Such is the impact of market conditions to the equity markets over the medium term, they have lost their mantle as the “primary growth producing asset class.”

“It was going to be tough enough for equity markets going forward anyway but with Brexit … it has probably increased the tail risk of an accident in equity markets. If the European Union does ultimately crumble, it is likely to create a global recession,” says John Eliopoulos, investment manager at Telstra Super.

“That’s not our core scenario, but we can’t ignore it either and we have to build it into our expected returns when we are looking at growth assets and risk assets like equities.”

Richard Brandweiner, chief investment officer of First State Super, sees equities as retaining an important structural role of helping to combat against inflation and provide growth. However, he too is conscious of their changing role.

“It can’t be a blind allocation, because price risk can undermine those returns unless it is actively managed,” Brandweiner says.

Change in strategy

Change in strategy

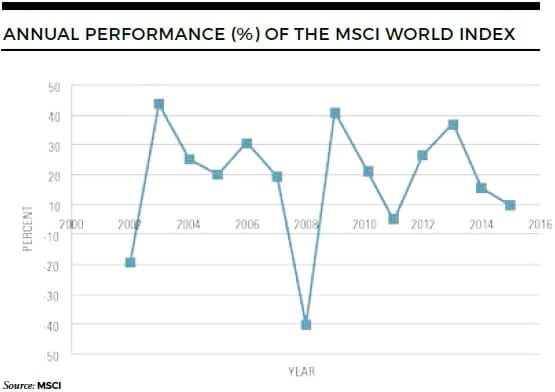

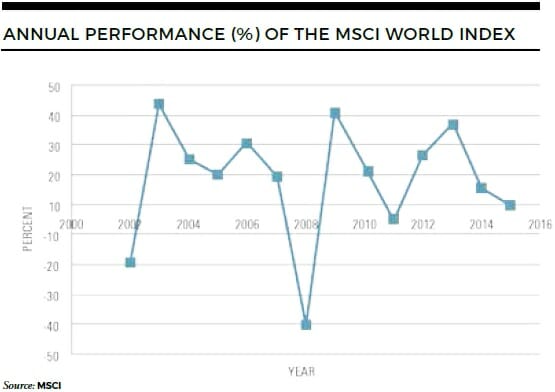

Even with a relatively positive view on some regions, the squeezing of returns in equities (see MSCI World Index chart) has led super funds to consider new strategies, with more than one shifting allocations in an attempt to be more efficient.

For example, First State Super has allocated more through its passive strategy than it did in the past, as it looks to move capital into systematic beta strategies.

“The theme is that we are holding our active managers to a higher standard and trying to capture some of what might have traditionally been regarded as alpha, through a mix of systematic beta,” Brandweiner says.

“We are trying to improve the efficiency and reduce the cost of our core equity portfolio and then deploy those savings into more active managers and more diversifying alternatives.”

The super fund has gone live with systematic beta strategies in Australian small caps and global emerging markets. These were constructed jointly with external managers, and in both cases this was done to gain beta exposures to those sectors, as well as factors within them, such as quality and value.

According to Brandweiner, one of the advantages of this approach is that it has freed up some of the fee budget, which has then be used to invest in private equity, property and infrastructure.

Better beta

Importantly, for the role of equites in the portfolio, First State Super sees long-term returns being improved by active engagement with the underlying companies in which it invests, and is devoting resources to this area to this end.

“This ties back to the universal ownership belief, but specifically, relates to the idea of what we’ve been calling ‘Better Beta’,” Brandweiner says. “Structurally, superannuation is so exposed to Australian equity beta, that over the long term it’s the growth in that beta that is going to underpin member returns, and so active involvement in corporate governance and in long-term risk management is going to be critical in supporting the long-term growth of that beta.

“That is why direct relationship with boards and CEOs (chief executive officers) is going to be of increasing importance as we, and the system, grow in size.”

Sunsuper and Telstra Super take different approaches to equites – the former favours an enhanced passive approach while the latter believes in active – but both Greg Barnes, listed shares manager at Sunsuper, and Eliopoulos have put thought into factor and smart beta strategies.

One of their mutual concerns is that as so many people are investing in these factors, returns could be arbitraged away.

In terms of Sunsuper’s investment approach, Barnes does not see the lower returns from equities having a dramatic effect, as the super fund will continue to have a very diversified portfolio with an exposure to a mixture of both growth assets and bonds.

“We will not [be] going to go out and take higher risk to chase higher returns because that introduces more volatility into the portfolio, and we don’t think our members want that,” Barnes says.

In contrast, as Telstra Super has a pretty benign view of the total return that can be got out of domestic listed equities, they are exploring other ways in which they can take on similar type of risk and that get a better outcome in terms of returns for members, says Eliopoulos.

