On the first Saturday in March 2016 Jenny Oliver was at her local netball courts in Sydney, but she wasn’t watching when her daughter scored a goal. Oliver, who heads up the group insurance division of Australia’s largest life insurer TAL Life, had missed it because both eyes were glued to her smartphone watching the comments unfold on a story the Sydney Morning Herald was running about alleged improper claims handling practices at rival CommInsure.

The media investigation, led by journalist Adele Ferguson for Fairfax Media and the ABC’s Four Corners program, centred on revelations made by CommInsure’s former chief medical officer turned whistleblower Dr Benjamin Koh about the use of inconsistent and outdated medical definitions. It also contained video testimonials from disgruntled customers with heart-wrenching personal stories.

Commonwealth Bank of Australia chief executive Ian Narev had apologised, while strongly denying any systemic wrongdoing inside the bank’s life insurance division.

All the CommInsure clients interviewed by Ferguson had taken out their policies either directly or under advice, but the news story going viral online drew attention to the fact that most Australians are automatically signed up for default life insurance cover via their superannuation fund.

It was the start of a public relations nightmare for the whole sector.

“I think a lot of people in the industry remember where they were when the news broke that Saturday morning about the denied claims,” REST Industry Super chief operating officer Andrew Howard says.

“I was in a campsite with a bunch of families and I remember thinking ‘this is not good’.”

Howard and Oliver shared their candid recollections at the Association of Superannuation Funds of Australia (ASFA) annual conference on the Gold Coast in November, while participating in a panel discussion titled ‘Insurance in super: restoring consumer and stakeholder confidence’.

Both executives are part of the Insurance in Superannuation Industry Working Group, which has pledged to create a compulsory code of conduct to lift standards in the sector by the end of 2017. That announcement was made in October, on the eve of the release of the latest slap down from the regulators.

Back in March, amid the media scandal, the Turnbull government had Investments Commission (ASIC) to launch yet another review into the life insurance industry, which it has since completed in collaboration with the Australian Prudential Regulation Authority (APRA). That report found that while 90 per cent of claims were paid out, there were pockets of the industry where denial rates were alarmingly high. One insurer, later revealed to be the Westpac Bank-owned BT Life, had denied one in three disability claims.

The group life insurance code will be based on the new life insurance code of practice, unveiled by the Financial Services Council (FSC) in October 2016, which covers life insurance sold outside of superannuation.

The FSC is the peak body for both the retail wealth management industry and the life insurance sector.

The working group, which includes representatives of all the major insurers and super funds, was formed with the backing of ASFA, the FSC and three other industry bodies: the Australian Institute of Superannuation Trustees, Industry Super Australia, and Industry Funds Forum.

To date the regulators’ investigations have focused on life insurance sold directly and through advisers, but their attention has now turned to the group policies sold in bulk as a default component of super.

All MySuper products, the basic type of super account that is eligible for default fund status, auto-enroll members into a group insurance policy that includes a combination of death, total permanent disability (TPD), and income protection cover.

In the financial year ended June 2015, $7.9 billion worth of premiums were collected from group insurance sold via super funds. That year the sector paid out $4.4 billion in successful claims.

ASIC and APRA have written to the trustees of every super fund in the country putting them on notice to lift their game on benefit design, policy maintenance, and claims handling.

Political pressure on the industry is only set to increase in the year ahead.

Nationals Senator John Williams has stated a Parliamentary Joint Committee inquiry into the life insurance sector will focus on the group policies sold via super funds, and flagged it may even consider whether life insurance should remain a default inclusion.

Nationals Senator John Williams has stated a Parliamentary Joint Committee inquiry into the life insurance sector will focus on the group policies sold via super funds, and flagged it may even consider whether life insurance should remain a default inclusion.

Former Labor MP and Shadow Minister for Financial Services Bernie Rippoll, who has been helping to facilitate the Insurance in Superannuation Industry Working Group, says it is wrong to characterise the self-regulation initiative as a kneejerk reaction to mounting pressure from government.

