Super funds are required to develop retirement income strategies that deliver income over a retirement that may span decades. Waiting to see what happens is not going to work as an assessment technique. So how might you establish if a solution is any good?

Our original work, “Assessing retirement income strategies… when outcomes are but a promise”, suggests assessing the retirement income strategies of super funds by combining a checklist and quantitative modelling. The checklist would aim to gauge whether fund trustees are doing everything required to deliver good outcomes to retired members.

Quantitative modelling can assist in evaluating retirement ‘solutions’ – the mechanism by which a retiree’s assets are allocated to investments or products and then drawn on to generate income.

We’ve just released the companion research piece titled “How to approach quantitative assessment of retirement income strategies”, written with the assistance of modelling expert Gaurav Khemka from the ANU. It sets out a framework for how quant modelling could be done, while not prescribing a single approach. This paper is written for funds, asset consultants, research houses, regulators and potentially financial planners – indeed, anyone interested in better understanding the outcomes that a retirement solution might deliver.

Read Part I of this series: Significant challenges in assessing retirement income strategies

The ultimate aim is to assess the extent to which a retirement solution meets the objectives it sets out to achieve. The Retirement Income Covenant (RIC) mentions three (broad but not specific) objectives – maximising expected income, managing the risks to income, and providing flexible access to funds. Any modelling exercise should speak to all three objectives.

This gives rise to two implications. First, a stochastic model is essential to capture income risk. Second, although generating income may be the primary goal, the accessible balance across the entire strategy matters as a gauge of flexible access to funds.

Our modelling and assessment process has a relatively straightforward structure, although it requires technical skills to implement and inevitably requires making many assumptions. There are three parts:

1. Simulate a series of ‘outcome paths’ that a solution might deliver – This scopes out the shape and range that income and the balance might trace out over the course of retirement.

2. Summarise the outcomes through selected measures or ‘metrics’ – We suggest three presentations:

a) Table of metrics – these would be tailored to show the measures of most interest given the objectives.

b) Charts – we think the combination of an income layer and income percentile charts tell a good story.

c) Summary scorecard – to convey the extent to which each of the three RIC objectives is met.

3. Assessment by comparison – We recommend using a default solution that the ‘typical’ member might follow as a baseline benchmark. Any solution should improve on the default, while revealing no elements suggesting that it unsuitable for purpose. Comparisons might also be made between candidate solutions to inform solution selection and assist funds in solution design and development.

One complication is that there exists different types of income objectives. (It emerged during industry engagement that funds are working to different objectives). Different objectives imply delivering different income patterns and require different metrics to evaluate success and failure.

This is a central issue in implementing the RIC, which we highlight by referring to two income objectives in our case studies – an ‘income optimisation’ and an ‘income target’ objective.

We present here a simplified case study for a single male with a $400k retirement balance that is focused on income optimisation. This objective presumes that the retiree wants to extract as much income as they can from their savings while managing income risk. Our aim is to illustrate the assessment process, rather than recommend a solution. We note that assumptions are crucial, particularly around investment returns and product features.

