Retirement represents a “key commercial thematic” for both profit-to-member and retail funds over the next 10 years, according to The Conexus Institute’s* upcoming 2025 State of Super report, and high-quality member services and adviser relationships will determine who comes out on top.

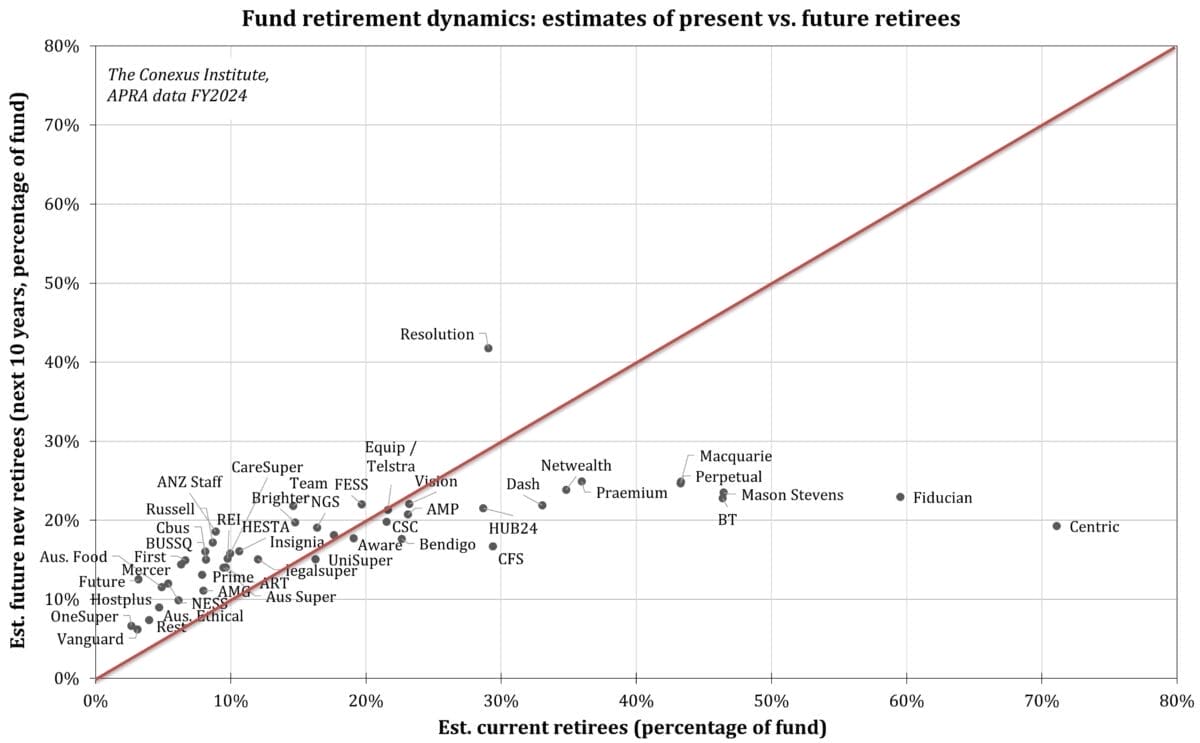

Funds like Cbus, Brighter Super and HESTA will see a silver tsunami of retirees over the next 10 years that exceeds their existing retired membership, while the likes of CFS, Netwealth and BT need new members to “offset their aging member profiles”.

“Those platforms that service retirees are in natural outflow; it’s their job to pay out pensions,” David Bell, executive director of The Conexus Institute, tells Investment Magazine. “For them, it’s imperative that they find new clients, and financial advisers are the conduit for that.”

“And then on the other hand you’ve got not-for-profit funds with members approaching retirement with bigger and bigger balances and expecting higher and higher service levels. And that’s where they’re getting picked off.”

So profit-to-member funds have “two commercial incentives” to improve their retirement offerings, the report says: to deter members from seeking external financial advice; and to attract or retain members. They can do that by making sure their services are “sufficiently personalised” and that their retirement offering is attractive to financial advisers.

“But with the platforms, their mission statement is often to increase the efficiency of the adviser, and allow them to add more clients,” Bell says.

“That’s a lot of supply potential, and if platforms are achieving that efficiency that allows the advisers to pick off more (industry fund members). You’ve got this supply and demand, defence and offence piece.”

While the natural demographic trends might be working against platforms, profit-to-member funds still need to scrutinise their own service offering and the gaps in their strategy if they want to hold on to high-value members wondering what to do with their million-dollar balances.

“Funds need to have a really good handle on their own wealth trajectory – cohorts within their membership,” Bell says.

“They should be able to see their vulnerabilities when it comes to retaining members – and I’m only talking about through the commercial lens. They’ve also got to think as fiduciaries and consider how they can do the best they can for these members. But they’ve also got to think about, commercially, if they uplift their services, how that will impact retention across these different cohorts. And they still might find that their top member cohort (by accumulated balance) goes to advice.”

To prevent that, profit-to-member funds are also trying to reduce frictions between accumulation and retirement. AustralianSuper has floated the creation of an “account for life” that would, according to the fund, “ease the transition between the ‘saving’ and ‘spending’ phases” by allowing members to receive income from and contribute to the same account.

“You’re seeing that push from a number of bigger funds with lower-balance members that want some of the heavy lifting to be done by product design; call it a soft default or a default with an opt-out,” Bell says.

“If it’s well-designed, the first offer can really help people that don’t know where to start, and be an anchor point for people to consider options around.”

The new class of adviser (NCA) – left out of the latest round of draft legislation for the Delivering Better Financial Outcomes bill – would have gone a long way to helping profit-to-member funds improve their service offering and retain their members in retirement, Bell says.

“Digital is scalable, but we know people take value from human input. The NCA accompanied by a digital tool is where it was going to go for super funds and enable them to, from a fiduciary standpoint, engage with their members and help them into something semi-tailored. From a competitive perspective, it would have felt more personalised and created higher retention rates. I imagine a lot of funds would have been disappointed NCA wasn’t in there.”

To receive a copy of the full State of Super 2025 report, subscribe to The Conexus Institute’s Independent Perspectives newsletter here.

*The Conexus Institute is a not-for-profit think-tank philanthropically funded by Conexus Financial, publisher of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.