“Since 2013 there has been a lot of focus on how to improve group life insurance. The sector has acknowledged there are issues and the working group is trying to find the best way to work through those and collectively lift standards,” Rippoll told Investment Magazine.

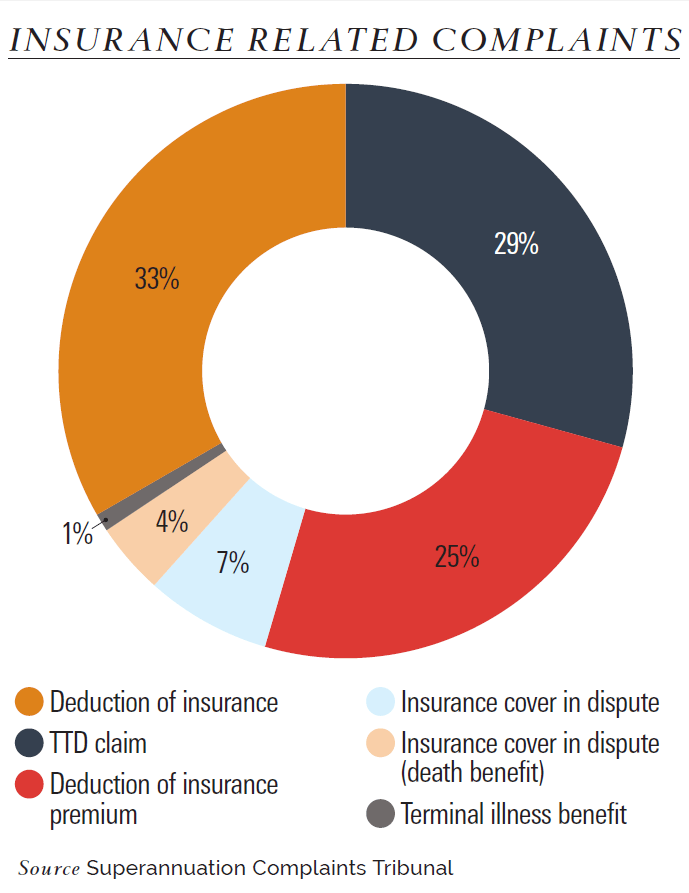

More than one third of all complaints lodged with the Superannuation Complaints Tribunal (SCT) in the 2016 financial year related to insurance, up from 20 per cent five years earlier.

Trustees need to question whether their policy could be structured differently to better meet the needs of their member cohort, SCT chairperson Helen Davis says.

Aside from policy design, lengthy and unexpected delays often compound member dissatisfaction, she says.

Former ASFA chief executive Pauline Vamos says an increasing number of people are turning to lawyers to lodge insurance claims on their behalf, which risks making the sector more legalistic and driving up member fees.

Berrill & Watson Lawyers principal John Berrill says there are many reasons for this trend, not least the “staggering volume of documentation” claimants are required to provide.

“A lot of people are daunted by that, especially when they are dealing with health issues and all sort of other challenges that come at these times,” Berrill says.

He would like to see the introduction of standardised claim and medical examiner forms.

Another problem is that too many funds take a “tick box mentality” to dealing with claimants, he says.

“One fund has got a voicemail message saying someone will return your call in four days. Then if they return the call and you don’t answer it you’ve got to go through the whole process again,” Berrill says.

“This is the sort of stuff that drives people to look to lawyers to help advocate for them.”

Davis wants super funds to act with urgency to improve their insurance claims handling processes to help stem the rising tide of complaints.

“If the industry can reach a standard that’s terrific. But there is nothing that stops a fund from improving its own process today,” she says.

“And remember that just because someone may not qualify under the policy it doesn’t mean they are not unwell, it doesn’t mean they aren’t out of work and having a difficult time, so just bear that in mind.”

This article first appeared in the December print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.