Modern super funds are hungry for data to improve member experience but Commonwealth Superannuation Corporation (CSC) chief customer officer Adam Nettheim says too much data can be a problem rather than an advantage.

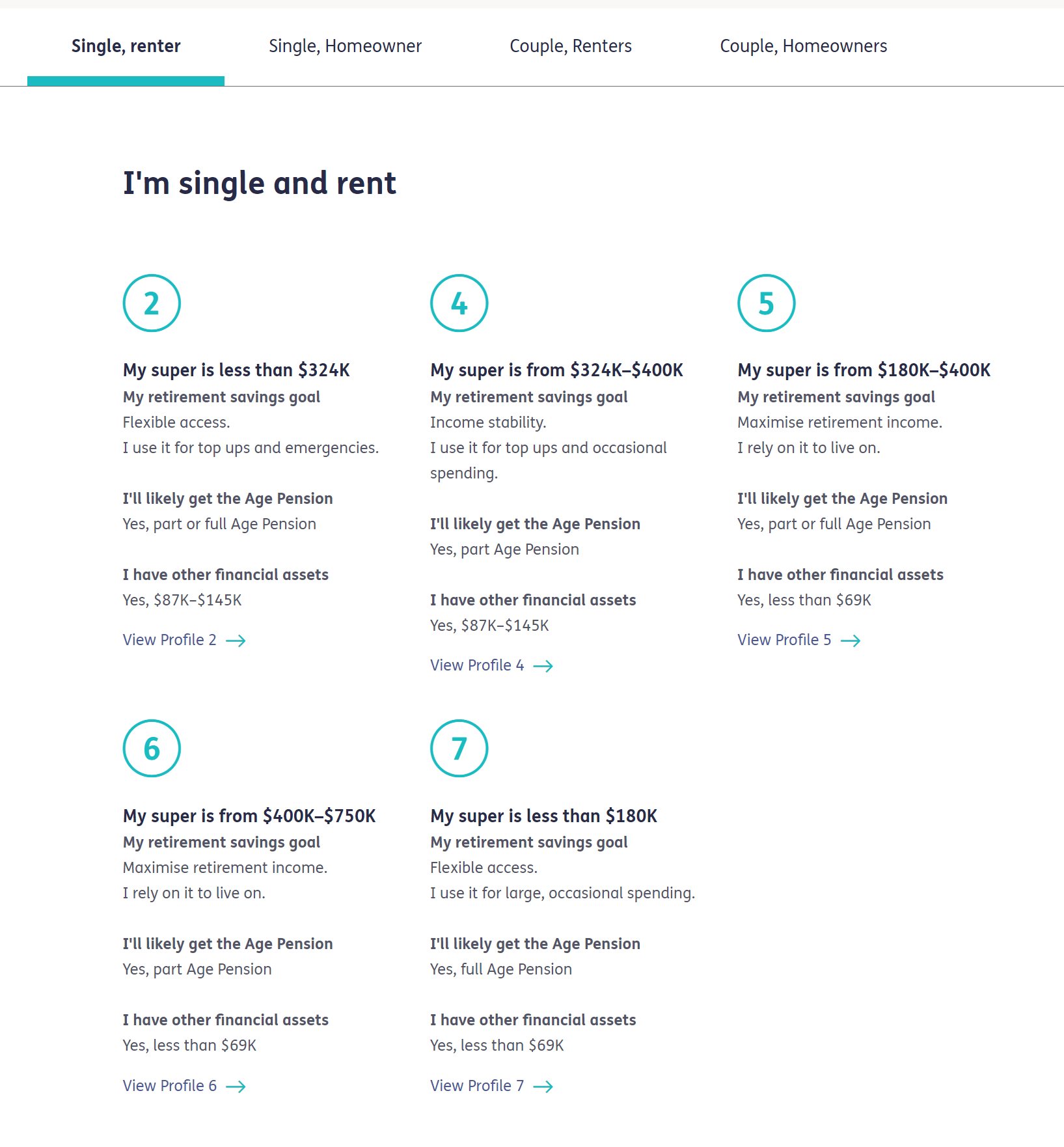

The public sector fund recently launched its Retirement Income Strategy (RIS) to support its Australian Government (APS) and Australian Defence Force (ADF) members, who were broadly categorised into 10 profiles based on their super balance, home ownership, and marital status.

