Retirees differ in many ways, including personal and financial circumstances and how they engage with transition into the “retirement phase”. This is why the principles-based Retirement Income Covenant (RIC) is a clever foundation for Australia’s retirement system. It affords super fund trustees the flexibility to meet the varying needs of members. However further policy is required because current policy settings don’t provide clear expectations and facilitate laggard funds.

We advocate for a retirement licensing regime (Note 1) as the next step. It addresses many of the challenges that are limiting progress towards a high-quality retirement system. Further, it can preserve the merits of a principles-based approach by being framed around the capabilities that trustees are expected to have in place to meet their obligations under the RIC. Taking this policy step sooner rather than later would establish the commitment required from super funds, institute minimum standards, and help resolve regulatory uncertainty.

Navigating a challenging pathway forward on DC decumulation

Defined contribution (DC) systems are becoming increasingly prevalent around the globe. While DC systems have largely worked well during accumulation, the decumulation phase is far from resolved.

The flexibility of DC systems matches up well against the challenge of meeting the needs of a highly diverse set of retirees. It supports household balance sheet management, integrates with other income sources and facilitates variable spending plans.

The principles-based RIC is a good match for a DC pension system. It creates an obligation for trustees to support their retiring and retired members, while providing super funds with the flexibility to meet the diverse needs of retirees.

Australia’s system may fail to reach full potential in its current state

The scorecard is mixed regarding development of retirement income strategies (RIS). There has been some progress, but there is much more to be done. Of particular concern is the large dispersion across funds in terms of the development and quality of their RIS.

The recent APRA/ASIC “Pulse check on retirement income covenant implementation” is illuminating. Forty-eight registrable superannuation entities (RSE) licensees responded to the survey. The statistics below focus on fund initiatives with projected timeframes of one year or longer (or unknown):

Understanding members’ needs: half said they plan to improve by interrogating existing member data, while two-thirds plan to actively seek to identify and address data gaps.

Designing fit-for-purpose assistance: 55 per cent said they plan to uplift information provision, with 46 per cent planning to provide some sort of advice.

Overseeing strategy implementation: half said they are planning to integrate their RIS into their broader business planning process, while 70 per cent intend to design and implement measures to assess the impact of their RIS.

These results are quite alarming given that these areas are foundational to developing and maintaining an effective RIS. It is quite possible that the majority of surveyed RSE licensees will not be on top of these key areas within

three-years of the RIC being implemented.

Next-step activities such as upgrading governance, developing integrated retirement solutions that blend investments, longevity products and drawdown plans, as well as approaches for assisting the disengaged, all feel a long way off.

APRA deputy chair Margaret Cole recently said that “the pace of change could be a great deal quicker” (note 2). ASIC commissioner Simone Constant said that “quite frankly, our patience is running thin – we want to see meaningful action now” (note 3). We share the palpable frustration of regulators.

It is far from assured that Australia’s retirement system will reach its potential under current system settings, even if given time. And time should not be viewed flippantly. Around 250,000 people enter retirement age each year. Delayed progress means many in each year’s cohort will not receive the retirement guidance and solutions they need.

The question is how to get the super industry at large committed to developing quality RIS at a reasonable pace. Before discussing how a licensing regime may help, we first outline the challenges that are inhibiting progress.

Six challenges to further progress

Our research identifies the following primary challenges inhibiting RIS development:

1. Inability to rely on market forces to drive progress on retirement.

Traditional economic models rely on market forces to drive innovation and efficiency, stemming from informed consumer choice and competition amongst providers. Unfortunately, these forces are weak in retirement. Retirement is complex and many retirees (for various reasons) find retirement decision-making hard and do not drive effective competition. For funds there is little financial reward for being a leader or penalty for lagging on retirement.

