A little-known administrative hurdle is prohibiting tens of thousands of poorer Australians from accessing tax-free account-based pensions, according to analysis by The Conexus Institute*.

Most super funds have placed a minimum balance requirement on retirees – as much as $50,000 in some cases – to apply for an ABP, the analysis found. It estimates that around 50,000 Australians who are retiring over the next year may not be able to access ABPs because they don’t have enough savings and don’t meet the minimum thresholds imposed by funds.

At the Conexus Retirement Conference in August, APRA deputy chair Margaret Cole said funds are not doing enough to nudge members towards accessing better retirement options, as a significant number of retiree accounts – an estimated 750,000 – are still parked in an accumulation MySuper product as of March this year.

The fact that a significant portion of retirees is ineligible to even apply for ABPs only exacerbates the problem.

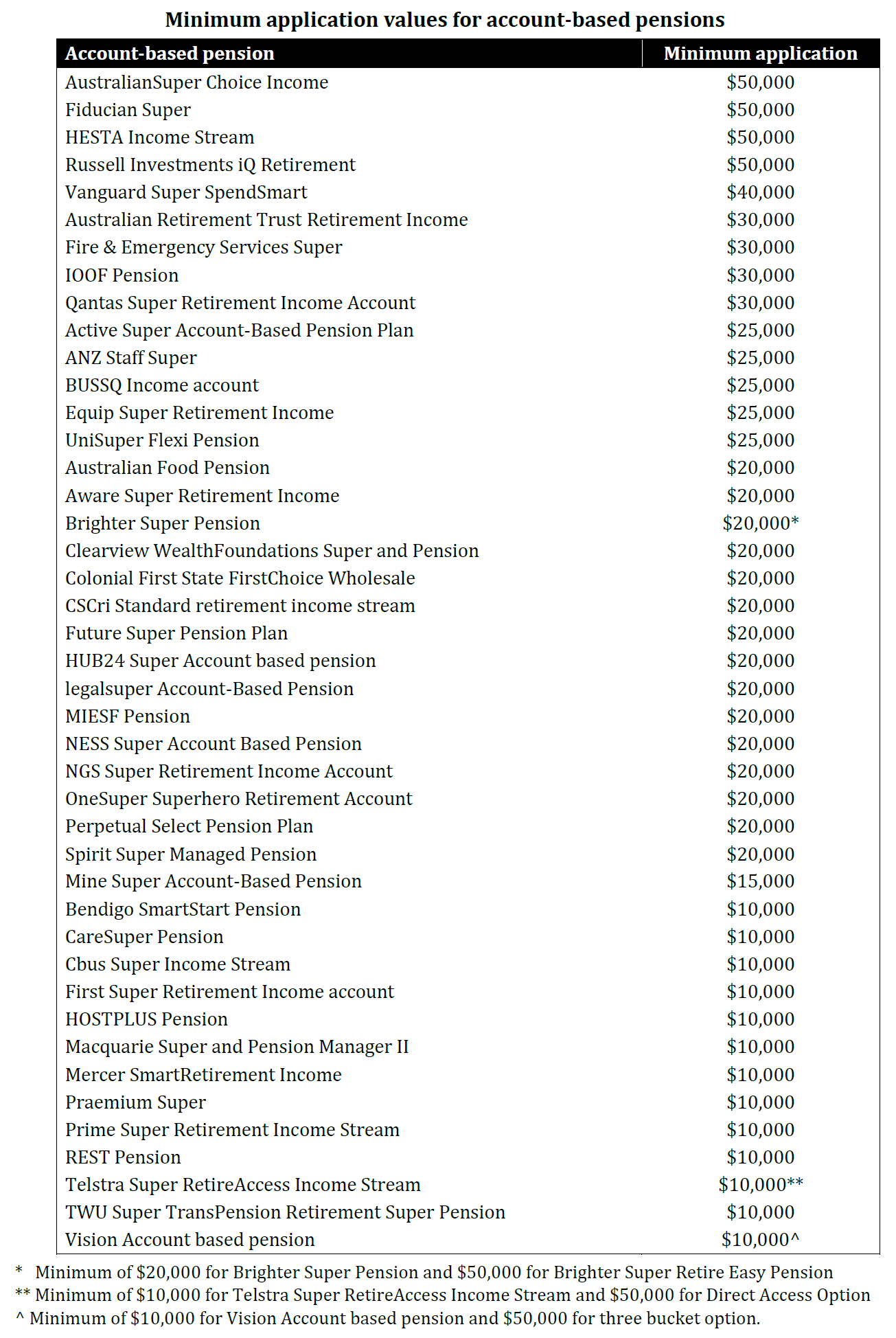

The analysis, co-authored by the institute’s executive director David Bell and research fellow Geoff Warren, reveals a list of funds with the steepest minimum application balance requirements, according to their own ABP product disclosure statements.

Topping the list were ABPs from AustralianSuper, HESTA, Fiducian Super and Russell Investment, each with a $50,000 minimum balance requirement.

These are followed by products from Vanguard Super with a $40,000 requirement, then Australian Retirement Trust, Fire & Emergency Services Super, IOOF and Qantas Super with $30,000.

ABPs with balance requirements at the lower end of the range include those from Prime Super, Cbus Super, Hostplus, REST, as well as those from Mercer, Macquarie, and Praemium. Members can access these products with $10,000 accumulated.

Some of these funds are known to serve members who have less retirement savings, such as REST, whose average member balance is $37,000, according to APRA fund-level data at the end of the 2023 financial year.

The analysis suggested that if low-balance retirees are prohibited from applying for an ABP, they would have “meaningful” disadvantage on tax. It said they are also potentially excluded from getting a retirement bonus where it’s offered.

“Low balance members may miss out on a tax-free environment that could easily provide a 0.5 per cent return uplift annually (relative to the comparable investment strategy applied in accumulation),” it said.

“The design features of Australia’s retirement income system include an accumulation phase that taxes contributions and income and a retirement phase that is tax-free.

“Precluding low-balance members from the tax benefits during retirement seems inconsistent with a fair and equitable system.”

The analysis also said it’s unclear what alternatives are available to low-balance members if they cannot access ABPs, and whether super funds are actively engaging with them about next steps.