One of these explorations has been the creation of a new asset class within the portfolio, called ‘alternative debt’.

“It’s basically investing in part of the capital structure of companies,” says Eliopoulos “It’s not investment-grade, but it isn’t common equity either; it sits somewhere in between.”

Eliopoulos thinks this asset class will deliver around 400 basis points over bank bills in terms of returns, with the investments occurring in things such as emerging market debt, bank loans and mortgage debt, some of which will be secured and others unsecured.

“It will all be publically traded, but it won’t have an investment-grade associated with it. That is how we are looking to juice up our portfolio,” Eliopoulos says.

“We’ve taken a little bit of money off listed equities as a consequence to fund that asset class. It is unlikely to be double-digit percentage weighting in our balanced fund option, but it will have a high single digit percentage.”

What parts of the market deliver the best returns?

What parts of the market deliver the best returns?

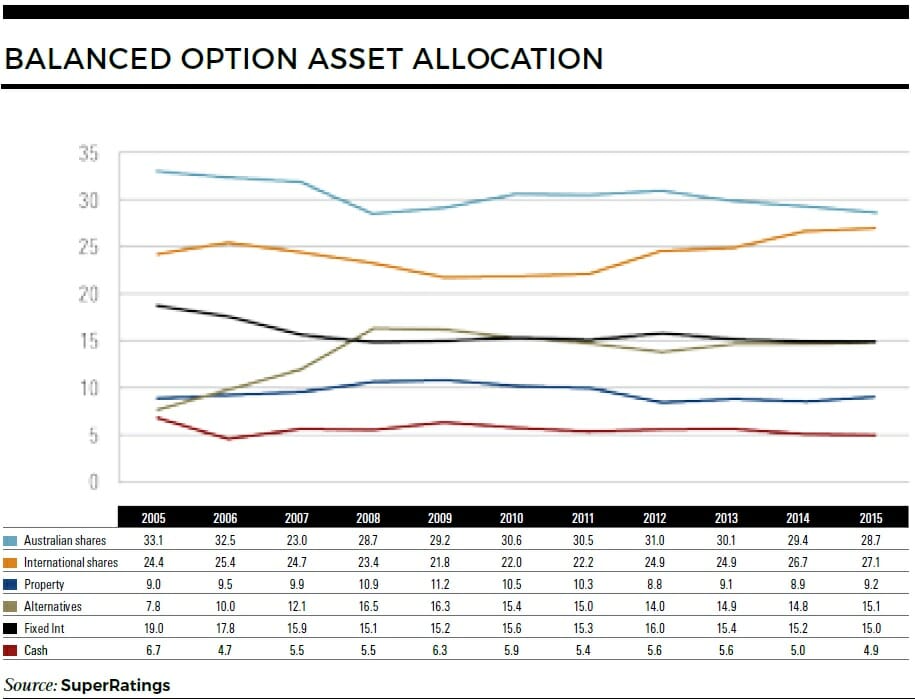

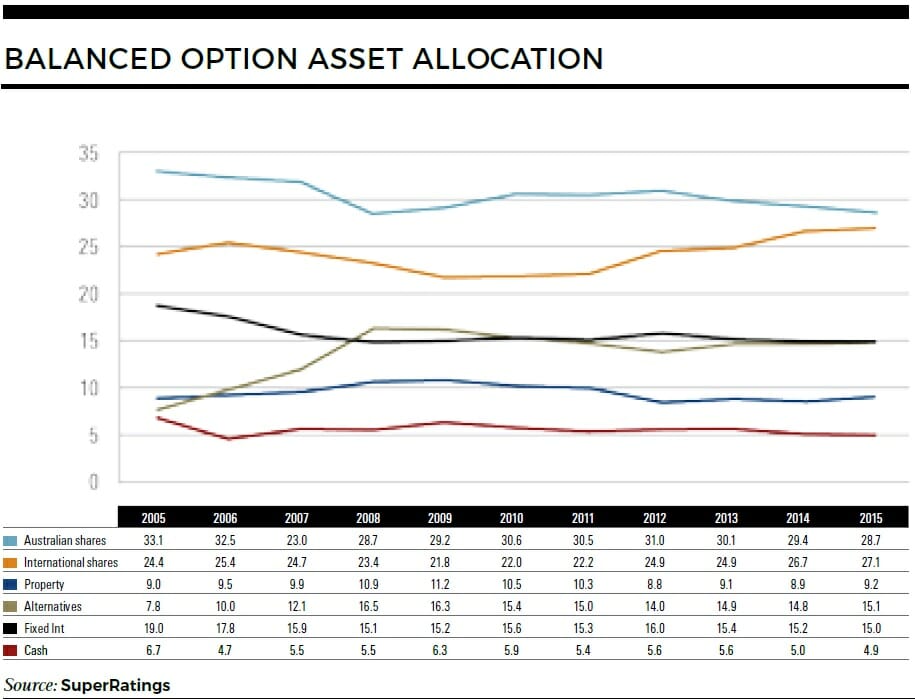

Stepping back from the recent environment and the response to it, over the past 11 years there has been an evolution of funds’ asset allocation, with the rise of alternative exposure, complemented by an increasing focus on international equity exposure, research from SuperRatings states.

