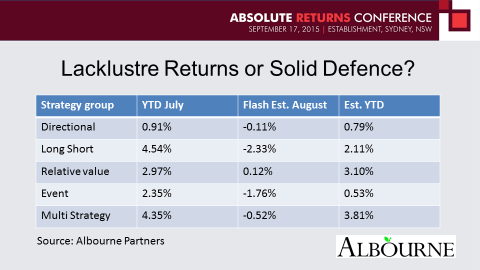

A combination of lacklustre performance, a growth in co-investments and liquid alternatives, are putting downward pressure on hedge fund fees, delegates heard at the 9th annual Absolute Returns Conference in Sydney.

Richard Johnston, managing partner at Albourne, said the move was being accompanied by a greater questioning of the talent that investors were paying for.

He also told how lower fees were also being offered in exchange for longer lockups.

Johnston said he has seen a few managers now adopt a partnership culture with the investor, giving the example of an account that offers access to modular strategies, that were often components of the managers main fund.

Travis Schoenleber, managing director at Cambridge Associates, predicted fees would also be hit by a growing saturation of the US hedge fund market with lower alpha generation and growing capacity constraints, making the bulk of the market less compelling. However, he saw promise in Asia, where he saw markets becoming more open, regulated and liquid.

“You have credit markets that are deepening, you have greater ability to short and you continue to have structural inefficiencies that skilled managers can exploit with far less competition than we see in the US,” he said.

Schoenleber added low-cost hedge fund substitutes like liquid alternatives would also continue to put pressure on fees.

Schoenleber added low-cost hedge fund substitutes like liquid alternatives would also continue to put pressure on fees.

“Where liquid alternatives get interesting is when they have a strategy in place that can chip away at the big difference you have between fee structures and net and gross fees. Where you don’t necessarily want a liquid alternative is where you have something that is kind of approaching a limited net return.

“But there is a big gap there for people who can do it really well.”

Sabrina Callin, managing director at PIMCO, said the increasing array of alternative and asset returns strategies meant diversification could be accessed relatively cheaply.

She saw the three reasons for the increased investor interest in liquid alternatives: as the need for alternative sources of returns, particularly as the traditional 60/40 portfolio split was unlikely to see the historic levels of double-digit returns again; diversification; and a reduction in downside risks.

Leave a Comment

You must be logged in to post a comment.