Produced in partnership with T. Rowe Price

Unlike the accumulation phase of retirement investing, during which most individuals share a common goal of saving as much as they can afford and growing those savings through investments, investors’ goals typically are more diverse during the decumulation phase.

As more defined contribution retirement providers evolve beyond exploring the landscape of available retirement income solutions to adopting an implementation‑oriented stance, we believe that the system could benefit from:

Research that fully appreciates and accounts for the trade‑offs inherent in individual retirement income needs and solutions; and

A common framework for evaluating retirement income solutions to help retirement providers evaluate products for their members.

To address this challenge, T. Rowe Price’s global multi‑asset research team, in partnership with our global retirement strategy team, has developed a patent‑pending five‑dimensional (5D) framework for exploring retirement income needs and potential solutions.

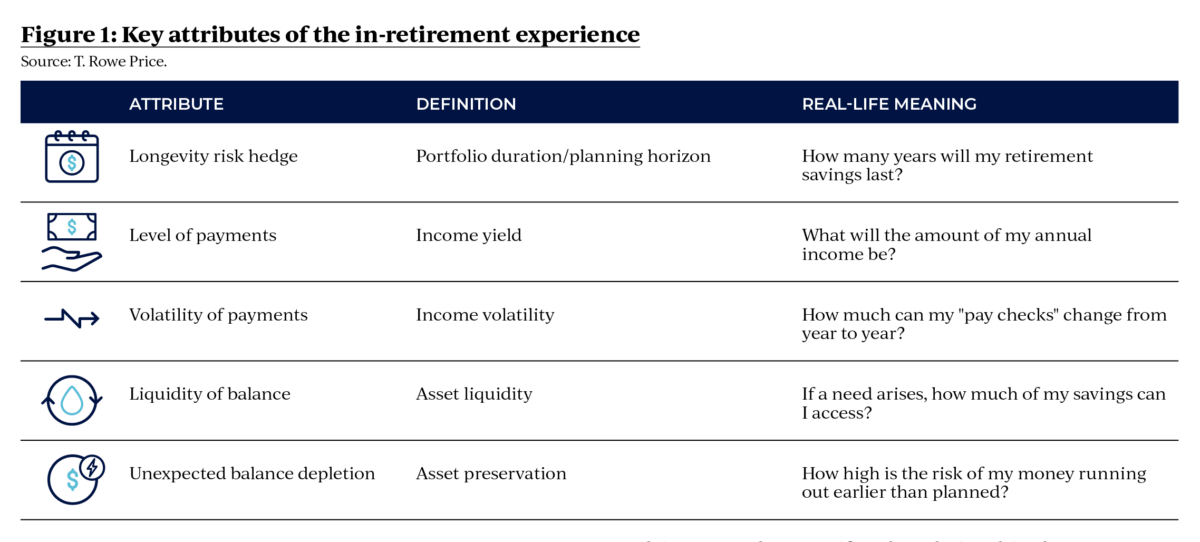

Our 5D framework establishes the foundational attributes of the “in‑retirement experience” for individual investors and quantifies the economic trade‑offs between these attributes.

Our unique approach starts with a simple assumption that every aspect of the in‑retirement experience is captured by at least one retirement income product currently available in the marketplace.

By comprehensively reviewing the existing universe of retirement income solutions and analysing the trade‑offs inherent in various product designs, we were able to identify five key attributes that are specific, mutually exclusive, exhaustive and that we believe fully characterise the in‑retirement experience (Figure 1).

Using these five attributes, we then analysed various retirement income solutions to identify and articulate the trade‑offs inherent in each solution, such as understanding how a specific solution balanced the goal of hedging against longevity risk with the objective of achieving a desired level of income payments.

