Australia’s superannuation sector is braced for a fresh government inquiry into life insurance. Insiders fear the review will recommend scrapping default group insurance in super – the tap that pours $8 billion a year in premiums. The need for proactive steps is the talk of the industry.

Chair of the Parliamentary Joint Committee (PJC) inquiry into the life insurance industry, Liberal MP Steve Irons, has warned the industry may need to be “jolted” into action to improve standards.

Irons spoke to Investment Magazine about his plans to put the group insurance sector under the spotlight ahead of the inquiry convening in late February. He says both the government and industry need to do better and promises the PJC inquiry will “push both in the right direction”.

The PJC will examine a range of issues related to group insurance in super, including: the value and effectiveness of group insurance products, the quality of service provided to members during a claims process, member education and understanding, and the unique needs of different age cohorts – particularly younger millennial generation members.

It is whispers of a potential push to dump universally mandated default group insurance via super, however, that is causing the most consternation.

There is no question that gutting mandated group insurance would rip a hole in the safety net that these default arrangements provide to millions of workers. There is also no question that many funds and their insurers need to provide better value and service to members.

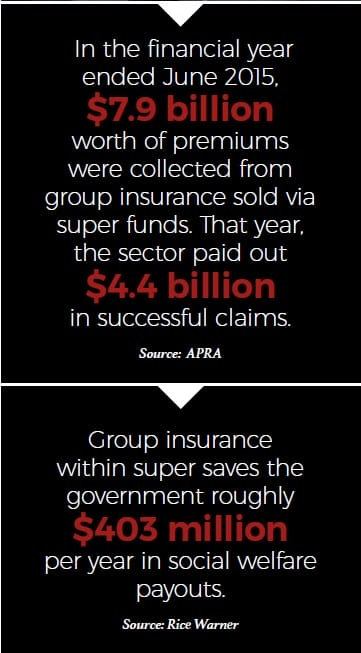

In the financial year ended June 2015, $7.9 billion worth of premiums were collected from group insurance sold via super funds. That year, the sector paid out $4.4 billion in successful claims.

BT general manager of superannuation Melinda Howes says default group insurance provides a valuable consumer protection and social good.

“The [government’s] decision to make the cover opt-out was designed to protect more Australians and ensure engagement from customers,” she says. “This is working.”

Warnings against ditching opt-out system

Warnings against ditching opt-out system

Under the current system, all members of MySuper funds – the low-cost, no-frills products that are eligible to be named in employment agreements as default super accounts – must automatically be signed up to group policies for death and total and permanent disability (TPD) cover.

Funds may augment this by also offering an additional policy for income protection on either an opt-in or opt-out basis. Most funds offer only death and TPD.

Members may opt-out of any or all of these policies, or choose to dial their level of coverage up or down. However, the vast majority of people make no change to the default cover their fund selects.

Dumping the opt-out mechanism for an opt-in system would be an “absolute disaster”, warns industry stalwart Jim Minto, who chairs the Insurance in Superannuation Industry Working Group.

The working group, formed in late 2016, has pledged to create a compulsory code of conduct to lift standards in the sector by the end of this year.

“If we did not have automatic life insurance, a huge percentage of the Australian population would have no insurance coverage,” says Minto, who is also director of Dai-ichi Life Asia Pacific. Eliminating mandated default group insurance inside super would leave millions of Australians with existing health conditions, or who work in hazardous environments, vulnerable, Minto says. It could also have big implications for Australia’s social welfare system.

Pressure on the public purse

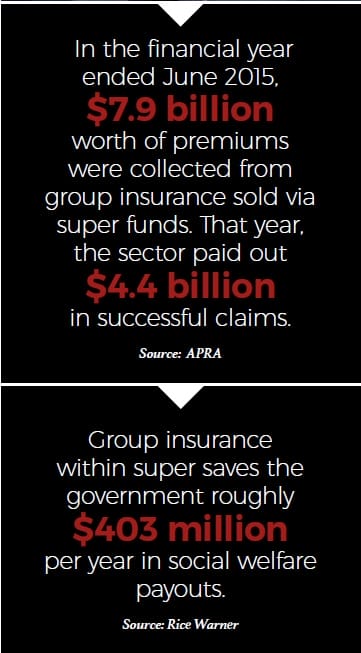

A 2014 report by actuarial and consulting firm Rice Warner found group insurance within super saved the federal government roughly $403 million a year in social welfare payouts.

Australian Institute of Superannuation Trustees (AIST) director Catherine Bolger, who is the peak body’s representative on the Insurance in Superannuation Industry Working Group, says scrapping default group insurance in super would put an unreasonable strain on the public purse.

“Australia already has a significant problem with under-insurance, so a move away from opt-out insurance in super would only exacerbate this,” Bolger says. “Members unable to work would draw on other forms of assistance, whether it be Medicare, the National Disability Insurance Scheme or Centrelink benefits and the like.”

Irons maintains that the PJC will look at all potential unintended consequences that any changes to the existing system would have on members, the industry and taxpayers.

Little value for younger members

One of the easiest targets for critics of default group insurance is the relatively poor value it provides to younger super fund members, particularly those aged under 25.

Research firm SuperRatings finds that the average 35-year-old male in a whitecollar occupation has an account balance of $58,550 and pays $226 a year in group insurance premiums. Meanwhile, the average 25-year-old male in a white-collar occupation has a balance of less than $4000, but he is still paying almost as much, $203 a year, in group insurance premiums.

AIA Australia chief executive Damien Mu, who is also co-chair of the Financial Services Council (FSC) life insurance committee, and another member of the Insurance in Superannuation Industry Working Group, says the sector must deal with this challenge in a more sophisticated way.

“Cover is essential at all ages, but the question that needs to be better addressed is exactly what type of cover and how much of it,” Mu says.

While he opposes scrapping default death cover for young people altogether, he does concede it often needs to be dialled down and that more focus should be placed on ensuring these members have adequate income-protection in case they are injured and can’t work for an extended period.

“For most young people, their ability to earn an income is their most important asset and protecting that is very important, particularly because they haven’t typically built a level of debt that would justify a large TPD payout.”

SuperRatings general manager of research, Kirby Rappell, says the good news is that there are signs the industry is already moving in the right direction.

“Some funds are reducing default cover for young members who are not expected to have material financial commitments but increasing this when people are in their 30s and 40s, when they are more likely to have a mortgage and dependents,” Rappell says.

Efforts to keep the government out of it

Still, the industry continues to cop criticism, with consumer watchdog Choice taking aim.

“There is a worrying lack of transparency around default life insurance policies,” Choice head of campaigns and policy Erin Turner says.

Irons says this is something the PJC intends to address.

“Understanding, transparency and clarity of the premium,” he says. “That’s where, hopefully, the inquiry and the insurance industry itself will head.”

Mu agrees the industry has room for improvement when it comes to communicating with members.

“Now is the time to improve engagement and confidence in the industry,” he says.

Minto also called on his peers to take voluntary action to improve standards in a bid to ward off unwanted government intervention.

Irons indicated he maintains an open mind about what the industry can achieve on its own.

“There is an opportunity for the industry to lead the reform, instead of being regulated into” it, Irons says. “Insurers and superannuation funds have the capacity to reform, but they may need to be jolted into that.”

This article first appeared in the March print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.