Brazil’s JBS S.A. is the world’s second-largest food group and largest meat processor with more than 400 production facilities across 20 countries.

When bidding against Andrew Forrest in its ultimately successful offer for Tasmanian salmon farmer Huon Aquaculture in 2021, JBS, however, stressed “we don’t operate our facilities and businesses like a multinational company”, instead valuing “local employment and local economies”.

In February this year, when its Dinmore beef abattoir in Ipswich – the biggest in the southern hemisphere – employed another 300 people JBS celebrated the fact the regional Queensland facility now employs workers representing 47 nationalities.

JBS’ Primo brand has just extended its partnership with the universally-loved Collingwood Football Club, supporting its AFL and AFLW programs and Primo has also re-signed as a key partner of the Brisbane Heat, with its logo to appear on the caps and helmets of both Heat Twenty20 cricket teams.

So why is JBS treated by so many around the world as an ESG pariah? It is hard to know where to begin.

A good place is probably the Brazilian billionaire brothers Joesley and Wesley Batista who control JBS S.A. and who JBS announced last week had been nominated to return as board members after years in the wilderness following their involvement in bribery and corruption scandals.

Then there is the litany of matters such as JBS’ highly questionable net zero emission claims, links to deforestation in Brazil, labour rights violations and governance issues relating to its proposed dual-listing on the New York Stock Exchange (NYSE).

JBS’s renewed NYSE ambitions have created a backlash that has led to the State of New York, a group of US senators and scores of NGOs and advocacy groups around the world taking action against the group and/or protesting its listing plans.

JBS SA is currently listed on Brazil’s Novo Mercado. A restructuring is proposed that would see JBS S.A. become a subsidiary of new Dutch holding company JBS N.V. that would be listed on the NYSE and the Novo Mercado.

A NYSE listing would put JBS N.V. on the stock radars of Australia’s biggest asset owners who are increasingly investing in overseas equities listed on major international markets.

ESG-conscious super funds may, however, have to do some thinking about the filters they should apply to their radars.

JBS S.A. has been, for example, on the exclusion list of Norges Bank Investment Management (the manager of Norway’s sovereign wealth fund) under its ‘gross corruption’ category since mid-2018.

Also not helping JBS’ investment case is the US$199 million ($305 million) net loss it has just reported for 2023.

Bacon, chicken wings and steak

In late February New York Attorney General Letitia James filed a lawsuit against JBS’s American subsidiaries for misleading the public about its environmental impact.

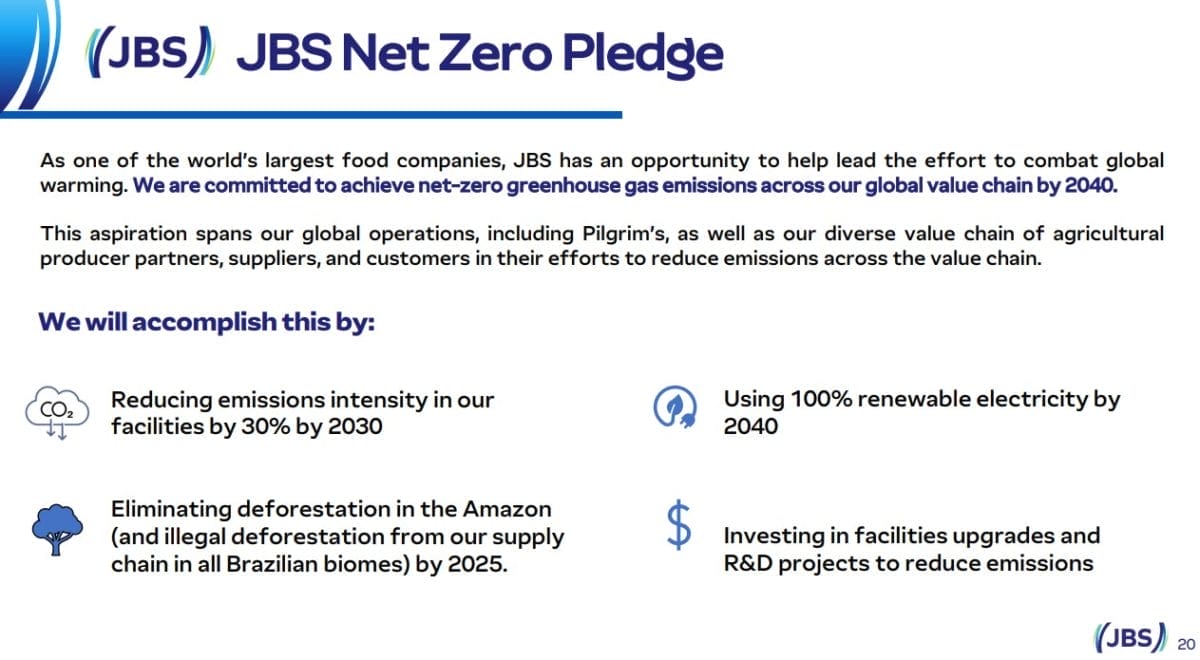

The lawsuit says that across its marketing materials, the JBS group has made “sweeping representations to consumers” about its commitment to reducing its greenhouse gas emissions claiming that it will be ‘Net Zero by 2040’ despite having “no viable plan to meet this commitment”.