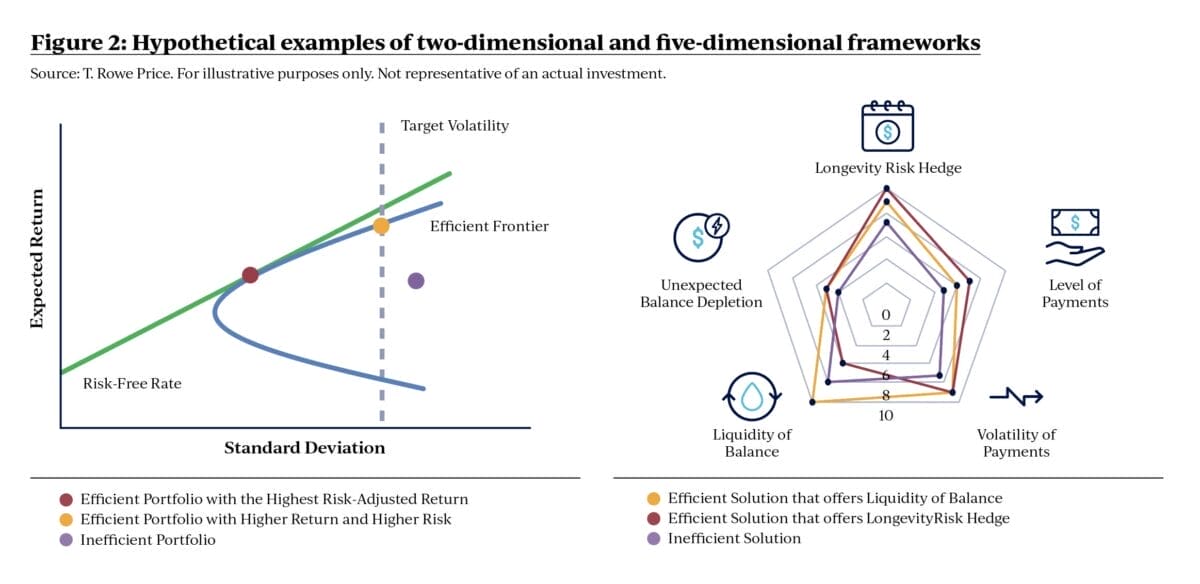

Our research revealed a parallel between our 5D framework and the traditional risk/return investment trade‑off. The 5D framework enabled us to conduct quantitative studies of retirement income solutions based on various well‑defined metrics, similar to how the risk/return trade‑off has been studied for decades.

A framework for evaluating retirement income solutions

While traditional metrics such as risk‑adjusted returns and the familiar mean‑variance frontier may suffice for traditional investments during the accumulation phase, retirement providers and their consultants or advisers need a more sophisticated approach to evaluate retirement income solutions.

Leveraging the five key attributes in Figure 1, we use our 5D approach to analyse how various retirement income solutions prioritise these five aspects of the in‑retirement experience.

We believe our 5D approach better captures the diverse needs and preferences of retiree populations and, importantly, quantifies the relationships between these preferences.

For example, in the accumulation phase, investors primarily seek to achieve the highest return possible for a given risk budget, which typically grows more conservative as they near retirement age.

During decumulation, risk and return are still important metrics but fall short of fully representing investors’ objectives at the point of retirement, which tend to be more varied and unique to each individual.

Because the in‑retirement experience includes these five attributes, potential solutions must be optimised against five dimensions instead of the traditional two – risk and return – that dominate the accumulation phase (Figure 2).

How does the 5D approach differ from existing frameworks?

In addition to establishing the five key attributes by which a retirement income solution can be evaluated, our 5D framework captures and quantifies the trade‑offs that a retiree must make in prioritising across these attributes. Much of the retirement income research conducted to date has focused on identifying retired participant preferences – e.g. “I want a guaranteed stream of income” – but failed to consider the other side of the ledger – e.g. “I am willing to give up X per cent in monthly income to achieve that goal.”

Under the financial market efficient frontier, our 5D framework quantifies retirement income needs by precisely calibrating trade‑offs between the five attributes and assigning quantitative values to each of those attributes based on well‑defined metrics. Quantifying participant needs for each of the five attributes allows us to identify how members would spend their savings to create desired in‑retirement experiences.

