Investment structures that could open up the affordable housing market to institutional investors have been submitted to the federal government’s Affordable Housing Working Group by three super funds and Industry Super Australia (ISA).

Cbus and ISA favour debt financing in the form of a bond aggregator model (BAM). As an alternative, ISA has also put forward an equity financing option in the form of a “densify recycling model” (DRuM).

Meanwhile, First State Super sees a role for a new “innovative” clearinghouse and Christian Super has suggested a “path to ownership” model that attempts to address the structure of the underlying investment and social program.

In addition to these, the government received a further 73 submissions from organisations and individuals including the ACT government, the Centre for Urban Research RMIT, Impact Investing Australia, National Australia Bank and the Westpac Group.

Debt financing using a bond aggregator model (BAM)

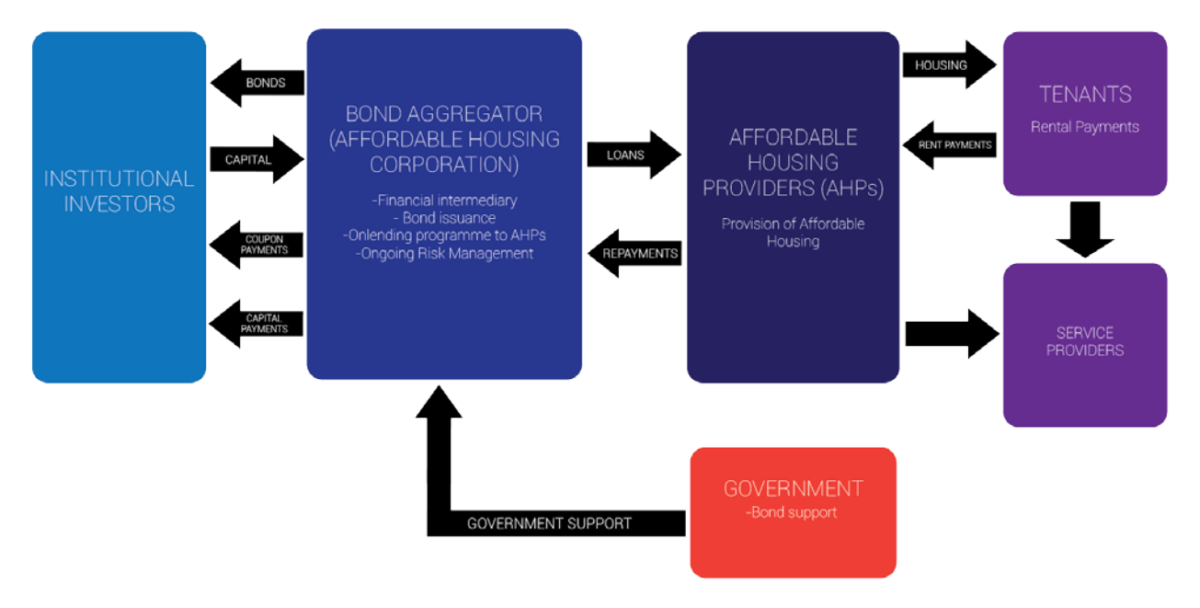

To make a bond aggregator model feasible, ISA envisages the establishment of an affordable housing corporation (AHC) that would interface between institutional investors and housing providers, similar to the UK Housing Finance Corporation.

The AHC would act in a similar way to a Treasury Corporation and would be responsible for:

- Performing credit assessments of approved housing providers (community housing providers, cooperatives, private sector etc)

- Aggregating approved credit for affordable housing providers into bond packages

- Issuing bonds of varying maturities to institutional investors

- Collecting repayments and paying coupons to institutional investors.

“Basically, we would have a very large-scale intermediary that issues bonds and then uses the money from the bonds to finance affordable housing providers. You would [also] need a very strong regulatory environment that sits around that. This would mean the cost of financing for affordable housing providers would come down significantly,” said Brett Chatfield, investment manager of public markets at Cbus.

In Australia, most housing associations have bank financing at three to five years and as a result are constantly refinancing, which can make pricing unattractive.

Chatfield said Cbus has been examining affordable housing from a debt financing perspective. In its thinking, there should be a role for long-term debt in affordable housing, where the super fund has the ability to take a long-term view compared to the banks but also earn an appropriate return.

He added the economics become a lot better for the overall structure if longer term and lower cost financing can be delivered to the providers.

“[However], one of the key issues for institutional investors in this space is that you need to move from a non-commercial to a commercial return. This [bond aggregator model] is one mechanism, but it needs to be supported by some degree of government support and also potential land grants, from state governments through to the housing associations.”

Echoing this in its submission, ISA said to alleviate institutional investor concerns regarding the underlying counterparty risk and the return premium that would be attached to this, the government would need to provide some degree of support to this structure.

Chatfield added to this, saying Cbus’ submission had left the form of support reasonably open because, depending on its nature, it would have different impacts on the government’s balance sheet.

“It certainly makes sense to have some degree of government support, at least in the initial stages as you build up scale and credibility of the market,” he said.