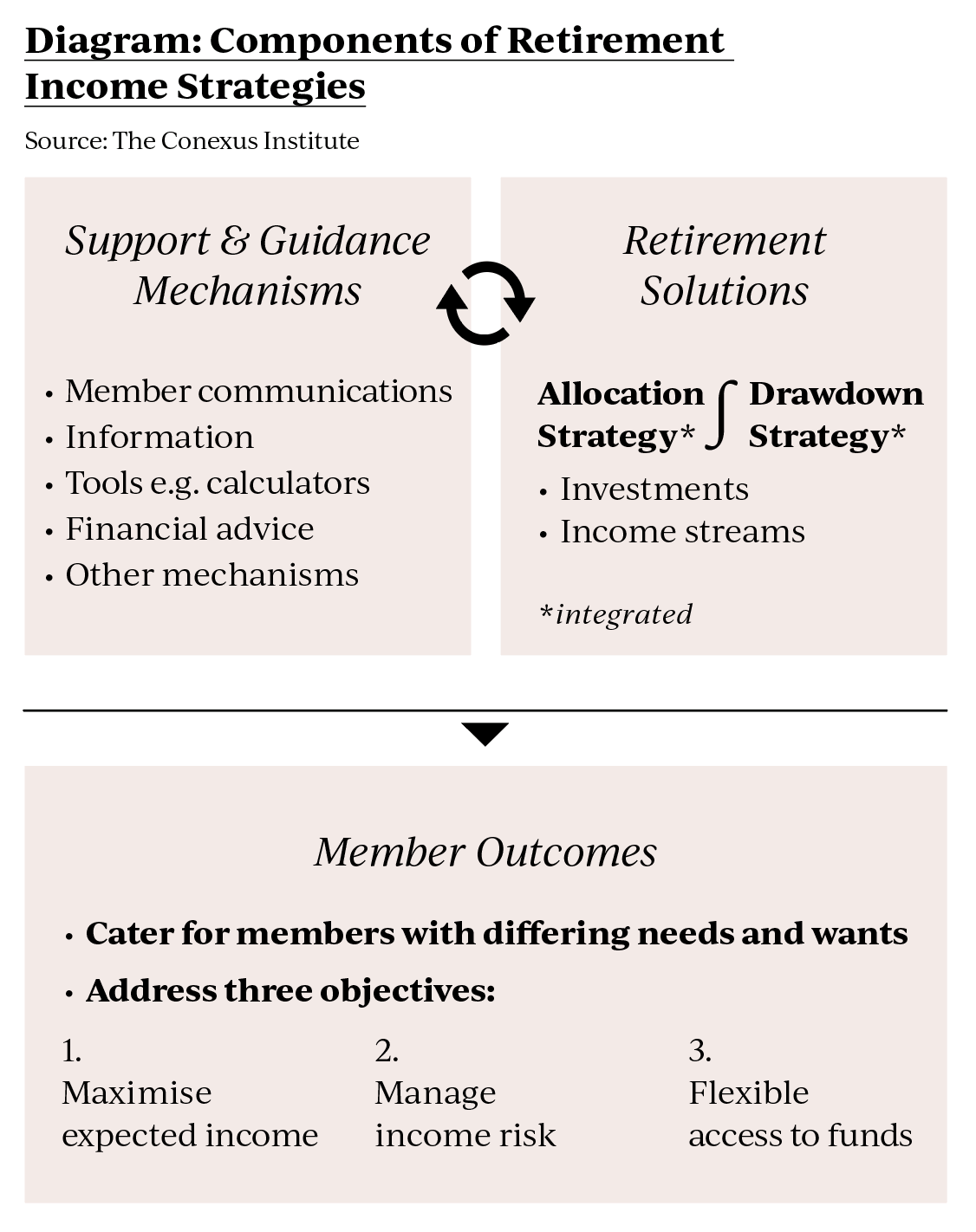

2. Difficulty of catering for diverse member needs.

Retirees differ along two main dimensions. One is their personal circumstances and preferences. The catalogue of circumstances that matter in retirement is broad, and at a minimum must include total financial resources, homeownership and household structure. Meanwhile understanding member preferences and how they view key trade-offs remains an underdeveloped area. The second dimension is how members want to engage. As identified recently by APRA’s Cole, a fund’s membership includes the advised, the self-directed and the disengaged. To that list we would add those that would like assistance from their super fund. Catering to all members is a complex and costly exercise, and a challenge for funds used to operating in an accumulation sector with default settings.

3. Lack of prioritisation of retirement by super funds.

A common feature of funds making real progress is that retirement has clearly been prioritised. However, many funds appear to have not made retirement a priority. This could be due to a tenuous business case (such as a small retiree cohort), cross-subsidisation concerns, policy uncertainty motivating deferral, or competing strategic priorities. While regulatory pressure may prompt some action, there is a risk of superficial activity.

4. Uncertainty around future regulatory assessment.

Current regulatory settings for assessing progress of RIS development consist of integration into APRA’s outcomes assessment standard (SPS 515) and the regulators adopting an “engage-and-share” approach comprising joint thematic reviews and surveys, accompanied by strong rhetoric imploring funds to make more progress. These settings provide little clarity around future expectations and assessment practices, while fund RIS are becoming more detailed. At some point expectations and assessment will evolve, creating the significant risk of unintended consequences and retrospectivity issues. Regulatory uncertainty hinders innovation and incentivises a wait-and-see approach from funds.

5. Policy and regulatory settings restricting trustees in providing personalised retirement advice and guidance.

The economics and the supply shortages in traditional financial advice motivate the need for a scalable and low-cost mechanism for super funds to provide retirement guidance and advice to their members. We acknowledge significant policy intent on this issue and that Phase 2 of the Delivering Better Financial Outcomes reforms may improve pathways forward. Nevertheless, progress in this area will remain inhibited until the policy uncertainty is resolved.

6. Retirement ‘frictions’ make navigating retirement difficult for consumers.

Consumers face difficulties in navigating retirement in terms of both understanding and implementing what they need to do. There is complex jargon and inconsistent labelling. Opening an account based pension (ABP) is not always straightforward. ABPs cannot accept contributions. It is cumbersome to switch retirement providers. All this deters retirees from meeting their retirement needs and suppresses competition.