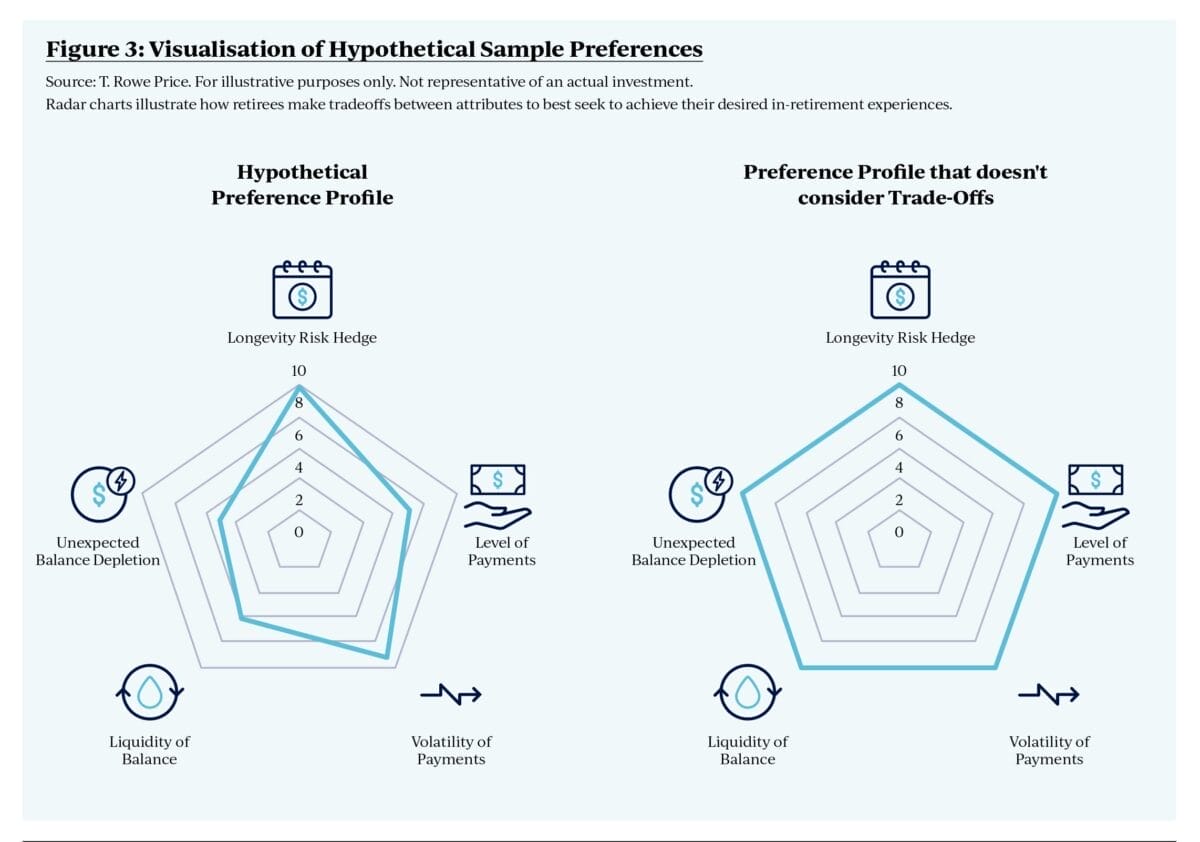

Using a radar chart (a way of displaying multivariate data on an axis with the same central point), we can quantify and visualize these trade‑offs.

For example, consider the radar charts in Figure 3. The chart represents one possible hypothetical preference profile for the in‑retirement experience. A retiree with this preference shape is primarily concerned about hedging against longevity risk—perhaps because of a family history of great health—and wants guaranteed income for life. This hypothetical retiree also prefers a stable income stream to allow for better travel planning in retirement, but wants a higher income level (measured as a percentage of balance) to compensate for past under saving.

Given these priorities, the retiree is willing to accept a moderate level of balance depletion risk while giving up some liquidity under the efficient frontier constraint. As one can imagine, preference profiles for different retirees can and do vary widely because of differing in‑retirement needs. Because preferences can change across all five dimensions, the range of desired in‑retirement experiences can be immensely diverse.

Figure 3 also highlights the difference between our 5D framework and those retirement income studies that fail to consider the trade‑offs inherent in retirement income products. There will be only one preference profile in such studies—a perfect pentagon in which maximum values for all five attributes are selected (as shown in the radar chart on the right in Figure 3) without acknowledging that it is impossible to attain all five under the efficient frontier.

