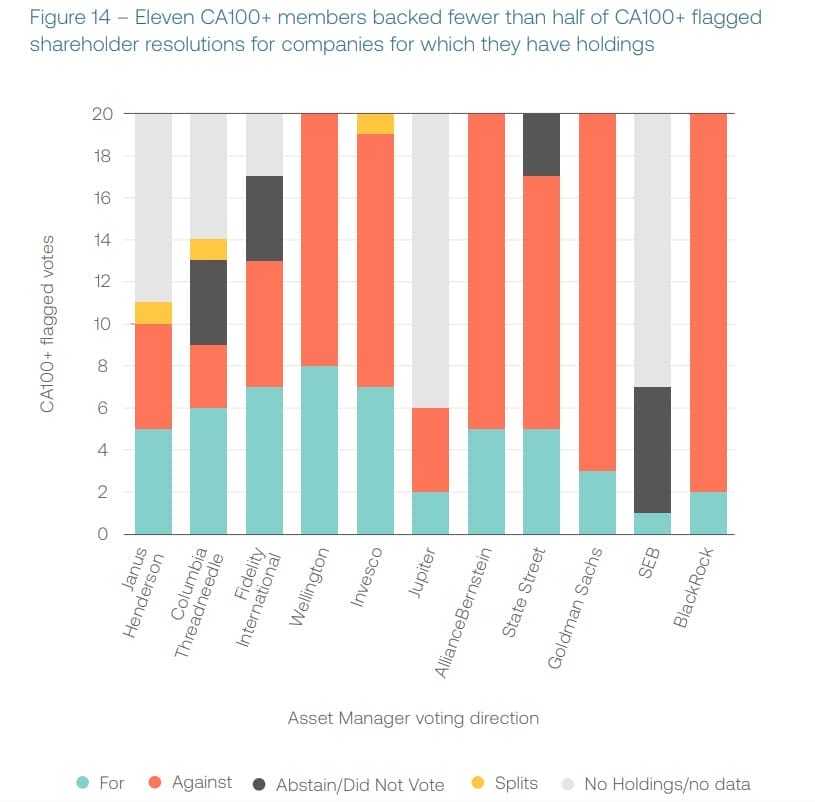

ShareAction’s Voting Matters report reveals a number of Climate Action 100+ members had voted ‘against’ all CA100+ flagged resolutions in 2023 that required companies to set stronger climate targets. Eleven CA100+ members in its sample voted for fewer than half of the flagged resolutions for which they had holdings (see Figure 14).

This raises questions around some CA100+ members’ commitment to meaningfully reduce emissions at investee companies. If CA100+ doesn’t require stronger minimum standards for signatories, the initiative “risks enabling laggard managers to greenwash their operations while continuing to vote against urgent climate action”.