(Continued below)

[tv playlist=’55c989c3150ba0fb768b458c’ theme=’im_article’]

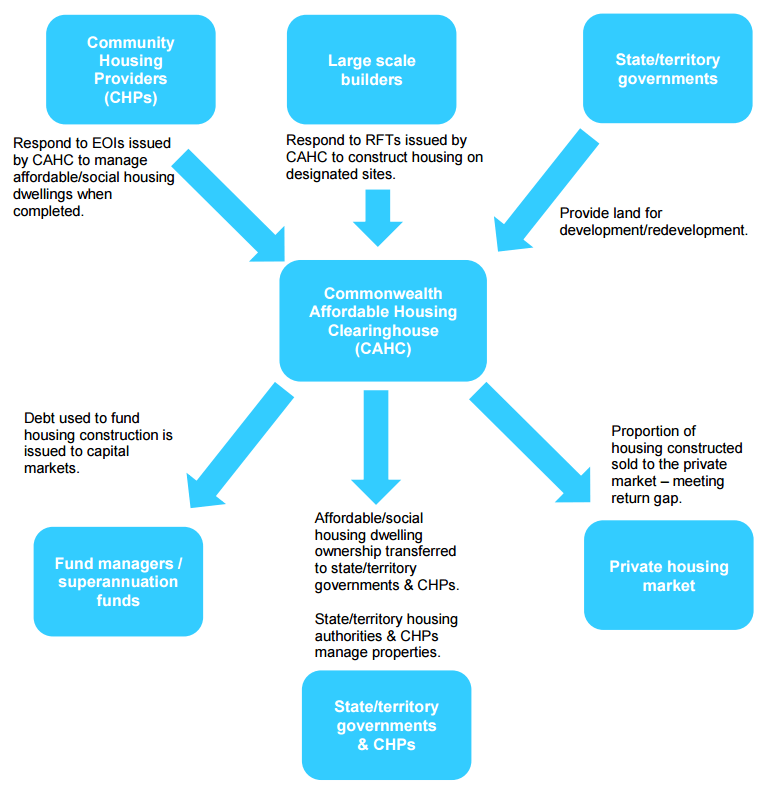

A new clearinghouse

Through this process, Cbus has been working with First State Super, who also has an interest in this space and favours bonds.

First State Super in its submission (which was put together with policy think tank Per Capita and the Financial Services Knowledge Hub) argues while housing loans and bond aggregators rely on government funding subsidies or guarantees, its proposed model leverages existing state and territory government land to fund the construction of new affordable and social housing dwellings.

According to the $52 billion fund, in order for an affordable financing model to succeed it must solve three fundamental challenges simultaneously. These challenges are that:

- Governments need to be willing to provide increased funding, guarantees, or land/stock transfer

- The community housing sector needs to be credible at managing and increasing affordable and social housing stock at a very large scale

- Capital markets need to be unlocked through appropriate risk-adjusted returns.

First Sate Super believes the establishment of a new clearinghouse would solve all three challenges, “unlocking capital markets and facilitating significant investment in the development of affordable and social housing in Australia”.

It suggest the Commonwealth Affordable Housing Clearinghouse (CAHC) would partner with state and territory governments, community housing providers and builders to generate housing construction projects which will produce affordable housing stock.

“State and territory governments (as well as potentially the Commonwealth) would provide government-owned land for development (in the case of greenfield sites) or redevelopment (in the case of brownfield sites),” the submission says.

“The CAHC, in partnership with the relevant state or territory government, would issue tenders to leading residential building companies for the construction of private, affordable and social housing dwellings.”

It would also facilitate the issuance of project debt, and following the development of affordable housing stock it would transfer it to appropriate community housing providers and state or territory housing authorities, potentially in the form of a long-term lease.

Path to ownership model

Christian Super tackles the issue from a different angle, suggesting that solely increasing the availability of affordable housing will likely be ineffective at addressing social issues unless there is a path to broader home ownership.

“Simply increasing cheap rental supply may perpetuate subsidy-dependency by the renters, reduce supply in the owner-occupied market (by making it attractive for investors to buy existing housing) and create a long-term cost to government,” their submission says.

As such, the super fund recommends a path to ownership model that would see the occupier build up equity in the property over a 10-year period by sharing in the capital gain of the property with the government. This would allow the occupier to comfortably afford a mortgage after this time and buy the property.

The government’s share of the capital gain would be on a sliding scale depending on the progress the occupier made towards saving for a deposit, with the help of the institutional investor.

To attract investment, the government would provide institutional investors with a tax offset of 3 to 5 per cent per annum of the purchase price of the dwelling.

Other benefits for the institutional investors include:

- Rental income from the occupier (80 per cent of the prevailing rents)

- Transition to ownership incentive payments from the government

- Availability payments from the government to mitigate occupancy risk

- Capital loss protection from the government.

Densify recycling model (DRuM)

Like Christian Super, ISA has also examined how equity financing could be used in the space. The proposed DRuM would potentially create a pipeline of mixed housing developments and would focus on increasing returns by “densifying” existing development and then recycling the proceeds.

In ISA’s assessment, this would require relatively less fiscal outlay by government, deliver social and affordable housing to the community and provide acceptable investment returns to members.

ISA chief executive David Whiteley says: “We believe that with the right policy settings to tap into our growing retirement savings pool, those outcomes [of boosting the supply of affordable housing and providing greater retirement security] can be achieved in a market-based way that also provides secure, long-term outcomes for investors.”

Leave a Comment

You must be logged in to post a comment.