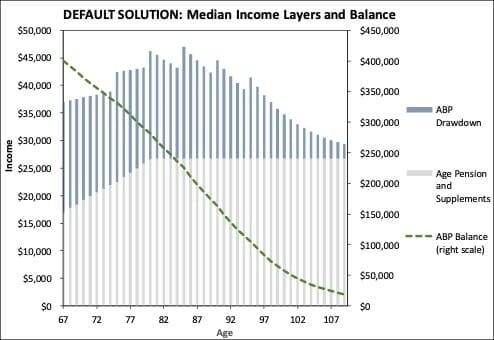

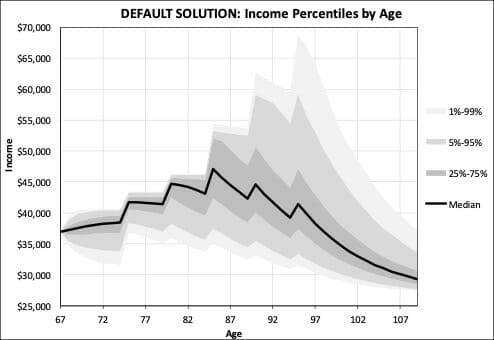

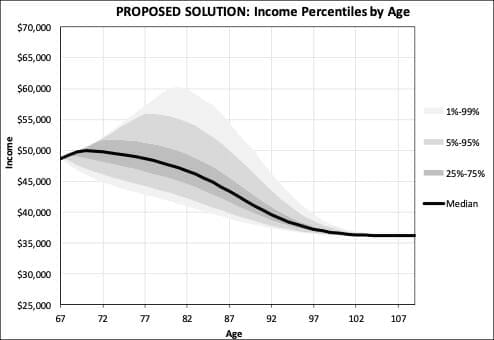

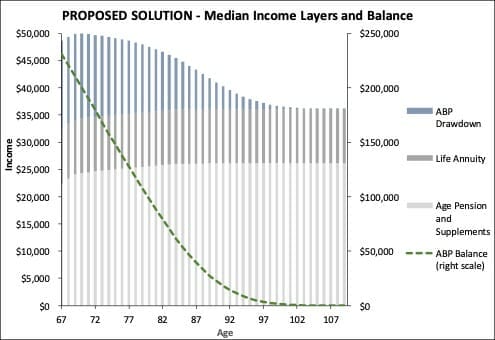

Charts 1 and 2 are for a default solution that invests only in an ABP while following the minimum drawdown rules. Charts 3 and 4 are for a proposed solution that invests in an inflation-adjusted life annuity, and the remainder in an ABP where an ‘affordable’ drawdown is taken that varies with age and balance.

The income layer charts at the top show median income and its sources, and the trajectory of the ABP balance. The percentile charts at the bottom convey the range of income, and speak to income risk by revealing the likelihood of lower income and how far income might decline.

The charts reveal that the proposed solution generates moderate income that trends down from about $48,000 to around $36,000, with some chance of income over $50,000 up to about age 90. However, it delivers income that is generally higher, more stable and has less downside than the default solution. Meanwhile, the proposed solution runs down the ABP balance quicker and so offers lower flexible access to funds; but nevertheless sustains a meaningful median ABP sustained into the 90s.

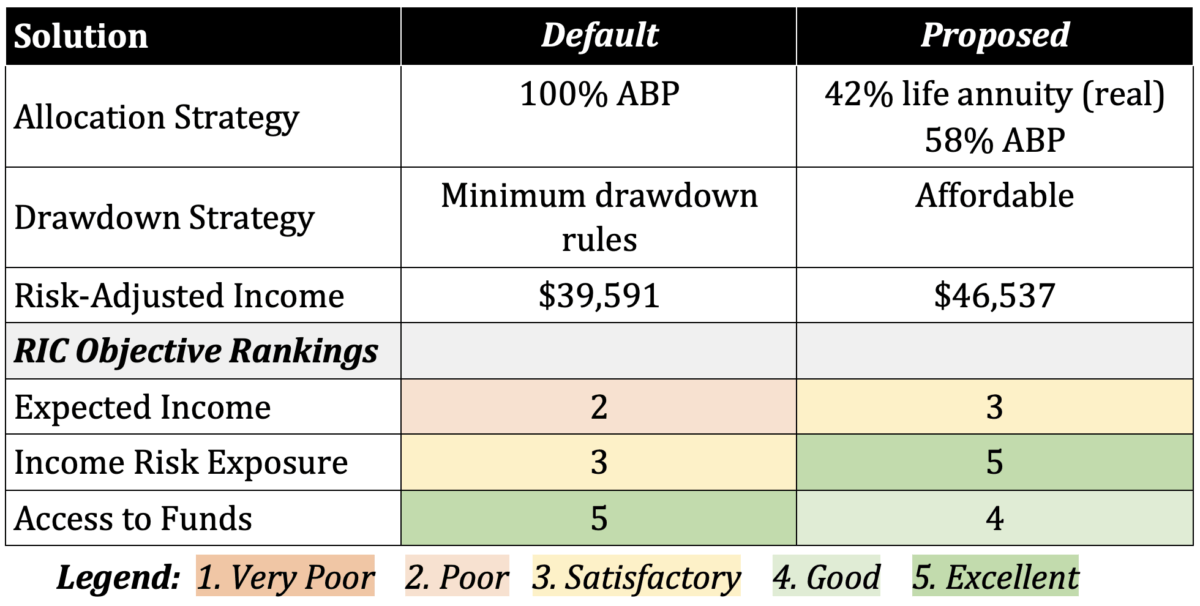

Below is our summary scorecard for the two solutions. We report an overall score called ‘risk-adjusted income’ (which is utility-based), and attach rankings on the three RIC objectives. The rankings are subjective, but informed by the modelling. The proposed solution improves on the default on balance, taking into account that it does worse on flexible access to funds but not in a critical way.

Summary scorecard

Our presentation of the model outputs is just one way of summarising, and should be taken as an illustration and not a recommendation of how it should be done. Nevertheless, the simple examples presented should suffice to show how quant modelling makes it possible to better understand and hence assess what a retirement solution might deliver.

We are grateful for the significant feedback received during the research process. It helped reinforce the importance of assumptions, and the need for robust solutions that account for alternative assumptions. Scenario analysis or stress testing were other valuable suggestions, although these methods risk drawing too much attention to a few out of many potential future paths.

Everyone involved in the design and assessment of retirement solutions should have a quantitative model in their toolkit. It is only through undertaking such modelling that retirement solutions can be connected to the outcomes that matter most to retired members – the income that they could receive.

Geoff Warren is an associate professor at ANU and research director at The Conexus Institute

David Bell is executive director at The Conexus Institute

Leave a Comment

You must be logged in to post a comment.