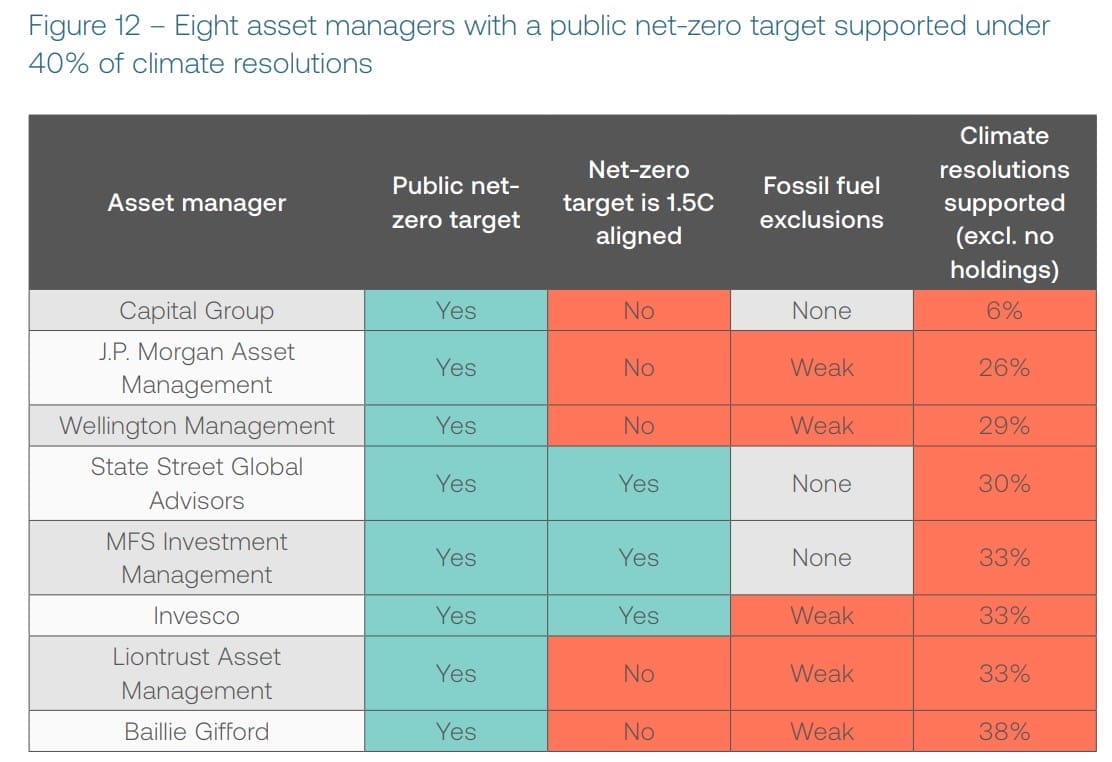

Many asset managers with public net-zero targets are also failing to back these up with support for climate resolutions (see Figure 12).

The varying levels of support show asset managers “are relatively more supportive of disclosure-based resolutions and are resistant to more action-oriented resolutions which would be required to actually address real world problems,” ShareAction says.

ShareAction also separately reviewed the stewardship and sustainability reports of the 50 largest global asset managers, and found disclosure on escalation was “limited and vague”.

Its ‘Responsible Investment Standards & Expectations (RISE) – Guidance Paper #2’ said that “although the majority of asset managers reference escalation, on the whole they provide insufficient detail about the application and outcomes of escalation activities, including the pace of escalation” (see Figure 1).

The IIGCC guidance says voting should be incorporated into a fixed part of the selection, appointment and monitoring of external asset managers, encompassing both the managers’ voting policy and voting behaviour during the year.

It also recommends asset owners set up annual calls with their managers to discuss voting behaviour and conduct a “deep dive on how the managers’ commitments (e.g. Climate Action 100+) align with their voting actions”.

IIGCC suggests that a voting policy such as the one adopted by the UK’s biggest pension scheme Nest could be “a powerful tool that can be used to conduct a gap analysis between the asset owners’ potential voting decisions and those made by the manager during the year”.

Whilst Nest’s fund managers usually vote on its behalf, Nest has its own voting and engagement policy outlining its views and its expectations of companies. Nest is able to override its fund managers’ votes when their voting decisions do not align.

Nest determines what are its significant holdings – called the “voting subset” – and asks its fund managers to pre-disclose voting intentions for these holdings. Nest uses Minerva Analytics to help monitor the voting intentions of its fund managers for voting subset companies.

Before deciding to override votes, Nest engages with its fund managers on the voting decisions they make to understand their rationale for voting differently and what research and engagement they’ve undertaken to inform their voting decisions.

Client-directed/pass-through voting

The UK open letter noted technology such as fintech company Tumelo’s pass-through voting solution now enabled asset owners to choose a voting policy or vote on specific issues without disrupting their asset managers’ existing stewardship process.

These solutions – which in the UK are now being offered by asset managers such as Legal & General – mean asset owners can align voting across their entire portfolio; for their direct shareholdings, segregated mandates, and pooled funds.

The IIGCC said “If used correctly, client-directed voting can be a “cost-effective tool for asset owners who are seeking to align voting with their climate commitments”. It can also highlight disagreements and misalignment between asset owners and managers, “providing an evidence-based engagement tool for asset owners to highlight discrepancies to managers through the selection, appointment and monitoring process”.

However, the IIGC also warned “client-directed voting not supported by aligned engagement activities could risk splitting the vote between asset managers and asset owners, diluting the voting decisions and divorcing voting from engagement, rather than reinforcing objectives set during the engagement process”.

ShareAction is also concerned that pass-through voting “facilitates a fall in ambition from asset managers, rather than primarily empowering clients to exercise their voting rights”.

Leave a Comment

You must be logged in to post a comment.