As one of the rare public-offer industry super funds with a considerable defined benefit (DB) component, Aware Super is keen to apply its investment and liabilities management skills to defined contribution (DC) assets in a post-Retirement Income Covenant world.

During a media event hosted by Challenger, Aware Super portfolio manager of retirement strategy Shang Wu said even in the DC world, funds are exploring what their retirement solutions are going to look like for members.

“That’s also shaping the liability of the defined contribution members, because your retirement solution is going to decide how their income profiles are going to look like in retirement,” Wu said.

“It’s the same skill [between DB and DC] that you understand the liability, you understand how the asset will support liability, and how these two come together that will give you the better outcome for your superannuation members.”

Aware Super services approximately $1 billion in DB assets and more than 5000 members as a result of the Health Super merger in 2011. And according to APRA fund-level data as at the end of FY23, it has the third-largest DB assets among industry funds after UniSuper and Vision Super.

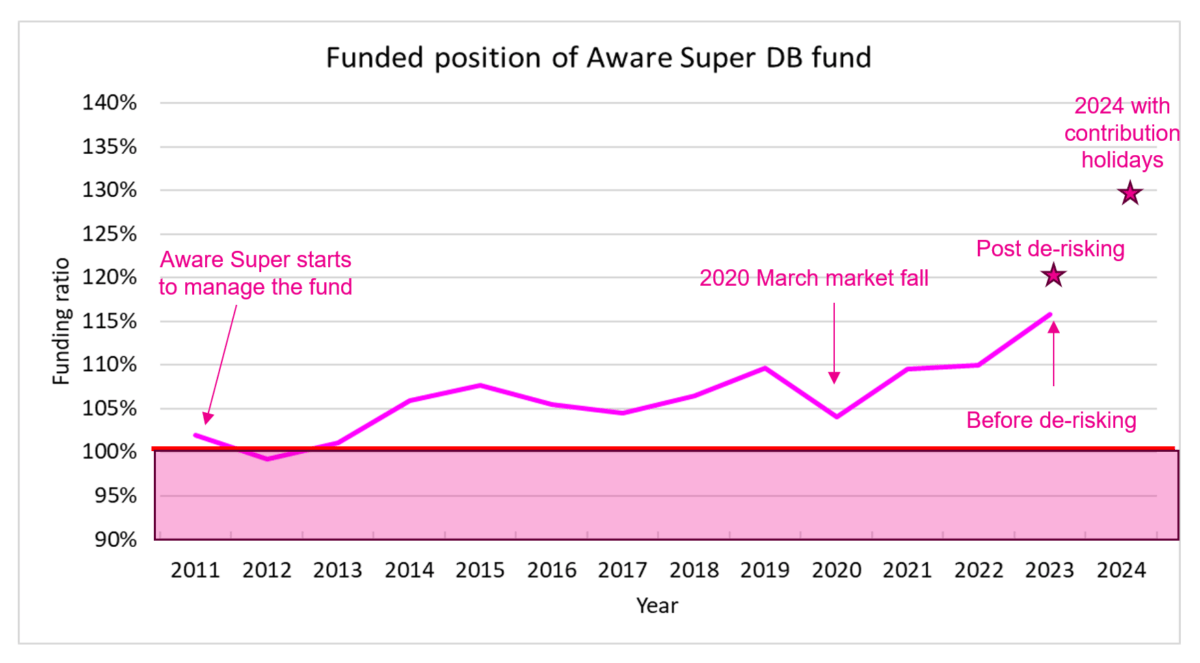

When an Aware Super DB member retires, they can either choose a lump sum or a lifetime pension, and more than 3000 members have chosen the latter option. For these members, the fund selected Challenger in 2023 to provide a group lifetime annuity policy to the value of $619 million, in a bid to de-risk the liabilities from investment, inflation and longevity risks.

But before this decision to de-risk, Wu said Aware Super needed to know exactly when it could afford to do so. The fact that the majority of DB fund members are retirees complicates things, because it means employer contributions are a very small part of the funding source.

Difficult situation

This poses a triple threat to the fund – for one, if it now needs to ask employers to adjust their contributions, the change is likely to be drastic.

“If the funding position – measured by the technical measure called vested benefit index, or VBI – if that index dropped by 0.3 per cent from 100 to 99.7 [per cent] we estimate that our employers have to double their annual contribution, which will be big burden for their corporate finance,” Wu said.

It will also be a difficult conversation to have with employers since the last time these retired members worked for them could be 20 years ago, Wu said.

“There are also deferred members [still in the fund] who are not working for the employer anymore,” he said. “You’re asking them to pay money for someone that has very low relevance to them.”

And thirdly, the sheer number of employers makes it operationally difficult for the trustees to negotiate with every single one of them.

“Even they agree to do that [extra contribution], it’s a painful process you have to go through because there are hundreds of employers there,” Wu said.

“It just becomes a very, very bad event for the trustee in that situation.”

When Aware started to manage the Health Super DB fund in 2011, the funding position was 101.9 per cent and Wu admitted the team was “nervous” when it dropped below 100 per cent in the following two years due to market volatility. But fortunately, the position recovered and reached a desirable 116 per cent funding level in 2023, which has given the fund confidence to explore de-risking options.

Apart from being used to build DC retirement income solutions, a DB capability could also prove useful in merger negotiations. Mercer partner of investment and retirement Richard Boyfield said most DB funds seeking merger partners might be hesitant to choose someone without their own DB system because of the complexities it might add.

“[DB and non-DB funds merging] isn’t impossible. It has happened over the last couple of years, but it does mean that you need really got to consider that risk management,” he said.

“Regulators in Australia, compared to the UK, [are] far less involved in monitoring and the requirements that they have on defined benefits schemes.

“So, you’re in this situation where, as a trustee, [you need to think] is this where we can excel, and where we can do well? If you’ve not got any experience in that [DB] area, then it becomes a challenge.”

Leave a Comment

You must be logged in to post a comment.