These profiles were checked by an external actuarial group and published online, Nettheim says, so that members have access to them and can be nudged in the right direction when choosing their retirement income product.

The main data sources are member surveys and interviews, as well as the general public household income figures from the Australian Bureau of Statistics and Household, Income and Labour Dynamics (HILDA) in Australia survey.

“A lot of funds say we don’t have enough [data], and you wonder how much you have to have,” Nettheim tells Investment Magazine.

“For me, I don’t think we’re short of data. I think what you have to do is determine what data really matters. Some data is kind of interesting, but not influential in how you think or how you might think about your customer base.”

The comments resonated with regulators’ expectations as ASIC commissioner Simone Constant recently urged super funds to make good use of existing members’ information in developing an RIS.

“We understand that industry is concerned about the cost and privacy issues associated with collecting more data,” she told the Conexus Retirement conference in Canberra this month.

“That is not what we are asking funds to do. Instead, we are asking you to maximise the value of the data you already have.”

Nettheim’s team has been trying to simplify its data needs across a range of fund initiatives – including retirement – and has so far reduced the number of data sets it uses from 65 to 15.

“We find that the difference between the 65 and the 15 hasn’t actually changed the nature of what we do from that data,” he says.

“Then, of course, you get to the data that you would like to have, but you don’t have, which is the spending pattern stuff.

“For those people who are just retiring, we’ve got a bit of work to do there…we think we can set them up well, but if they outspend it [retirement income], then we haven’t really helped them get to the right outcome.”

Reducing the ‘cognitive load’

CSC wrote to 9200 members in the months leading up to 1 July this year when its retirement income solutions were released. And within the first month of going live, there were 100 applications to its account-based pension CSCri – normally there are only 40 to 50 monthly applications.

The fund’s internal “super specialist” team also have 150 appointments with members to consult on retirement products in the next month. These are great results, but Nettheim says there’s much more to do.

“We’ve seen an uptick in actual applications. We’ve seen a lot of traffic on our website from people getting onto pages and having a look.

“But I expect one of these days, we’re going to be spending a fair bit of time with those people who haven’t come forward with any interest to find out why not.”

Nettheim says CSC never expected the current RIS to be the ultimate rulebook. In fact, the fund already factored an “RIS 2.0” into its budget before the current iteration even came out.

“We’ll do a formal review at the 12-month period, but we’ll be doing informal reviews every three months from going live onwards.”

Nettheim says CSC won’t use retirement product signup as a measurement of success.

“I’ve been very clear and very much supported by the board and the CEO that we want people to take the product because it’s right for them, not because we’re trying to meet a sales target,” he says.

The real indicators of success would be an improvement in understanding members’ retirement needs, positive feedback from members, and the reduction of “cognitive load”, which Nettheim describes as a mental burden that retirees have when they grapple with the change of lifestyle in retirement (of which finances is only a small part).

“Particularly for some of our customers, if you look at military people, or the Australian Federal Police, or a lot of the public services [employees], they are really proud of the work that they’ve done, and then they suddenly lose their identity [in retirement],” he says.

“So how do people stay healthy, happy, connected to friends and family and all of those kinds of elements. Because having decent money in retirement is obviously important, but being happy in retirement is probably just as important.

“I do think one day, super funds will be compelled to help [with this cognitive load], because, ultimately, we’ve got all the funds under management. I think the government will say it’s up to you. You’ve got all the money.

“I’m trying to make sure that we’re an early adopter, if you like, into this space.”

CSC’s RIS products are developed for PSSap, ADF Super and CSCri members, as well as for defined benefit members who still receive contributions or have a have a preserved account balance.

Leave a Comment

You must be logged in to post a comment.