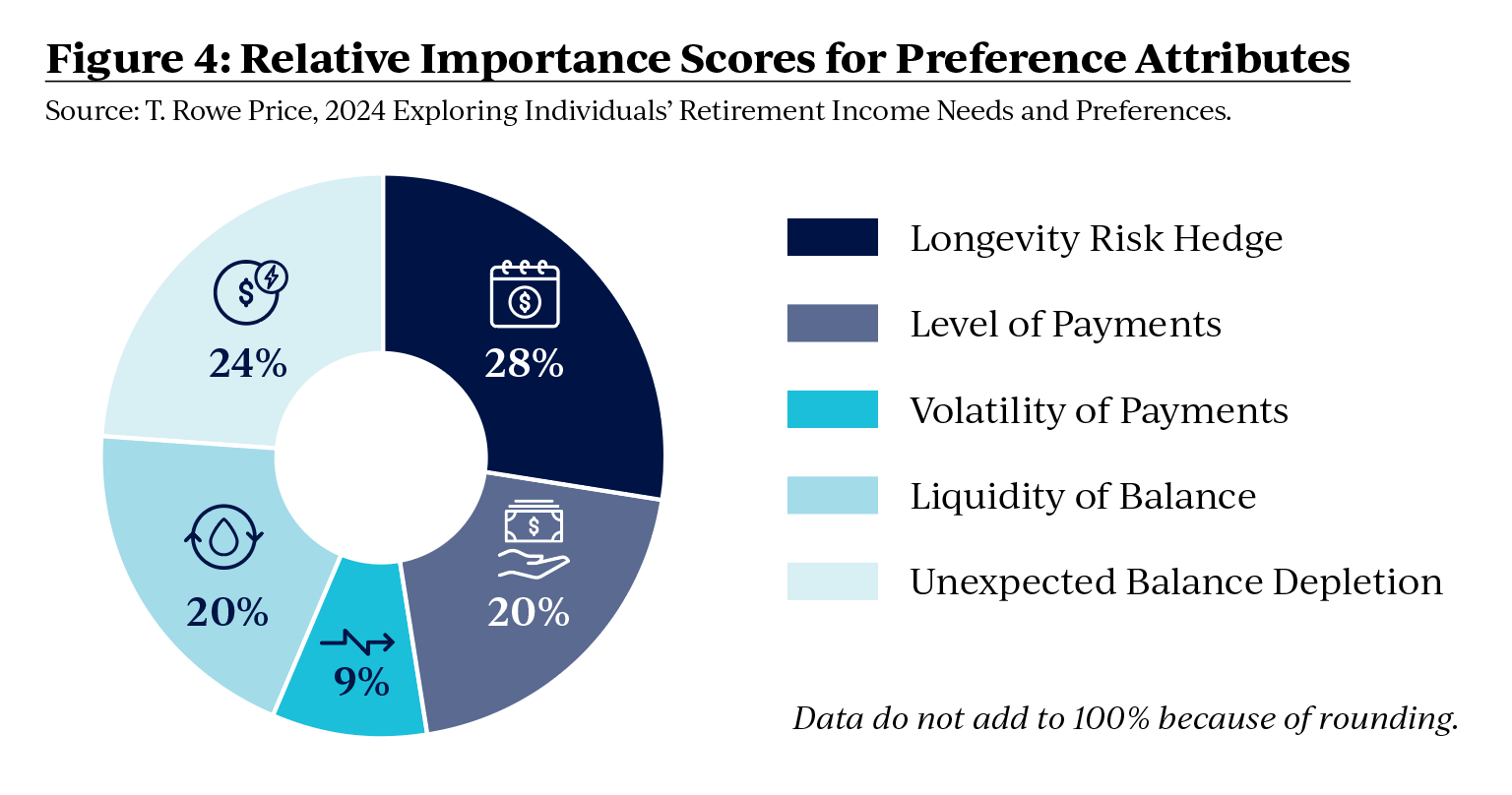

Rowe Price’s proprietary 2024 study of approximately 2,500 individual investors in the US shed light on how investors, as a group, actually prioritised each of the five in‑retirement attributes (Note 1)

As illustrated in Figure 4, the data indicated that individuals who were approaching or in retirement were most concerned about how many years their savings would last (longevity risk), followed by the risk that they might run out of money earlier than expected (unexpected balance depletion). Level of payments and liquidity of balance were assigned equal importance, while volatility of payments was viewed as the least important attribute by the investors surveyed.

