The retirement industry is currently operating in a kind of purgatory where business, policy and regulatory challenges are holding back the provision of good retirement outcomes for all retirees. We are concerned that many retirees will be left behind unless the right settings are put in place, ideally sooner rather than later.

It is time to think big – something that the Treasury’s ‘Superannuation in retirement’ consultation encouraged. Our submission took up the challenge by penning 13 essays on a range of topics that informed a variety of policy recommendations. Our central theme is that current settings are working for neither super funds nor retirees. Some bold measures are required to create an effective retirement super industry that works for all retirees.

Three overlapping pieces of work are central to our key policy suggestions:

- Market mechanisms cannot be relied on to deliver good outcomes for retirees.

- Business incentives to deliver high-quality retirement income strategies (RIS) are lacking for some super funds, creating tension with the obligations under the Retirement Income Covenant (RIC).

- We build on our work on choice architecture (see “Pathways for directing members into retirement solutions”) in expressing high concern that certain retirees will be left behind without the ability to ask their fund to provide them with a clear recommendation.

These themes together suggest that improvement is necessary in three areas for the super system to work well for all retirees. First, super funds need to step up and do more for their retired members. Second, the super sector needs clarity and appropriate incentives to commit strongly to retirement. Third, funds need to be enabled to assist their retiring and retired members in an effective manner.

We now explore these areas in further detail.

Retirement market is prone to failure

In 2018 the Productivity Commission stated that “there is no prospect that Australia’s basic financial markets will be fully competitive”. When it comes to retirement, we believe the market is more prone to failure for two reasons. First, effective competition seems unlikely between providers (i.e. super funds). Competition is inhibited by the combination of difficulty in comparing products, services and solutions and strong incumbency effects. Most members tend not to look beyond their current fund as they find it very difficult to choose and switching costs are high.

Second is limits to effective choice. Many retirees have low capacity – and willingness – to make financial decisions for themselves. This reflects a range of influences, most notably the intersection between cognitive limits and complexity – both of retirement itself and the solutions and products on offer.

Business incentives are weak for some super funds

The RIC places an obligation on the trustees of all super funds to develop an RIS. However, the business case for investing considerable resources and effort into retirement is not clear for every fund. There is a stark variation amongst funds relating to the percentage of assets (1 per cent to 69 per cent) in the retirement phase.

Thus many funds are facing into their RIC obligation to develop an RIS for a small portion of their existing member base. These funds are confronted with a tenuous financial case (high cost, long-dated benefits, little competitive upside) and issues including how retirement fits into the overall business strategy, cross-subsidisation, first-mover risk, and legacy product threats.

The incentive for some funds will be to drag their feet or deliver the minimum required rather than make a big commitment of management time and resources to developing a high-quality RIS. Further, undershooting is somewhat accommodated by a principles-based framework. The members of these funds are at risk of poorer outcomes.

Choice architecture fails those retirees who would benefit from a recommendation

There are two existing pathways through which a retiree finds a retirement solution: financial advice and self-direction.

Retirees advised by a financial adviser will receive a personalised retirement strategy, but the financial advice sector is supply-constrained and too costly for some. Self-guided retirees will benefit from improvements in the information and digital tools provided by funds. But these are not enough.

In particular, a class of members exists that has limited capacity or desire to make financial decisions on any level – be it for reasons of very low financial literacy, poor language skills, cognitive decline or even ‘fear of finance’. Relying solely on engagement in a choice framework will leave these members behind if they are required to make choices that they can’t even understand.

There is a substantial group of retirees who would benefit from being able to ask for their fund to choose a retirement solution for them, thus relieving them of the need to engage with decisions for which they are poorly prepared.

Solutions when the market is prone to failure

Three broad alternatives in situations where the market is prone to fail include:

- Taking action to address the source of market failure;

- Government intervention, either through regulation or direct involvement in the market;

- Ensuring consumers have access to well-informed and aligned agents that can assist them, or even make decisions on their behalf.

We see a role for pursuing all three alternatives. However, the role that might be played by super fund trustees as a trusted agent is being largely overlooked in the current policy discussions.

Both the Super in Retirement consultation and Delivering Better Financial Outcome reforms seem more focused on assisting members to make better choices for themselves, i.e. addressing market failure. Do we really want to continue to rely on a choice market structure where not all retirees are capable or want to make retirement decisions?

Super fund trustees as an informed and aligned agent

Three elements are required for super fund trustees to operate as effective agents in assisting their retired members.

First is ensuring that trustees will act in the interests of retired members. Our concern is that funds which lack a strong business case to develop a quality RIS may struggle to prioritise retirees.

Second, super funds need to deliver RIS of at least an adequate quality. The issue here is the principles-based RIC that places no formal obligations around delivery standards.

Third, super funds need to understand individual members to identify the retirement solution that best suits their needs. Here the personal financial advice rules and related difficulties of collecting and using personal information loom large as a barrier to assisting members on an individual level.

