Local Government Super (LGS) has launched its first annuity product to complement its account-based pensions, as a strategy to defend against longevity risk.

LGS is still of the view that allocated pensions are a very effective way of providing retirement income for members, however, one of the weaknesses is that income may run out because of the uncertain nature of the returns and longevity risk, said Peter Lambert, chief executive of the $9 billion super fund.

“Given that, it is appropriate to have something that provides longevity risk protection for members who are interested in that and have sufficient assets to make that worthwhile,” Lambert said.

“Clearly for many people, the longevity risk protection is going to be the age pension, but for those that wish to have something over and above the old age pension when they get to their 80s and beyond, that’s really where the annuities are an ideal solution.”

He added his own preference would be for members to consider deferred annuities, but that the super fund could not offer them until the government changed the rules surrounding them.

“A deferred annuity is probably a more relevant product than a lifetime annuity,” he said.

This newly launched annuity has been white labelled, so that it can be offered to members and embedded alongside other products. This is part of a ‘layering’ income approach advocated by Challenger, who are backing the product.

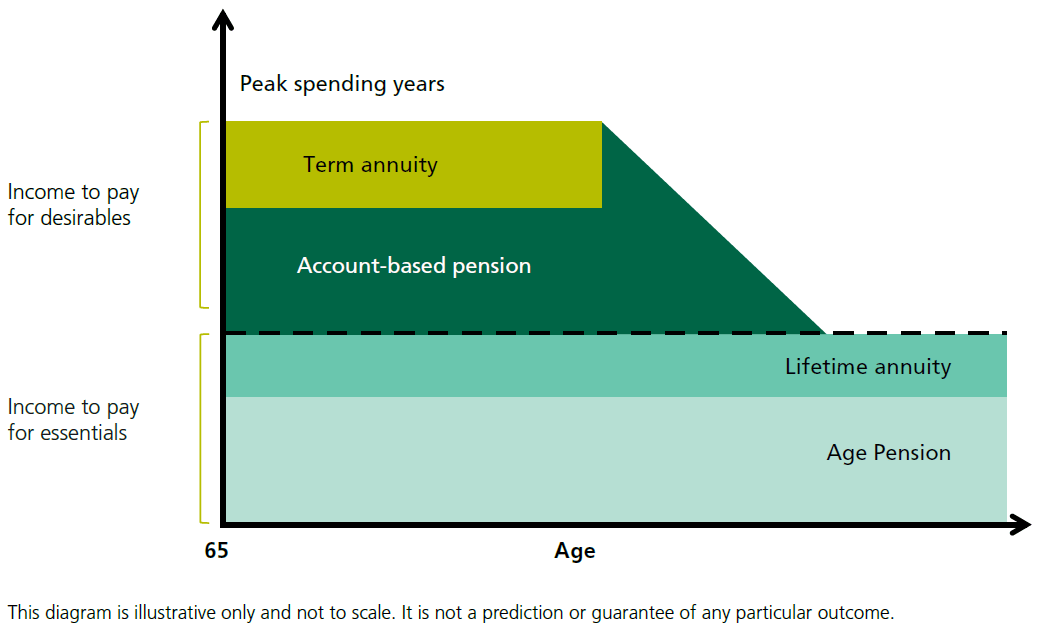

Layering works by having multiple sources from which members can draw an income (see fig 1, click to enlarge).

For this to work effectively, advice to members is crucial.

“We think it’s essential that anyone buying an annuity knows the benefits and pitfalls in them, and it won’t be for a majority of people, but there will be a section of our membership it will resonate with,” Lambert said.

“For someone that has received sufficient assets to provide them with lifestyle needs well into their 80s, an annuity does give them that protection of guaranteed income over and above the age pension, primarily to ensure that they are able to meet medical bills at that age.”

He added while this annuity was a step in the direction of providing income in retirement, he fully expected there to be other products that will be attractive and added to options available to members.

LGS has more than 90,000 current and former government employees as members; with a significant portion due to move into the 65-plus age bracket over the next ten years.

Leave a Comment

You must be logged in to post a comment.