The lawsuit claims JBS have used greenwashing and misleading statements to capitalize on consumers’ increasing desire to make environmentally friendly choices, by claiming amongst other things “Agriculture can be part of the climate solution. Bacon, chicken wings, and steak with net zero emissions. It’s possible.”

When making these promises, JBS had not calculated (and has still not calculated) the company’s total greenhouse gas emissions – including emissions resulting from deforestation in the Amazon – and therefore had no way of knowing whether it could successfully reduce those emissions to net zero by 2040.

JBS continues to make net zero claims as evidenced below in this slide from a presentation to proxy advisors in February.

Political pile-on

Fifteen US senators also recently joined the JBS pile-on, writing to ask the Securities and Exchange Commission (SEC) to “protect the integrity of US capital markets and the legal rights of US investors by exposing the risks that JBS poses to potential shareholders, including its track record of corruption, human rights abuses, monopolization of the meatpacking market, as well as environmental risks”.

The senators’ letter also noted JBS faces a pending SEC whistle-blower complaint (from NGO Mighty Earth) for making inaccurate claims when selling sustainability-linked bonds to US investors.

JBS’ Form F-4 Registration Statement lodged last year for its proposed NYSE listing admitted that given JBS N.V. will be a foreign private issuer, investors “will not have the same protection afforded to shareholders of companies that are subject to all of the NYSE’s corporate governance requirements”.

The senators’ letter therefore argued “US investors’ legal options would be substantially limited in the event majority shareholders acted in a manner that conflicted with or harmed their interests”.

The letter also noted the US Senate Finance Committee had recently conducted an investigation into JBS’ ties to deforestation and that the committee’s chair Senator Ron Wyden believed the company was “turning a blind eye as parts of its supply chain burn down the Amazon”.

