A student project to improve the richness of information in retirement estimates provided under ASIC’s class order relief inadvertently highlighted the many challenges faced by industry, policymakers, and regulators as they seek to make quality guidance accessible to the broad population. The trade-off between tailoring information to be more relevant for people pulls against the desire for such information to be accessible at low cost.

The Sandbox Program

The aim of the UNSW Sandbox Program* is to introduce students to industry projects. Industry partners develop project tasks which reflect contemporary challenges and then engage with student project groups through the term. Adopted across various courses at UNSW, last term it was incorporated into the popular subject ‘Retirement Saving and Spending over the Lifecycle’ taught by Dr Kevin Liu, a foundational subject for those interested in Australia’s retirement system.

The Conexus Institute collaborated with Super Consumers Australia – Xavier O’Halloran and Matthias Oldham – and Estelle Liu from Aware Super. The assigned project focused on extending guidance around retirement estimated provided to fund members.

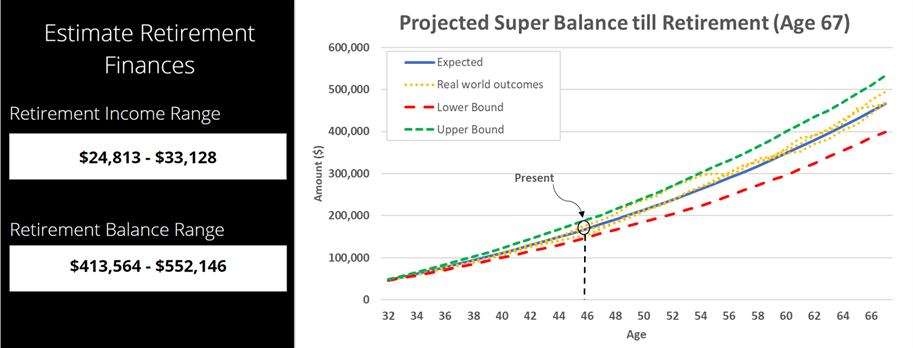

The group awarded top mark was Nafiz Khan, Andy Nguyen (pictured, insert), Ainkaran Sritharan, James To (main picture), Calvin Tran-Huynh. This group considered it important to show how retirement balance grows over time and to then use this as a frame for presenting both lower and higher outcomes. Presenting retirement income and retirement balance in proximity enabled the two pieces of information to be better connected.

The group awarded top mark was Nafiz Khan, Andy Nguyen (pictured, insert), Ainkaran Sritharan, James To (main picture), Calvin Tran-Huynh. This group considered it important to show how retirement balance grows over time and to then use this as a frame for presenting both lower and higher outcomes. Presenting retirement income and retirement balance in proximity enabled the two pieces of information to be better connected.

Retirement estimates a test case for scalable guidance

To a degree, retirement estimates are a test case for the area of scaled advice. Class order relief provides a ‘safe harbor’ for super funds to provide some basic guidance to their members. In this context the concerns and frustrations raised by a large group of students are insightful. These fall broadly into three categories, outlined below:

1. Calculation

- Concerns around the calculation itself, particularly the assumption that age pension payments will be constant for life, when for many people it will increase as their balance falls.

- The assumption that people will live to 92 concerned some students (as roughly about 50 per cent of people will live for longer).

2. Personalisation (individual and product characteristics)

- Students flagged significant concerns relating to the accuracy of the calculation given characteristics of individuals and their household situation. The class order contains many assumptions relating to an individual’s household situation (for instance they are assumed to have a partner with the same super balance, own their house and have no other assets).

- Similarly, the class order does not allow for funds to incorporate product characteristics. Under the class order, returns are a constant 3 per cent real regardless of which options members have their accounts invested. It also fails to account for product features such as lifecycle strategies.

3. Next steps / call to action

- Students constantly wanted to enable consumers to interact with their projections. This is not permitted in the way the class order is applied.

- Students had concerns that the information provided was insufficient as a basis for making decisions around issues such as additional contributions.

- If members seek guidance from a more detailed source (e.g. ASIC MoneySmart) they are likely to receive a different forecast as it incorporates personal information and product features – so the transition is not simple and potentially confusing.

In a microcosm this case study draws out many of the major challenges facing the provision of quality, scalable guidance. Personalising to individual and product characteristics makes the information far more relevant but potentially represents personal advice which requires an assessment of the best interests of the person receiving it, increasing the cost. Providing pre-approved safe harbor style tools and calculations will reduce cost but are necessarily limited in how they can be used to protect consumers from advice that is not in their best interests.

Unfortunately, there continue to be many examples within the super industry of financial advice that is not in the best interests of members. For example, ASIC’s 2019 report into advice provided by super funds found 51% of the advice provided was in breach of the law and 15 per cent of the files analysed would have seen the person suffer financial or non-financial loss had they followed the advice.

This project highlighted many of the challenges industry, policymakers and regulators will need to grapple with if we are to get more high quality, affordable guidance and advice that can be used by people.

* For background: ASIC Class Order [CO 11/1227] provides prescriptive formulae and disclosure rules for the provision of deterministic estimates of projected accumulation balance at retirement and annual income in retirement. According to SuperRatings, 42 per cent of super funds now provide retirement estimates in annual reports. We are unaware of any fund which steps outside the class order relief. The student challenge was to take the existing ASIC class order relief on superannuation projections and create a hypothetical stochastic version to illustrate the range of outcomes that consumers may experience. While part of the assignment relates to calculations, arguable a greater challenge is how to communicate and frame the information.

Leave a Comment

You must be logged in to post a comment.