Potential applications of the 5D framework

(See note 2.)

Once a retirement provider understands the distribution of preferences within their member population—whether that’s based on a member survey or a qualitative review that prioritises the five attributes—we think they will be better positioned to identify potential solutions that prioritise the needs of that population.

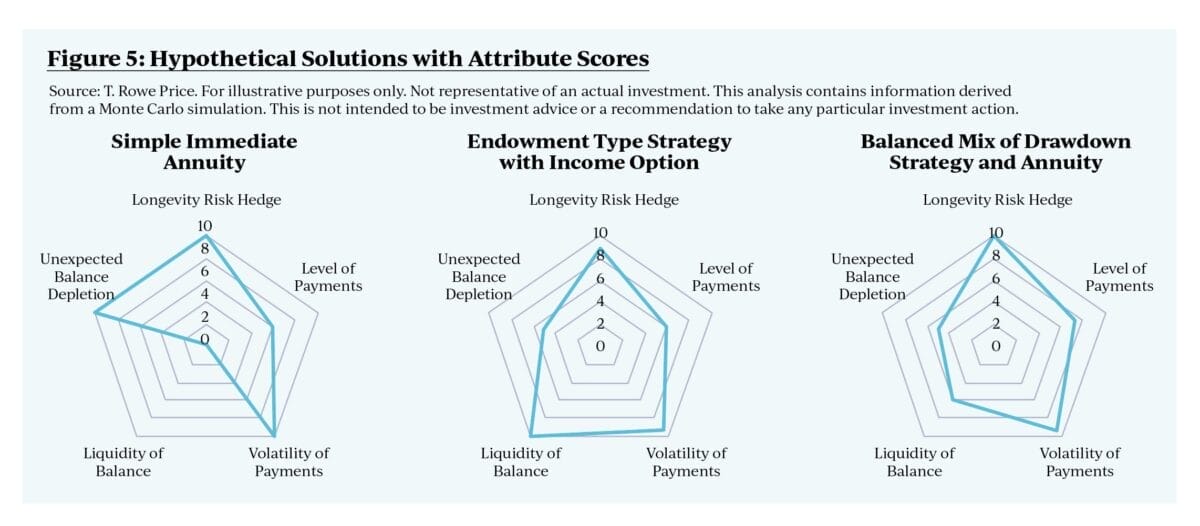

Similarly, retirement income products can be plotted using our 5D framework to visualise which products appear to align best with the provider’s retirement income priorities (Figure 5).

Notably, the 5D framework provides an opportunity to compare different retirement income products using a uniform and unbiased process, much like mean‑variance optimisation can be used to compare products suited for traditional investments. The 5D framework shows how a retirement income product scores across each of the five attributes, and this output can then be compared with the same output for another product.

Retirement providers, in partnership with their consultants or advisers, can compare the findings of a 5D analysis and the specific retirement income needs of their member populations to identify “best fit” solutions. Any retirement income solution can be analysed using our 5D framework under a commonly accepted set of capital market assumptions to understand and quantify how well the product meets each of the key attributes.

We believe our 5D framework is a novel approach that offers superannuation funds the ability to better understand the unique preferences of their members, enabling them to narrow the retirement income product universe to the solutions that are most likely to meet the needs of their unique populations.

Notes:

1. Exploring Individuals’ Retirement Income Needs and Preferences. T. Rowe Price. 2024 . Data reflect responses from 2,582 individual investors age 40 to 85 that were currently enrolled in a DC plan and had at least $100,000 saved in their plan accounts. The survey was fielded December 2023 through February 2024.

2. The methodology used for our hypothetical case study is a proprietary method developed by T. Rowe Price that combines traditional quantitative investment research techniques, such as Monte Carlo simulations, and a quantitative marketing research method commonly used to understand consumer preferences. Fees and other expenses associated with actual products were not considered in our analysis.

Dr Berg Cui is senior quantitative investment analyst and Jessica Sclafani is global retirement strategist at T. Rowe Price. Contact your T. Rowe Price representative to learn more about applying our 5D approach to your evaluation of retirement income solutions. To read the full paper and learn about the study methodologies, please click here.

Leave a Comment

You must be logged in to post a comment.