“A generic message that there is a good retirement product while confronting members with minimum balance requirements that they may not meet seems like a poor communication practice, and may reduce member confidence,” the report said.

‘Outrageous’

Super Consumers Australia has blasted the minimum-balance requirement as “just wrong”, and SCA deputy director and former APRA official Katrina Ellis said funds are “compounding inequalities”.

“Funds don’t really have the right to deny members from receiving the tax benefits that you get with the retirement pay,” Ellis said, having joined the member advocate group from APRA this year where she was general manager of superannuation.

“It [the minimum] is just quite arbitrary, and something that the trustees appear to be doing for their own convenience ahead of the members best financial interests.

“HESTA – that is for nurses and women who have broken work patterns and so have lower superannuation balances – they’ve got one of the highest limits.

“It’s funny that nobody has seen it before, because once you see it, it’s really quite outrageous.”

AustralianSuper head of superannuation and retirement product Dena Brockie said the fund is currently reviewing the account balance minimums.

“The minimum investment requirement for our account-based pension fund is designed to create a robust and stable environment that benefits all members, with minimal cross subsidisation,” she said.

But Ellis called for the minimum application threshold to be scrapped completely and for the regulators to demand a “please explain” from trustees.

“To me, it seems like a breach of their [super funds’] best financial interest obligations to members… and the regulators could just take action against the trustees because they’ve broken the law,” she said.

“I don’t see any case for a nuanced position…or alternative minimum.”

The Conexus Institute analysis acknowledged the minimum application balance issue is complicated, considering that “operating a product with operational complexities and small balances is likely to be cost-ineffective” for super funds, and that many low-balance members may not make use of an ABP even if it’s available anyway as they prefer to withdraw the lump sum.

But still, some changes in funds’ approach would contribute to a “fairer system”, the analysis said.

“While the size of the affected cohort will likely shrink as the system continues to mature, this cohort will not entirely disappear, and a sizable number of Australian retirees appear to be impacted now,” it said.

“We think more should be done to assist these members.”

HESTA was approached for comment.

*The Conexus Institute is an independent think tank philanthropically funded by Conexus Financial, the publisher of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.