At Chant West we spend a lot of time assessing superannuation funds, which includes the retirement offering of each fund. When we talk about retirement offering, we’re not just interested in the destination – the account-based pension product that most people end up in. We are also interested in how funds help members along the journey before they get to a pension product. So, what do we believe makes a great retirement offering?

At a high level, it means products and investments that a member needs to meet their retirement goals, the guidance and advice to help put these together into a strategy, and then making it easy to implement that strategy.

Different objectives

A great retirement offering shouldn’t look just the same as in accumulation, as the objectives of retirement are very different. Accumulation is focused on growing your super balance through strong returns over many years – it is all about growth. But in retirement, it is also about managing risk, as you don’t have decades to make up any fall in value.

The different objectives between retirement and accumulation suggest different strategies may be required – not just a rehash of accumulation.

So what do we look for in the main areas of investments, product and guidance/advice?

Investments

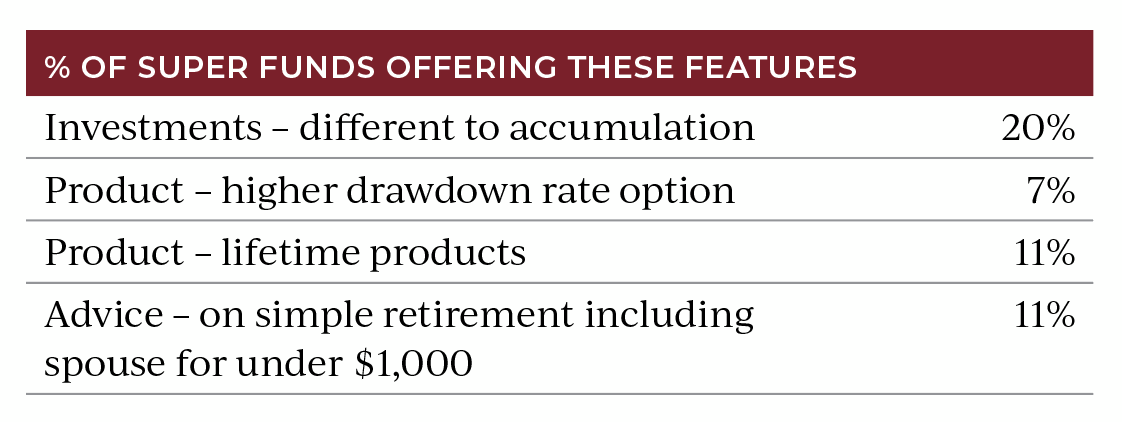

Ideally, funds should offer a range of well-performing diversified investment options across different risk profiles, to cater for the needs of different retired members. Almost all funds offer these, but they are almost always exactly the same as accumulation options, even though there is zero tax in the retirement phase and they are pitched at members who are more risk-aware.

Only a small number of funds invest differently in retirement. Some notable examples are Aware Super and TelstraSuper, both of which have unique asset allocations and tailored equity investments for retired members that focus more on lower volatility and franked income. We believe these types of strategies should have a place in most retirement offerings, and the primacy of member outcomes for all members should drive funds to seriously consider this.

Product

The traditional approach has been to provide an account-based pension which is just like an accumulation account, but the money goes out rather than coming in. But the problem of how best to work out how much to draw down, one of the trickiest problems in finance, remains in the lap of each member. Members set up a strategy and hope that sequencing and longevity risk don’t mess it all up.

The good news is that an emerging range of lifetime income products provide another lever to help members meet their retirement goals. And we are seeing a coalescing around products that offer a market-linked income for life, where an external insurer covers longevity risk that are only 60 per cent Age Pension assessable. The early reports from these products is that members are drawing down much more income, as they are now confident their money will last and they get more Age Pension.

Another aspect of product is the drawdown rate – the level of annual income drawn down by each member. The pension application forms in most funds set up the legislative minimum rates as a quasi-default and about 50 per cent of members take that. But many retired members could have a much higher standard of living than they currently have. AustralianSuper and NGS Super, for example, offer a set of higher drawdown rates to address this issue.

So if we believe that members with the right investments and product settings will have better outcomes, how can funds help members get set up with what’s right for each of them based on their individual circumstances?

Guidance and advice

Funds need to start with education on retirement issues, delivered through a range of channels. Online information should clearly explain what types of products and investments suit members in different circumstances – case studies are really useful for this.

Retirement seminars should be offered to explain how to get the most out of a fund’s retirement offering.

Retirement calculators need to help members answer the key questions, such as how much income can I draw down, and what products/investments should I choose? And it should show a member approaching retirement what they can do to improve their retirement income. While most funds provide reasonable retirement calculators, few cater for the member already in retirement who just wants to see whether they can keep drawing down their current income.

Member online portals and apps are also important to conveniently show members their balance but also what income they can expect in retirement. It can also be used to deliver highly personalised nudges to direct members to make the choices that best suit them.

The best way to get members well set-up in retirement should include member input about their situation, preferences, goals, and so on. And this is best achieved through personal advice. At the moment, advice is generally either basic and free (investment choice) or full and expensive (for example, $5000). Most funds provide personal intra-fund advice on investment choice, additional contributions, insurance, and the like, but provide members with very little advice to set up their retirement strategy. Members are largely on their own, unless they pay for comprehensive advice.

Funds need to find a way to deliver the sort of one-off advice most retirees need at the point of retirement. This should cover which investment options to choose, the need for a lifetime income product and how much annual income can be sustainably drawn down – all of which should be based on the member’s super balance and other assets, as well as those of their spouse.

But this sort of advice is currently provided by very few funds, even though the potential demand for this advice is greater than both basic and full advice. A few funds like TelstraSuper and Russell now provide advice like this for less than $1000. We believe this is the biggest missing piece of super funds’ retirement offerings, as it is very difficult for members to navigate all these retirement decisions without help.

While Tranche 2 of Delivering Better Financial Outcomes should make this more possible, we believe that more can be done now – and indeed some funds are showing that this is possible.

Funds can also use digital advice, where a member enters all their information, and the tool provides a recommendation. Or better yet, a hybrid version, where members can start digitally and move to an adviser for any questions, or to confirm they are doing the right thing.

We believe guidance and advice is the most important part of a retirement offering. If a fund doesn’t do a really good job in this area, they are unlikely to get their members to where they need to be in retirement.

Ian Fryer is general manager of research house Chant West. He is a member of The Conexus Institute Advisory Board. The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Retirement Magazine.

Leave a Comment

You must be logged in to post a comment.