This shift in allocation has naturally meant that as an average across the industry to other classes has reduced, with the greatest fall occurring in Australian shares (from 33.1 per cent to 28.7 per cent) and in fixed income (19.0 per cent to 15.0 per cent), according to the research (see box).

Alistair Barker, co-head of macro and portfolio construction at AustralianSuper, says the move away from Australian equities (from 34 per cent in 2007 to 23 per cent in 2016) is due to a number of factors.

“We have shifted away from Australia due a number of factors,” Barker says. “First, to access a wider opportunity set of high quality companies and sectors which are not available in Australia, such as IT and healthcare.

“Second, to diversify away from Australian equities, as the local market has tended to be more concentrated in a smaller number of stocks and sectors, banks and materials in particular. Third, it was also due to the shift of the portfolio away from Australia as the mining investment boom slowed down.”

A number of other super funds echo this. For instance, Sunsuper and Telstra Super are underweight in both domestic bank and material sectors.

Delving into the rationale for this, Barnes explains that while domestically the super fund and its managers are benchmarked against the ASX300, which is dominated by those two sectors, they are underweight because the Australian banks are relatively expensive and represented a concentration risk.

To help offset this, Sunsuper has an overweight to small caps within the domestic equities portfolio, and the aggregate manager exposure has the super fund overweight to industrials (for example, companies like Qantas), healthcare, consumer discretionary and consumer staple stocks.

“Once you drop outside those big sectors there is a much broader range of companies to invest in, in mid caps and small caps,” Barnes says. “Even doing that the Australian market is not nearly as broad as the international market.

“For example, technology here is a relatively small sector, and the healthcare sector, while it has had some great performance, is still small. There are a number of sectors which are far more developed internationally that we can access by going offshore.”

Increase in international equities

Increase in international equities

Over the past few years, AustralianSuper has been investing more towards international equities (from 25 per cent in 2007 to 35 per cent in 2016), particularly to developed markets, primarily due to the better macroeconomic conditions and greater amount of policy stimulus being undertaken by central banks, says Barker.

“At the other end of the spectrum, emerging markets have been affected by a combination of factors. A high US dollar, falling commodity prices, concerns over a slowdown in the Chinese economy, high interest rates in places like Brazil; all of these have created something of a perfect storm.”

However, other super funds are optimistic in their view of emerging markets.

For instance, Telstra Super has an 18 per cent weighting to emerging markets equites, compared to an indexed weighting of 11 per cent.

“The reasons for that is the fundamental premise that you’re going to get rewarded for taking on an illiquidity risk in that small part of the market,” says Eliopoulos.

“For emerging markets, the valuation metrics and the relative GDP growth in those economic regions is still relatively attractive to the developed world. It is a simple thesis, but we [are] still holding onto that view.

“Those two pockets of equity [the other being domestic small caps] still remain the best probability for getting an outsized return, from what will be an overall lower equity return going forward.”

Are we there yet?

First State Super has also been looking to increase its allocation to emerging equities and has undertaken some deep research into a range of emerging market countries, such as India, Brazil and China, to better understand the opportunities across all asset classes.

“Our sense is there is a lot of challenges in those markets, there’s a lot of noise, there’s a lot of dislocation, the currencies have been weakened, markets are down, and frequently that is when there are more opportunities than at other times in the cycle,” says Brandweiner.

“We’re not there yet, but we … are continuing to look deeply at these markets, as our sense is there is some opportunity. It may not be in listed equites, however. In some cases in these countries, it is better to go in through private allocation.”

Despite growing interest in emerging markets as a place to get returns, for the time being developed markets continue to dominate the allocation of international equities, though there are definite regional views on where is best to invest.

For instance, First State Super and Sunsuper are both underweight US equities, as earnings margins still remain at elevated levels and don’t appear to be sustainable.

“Within the portfolio we tend to have a preference for value as a style, as we think that it’s factor or a characteristic which is positively rewarded in the market. And when you look at those two big geographic regions of the US and Europe, the US is relatively expensive and Europe is relatively less expensive,” Barnes says.

While holding a similar view on the US, Sunsuper is more positive than First State Super towards Europe, and as such is overweight to Europe equites relative to the MSCI World Index.

Leave a Comment

You must be logged in to post a comment.