Next step: a retirement licensing regime

Under a retirement licensing regime, super funds could choose to apply for a licence to provide retirement services to their members including guidance, advice and retirement solutions. Funds would need to meet licensing requirements, which we envisage being based around the capabilities required to deliver retirement services of a reasonable quality. A retirement licensing regime can be broken into three simple components:

Clear capability-based criteria that act as licensing requirements for RSEs to be able to provide retirement services. We consider the high-level requirements to be self-evident:

- Capability to guide and advise a large range of different member types into appropriate retirement solutions;

- Capability to design and deliver tailored retirement solutions that potentially consist of investments via an ABP, a longevity product, and a drawdown plan; and

- The competencies required to deliver and maintain oversight of a RIS, such as suitable governance and management structures and resources such as systems capabilities.

Regulatory assessment that is linked to the licensing requirements. This means that the assessment would be based around whether a fund has maintained and developed the required capabilities to deliver a reasonable quality RIS.

An opt-out option for RSEs that choose not to provide retirement services to their members. There would be an accompanying requirement to follow a set of prescribed rules to ensure members find their way to another retirement provider, for example, by engaging with members prior to retirement and referring them to another fund. In effect, non-licensed funds would be choosing to be accumulation-only funds. The result would be that the super system’s retirement frontline would consist of funds that are committed to retirement. Further, linking ongoing assessment by regulators to the capability-based criteria would help to address regulatory uncertainty.

The table below considers the licensing regime proposal against the first four challenges, noting that the fifth and sixth challenges are somewhat distinct and are being addressed separately.

Table: Licensing Regime Proposal

| Challenge inhibiting super system progress on retirement | How retirement licensing addresses the challenge |

| Inability to rely on market forces to drive progress by funds on retirement | Licensing regime would ensure minimum standards, where market forces would fail to do so |

| Difficulty of catering for diverse member needs | Capability-based requirements would clarify the minimum degree to which diverse member needs must be catered for |

| Lack of prioritisation of retirement by some super funds | Clarifies minimum requirements to be a retirement provider, affording a clear business decision

Opt-out mechanism provides a decision point for funds, and allows uncommitted funds to sit out Ensures that retiring members will not be serviced by funds operating beneath minimum standards |

| Uncertainty around future regulatory assessment | Significant clarity created around medium-term regulatory assessment |

The benefits of a retirement licensing regime would flow in particular to retirees. In addition, super funds would benefit from regulatory clarity, and the regulators from having an effective lever to move the industry forward.

Feedback so far

We are seeking feedback on this proposal. While we will reach out directly to many reading this article, there is no need to wait if you have perspectives to share.

Here are some of the insights we have received so far, along with our reflections:

A number of people express concerns about what future regulatory assessment would look like for retirement, and see benefit in clarifying the future regulatory environment.

Some question the need for the licensing mechanism, suggesting that simply establishing capability-based criteria would deliver the majority of benefits. We consider that without a harder penalty for not meeting the requirements, and without a clear opt-out, laggard funds will continue to deliver sub-standard outcomes for retirees.

We have heard concerns over additional regulatory burden. While there is some truth in this objection, the licensing regime would only be requiring funds to establish capabilities they should have anyway, and regulatory burden and cost is reduced for funds that opt out.

Some people expressed the view that, by the time a retirement licensing regime came into effect, most of the industry will be in good shape. We wish we could agree. The current trajectory leaves much to be desired with significant dispersion across funds. Further, announcing the intent to introduce a licensing regime would have an immediate impact on fund behaviour. Establishing capabilities-based licensing requirements would sharpen industry focus. All this brings forward the realisation of benefit to retirees.

Reflecting on this last piece of feedback has only strengthened our belief in the merits of the retirement licensing regime. We are cognisant of timeframes, with around 250,000 Australians entering retirement age each year. We challenge policymakers, regulators and those funds leading the way on retirement to think at a system level by considering what happens to the members of those funds that are lagging. We cannot envisage a better way to avoid these members being left languishing in funds with sub-standard retirement strategies.

Through the lens of both time and system-level outcomes, we are strong advocates for a retirement licensing regime. It would ensure a system of fit-for-purpose funds maximising the flexibility afforded by the principles-based RIC to meet the diverse needs of retirees in a modern world.

Dr David Bell is executive director at The Conexus Institute and Dr Geoff Warren is research fellow at The Conexus Institute and Honorary Associate Professor at the Australian National University. The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Retirement Magazine.

Notes:

1. This article extends on Green Paper: A retirement licensing regime, by David Bell, Jeremy Cooper, and Geoff Warren.

2. Speech to the Conexus Retirement Conference, Margaret Cole, APRA. 2024

3. A guide to ‘good’: delivering better retirement outcomes and member services for Australians, Simone Constant, ASIC. 2024.

Leave a Comment

You must be logged in to post a comment.