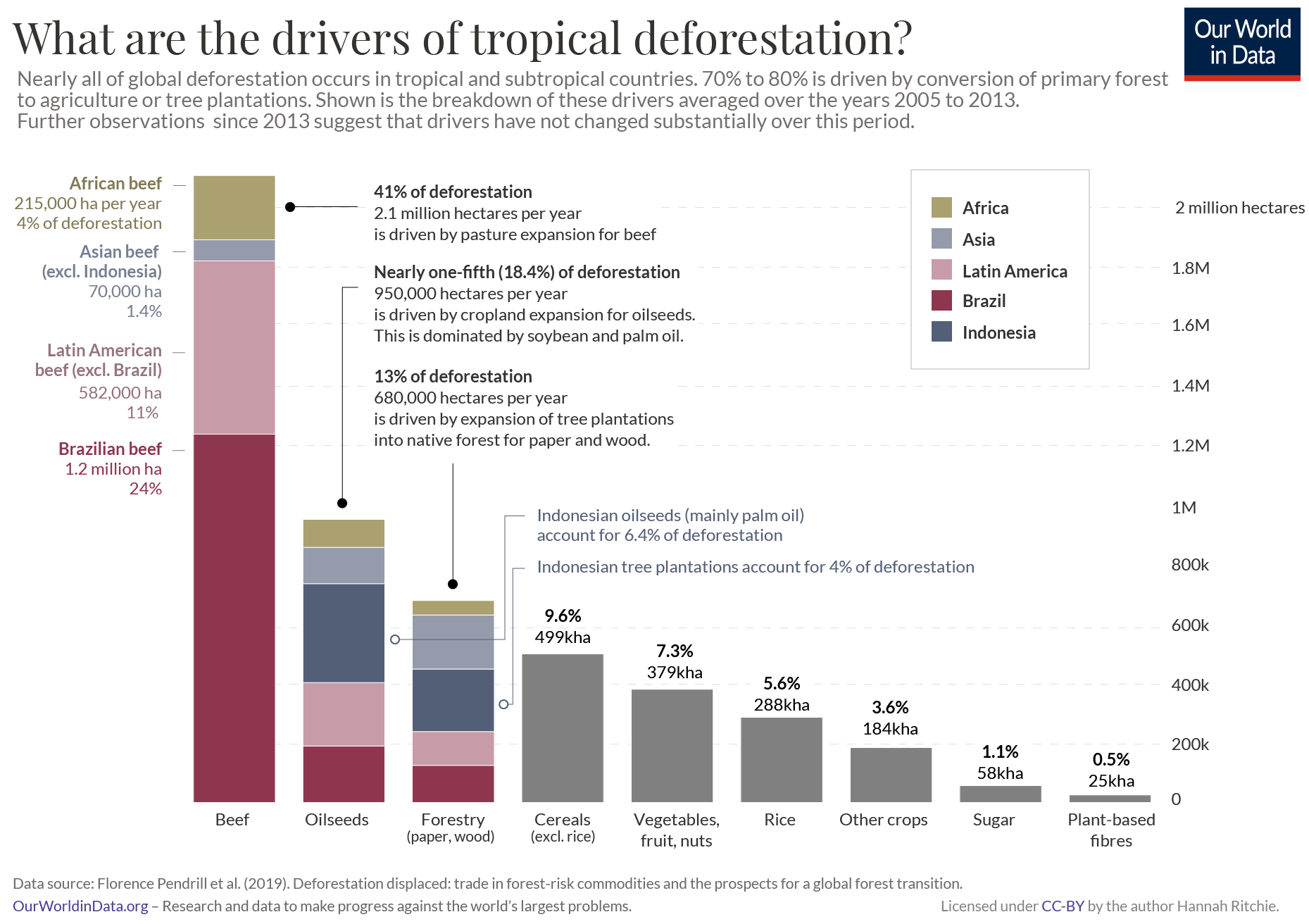

The graphic below highlights the extent to which beef – and especially Brazilian beef – contributes to global deforestation.

There have also been growing reports of what is known as cattle laundering or “beefwashing” in Brazil where ranchers take cattle born and raised on illegally deforested land and ship them to ranches with clean records to hide the fact they are the product of illegal deforestation.

There have also been growing reports of what is known as cattle laundering or “beefwashing” in Brazil where ranchers take cattle born and raised on illegally deforested land and ship them to ranches with clean records to hide the fact they are the product of illegal deforestation.

Reputational risk

JBS’ Form F-4 Registration Statement lodged last year for its proposed NYSE listing acknowledges the embarrassing problem of its controlling shareholders – and now soon-to-be-returning directors Joesley and Wesley, who are the sons of JBS founder José Batista Sobrinho.

The statement said “we are subject to reputational risk in connection with US and Brazilian civil and criminal actions and investigations involving our ultimate controlling shareholders, and these actions may materially adversely impact our business and prospects and damage our reputation and image”.

In 2017 Joesley and Wesley, among others, entered into collaboration agreements with the Brazilian Attorney General’s Office and a leniency agreement with the Brazilian Federal Prosecution Office following disclosures of illicit payments made to Brazilian politicians from 2009 to 2015.

The statement said JBS “cannot guarantee that negative news and publicity (whether or not factually accurate) will not be released in the future that involve our company, JBS S.A., our controlling shareholders”.

The brothers currently control 48.83 per cent of the voting power in JBS S.A. Under the restructuring, JBS N.V. will issue Class B Common Shares that are each entitled to 10 votes at general meetings that will see the brothers’ voting power jump to 85.03 per cent (and potentially reach 90.52 per cent).

JBS admits this dual-class structure “may result in a lower or more volatile” share price or “in adverse publicity or other adverse consequences”.

Index providers such as S&P Dow Jones and FTSE Russell have announced restrictions on including companies with multiple-class share structures in certain of their indexes.

Several stockholder advisory firms have also announced their opposition to the use of dual-class structures and they may “publish negative commentary about our corporate governance practices or otherwise seek to cause us to change our capital structure”.

Control

The proposed restructuring seems to hand the Batista brothers the ability to control the outcomes of corporate activities such as mergers and acquisitions; the sale of the JBS business to a third party and the election/removal of directors without minority shareholders having any say in the matter.

JBS says when Joesley (formerly JBS chairman) and Wesley (formerly CEO) are elected to the JBS SA board in April there will be 11 directors, seven of whom will be “independent”.

While the independents may form the ‘majority’ one imagines some intestinal fortitude will be required to make decisions not aligned with brothers’ wishes.

The JBS N.V. registration statement raised other governance concerns, noting the Batista brothers hold equity investments in other businesses “and may have an interest in causing us to pursue transactions that may enhance the value of those other equity investments, even though such transactions may not benefit us”.

Presumably, the statement will have to be eventually updated to note that the ultimate controlling shareholders that present reputational risk to JBS N.V. will also now be on its boar

Leave a Comment

You must be logged in to post a comment.