Recommendations to create a stronger retirement system

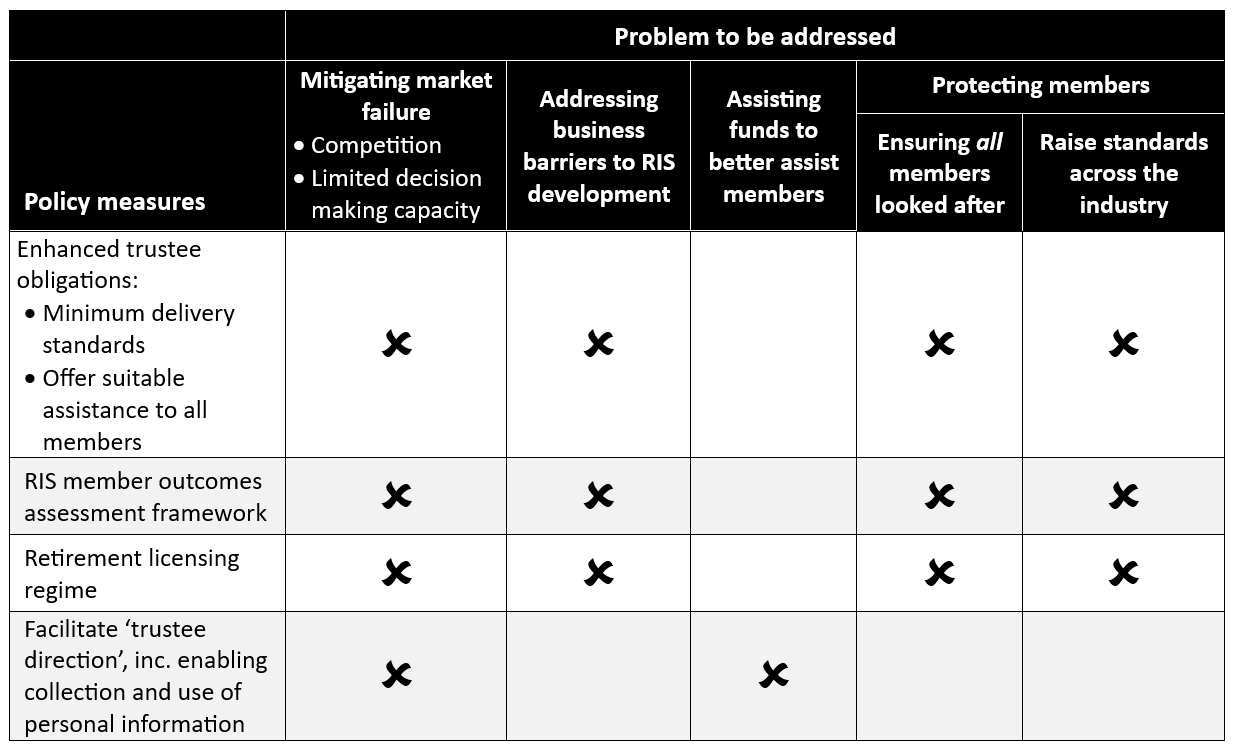

The table below summarises the problems outlined above and the policy measures we propose along the theme of ensuring that super funds are effective agents that act to benefit their retired members while leaving no members behind. The broad thrust is to (a) place clear obligations on trustees who operate a RIS in terms of service delivery, (b) provide an opt-out for those funds who cannot justify the business case, and (c) empower funds to assist all members into appropriate retirement solutions.

A brief description of each proposed policy measure along with how they assist:

A brief description of each proposed policy measure along with how they assist:

- Enhanced trustee obligations around meeting minimum delivery standards and “attempt-to-engage” every candidate retiree.

- A dedicated RIS member outcomes assessment framework (i.e. separated out from the existing member outcomes assessment framework) to enable deeper assessment and establish expectations around what trustees are required to address in their RIS.

- A retirement licensing regime would detail licensing criteria, and necessitate funds to either decide not to participate in the retirement market (i.e. focus on accumulation) or to develop a quality RIS that meets the licensing criteria on a specific timeline (e.g. a few years).

- Measures to facilitate trustee direction, including designing a framework that allows funds to collect member information and use it to provide a personalised retirement strategy recommendation, without the costly requirements associated with provision of personal financial advice.

Collectively the above measures would amount to a substantial change in retirement policy settings. But consider the current state of retirement: a foundational reliance on fractured market mechanisms, business case challenges for many funds, and cohorts of retirees who find it hard to make financial decisions about their retirement.

Stronger policy measures than currently being contemplated are needed to both assist the super industry and, most importantly, to help retirees. Undoubtedly each recommendation requires further consideration, research and healthy debate. The risk is that in “thinking small” we leave the retirement industry in its current state of purgatory. And leave many retirees behind in the process.

David Bell is executive director and Geoff Warren is research fellow at The Conexus Institute, a not-for-profit think-tank philanthropically funded by Conexus Financial, the publisher of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.