In public the chief investment officers of Australia’s biggest superannuation funds have been playing down the threat posed by the Brexit and Trump phenomena to their portfolio strategies. But the latest annual Investment Magazine CIO Survey reveals their private worries about the big geopolitical shocks of 2016, and their fears of more to come. A staggering 70 per cent of respondents said they were not confident of meeting their return targets in 2017. Amid the hunt for yield, in a high-risk and low-growth world, there is a glut of capital looking for a home in infrastructure and other real assets.

The fifth annual Investment Magazine CIO Survey gathered responses from the investment bosses of 40 major Australian institutional investors, collectively responsible for more than $600 billion in funds under management.

Chief investment officers from superannuation and pension funds comprised 90 per cent of the sample group, representing both the retail and not-for-profit sectors. The rest of the respondents were investment chiefs at banks or insurers.

Their answers, which remain anonymous, provide an insight into how some of country’s most influential investors are positioning their portfolios, in an increasingly volatile and unpredictable world.

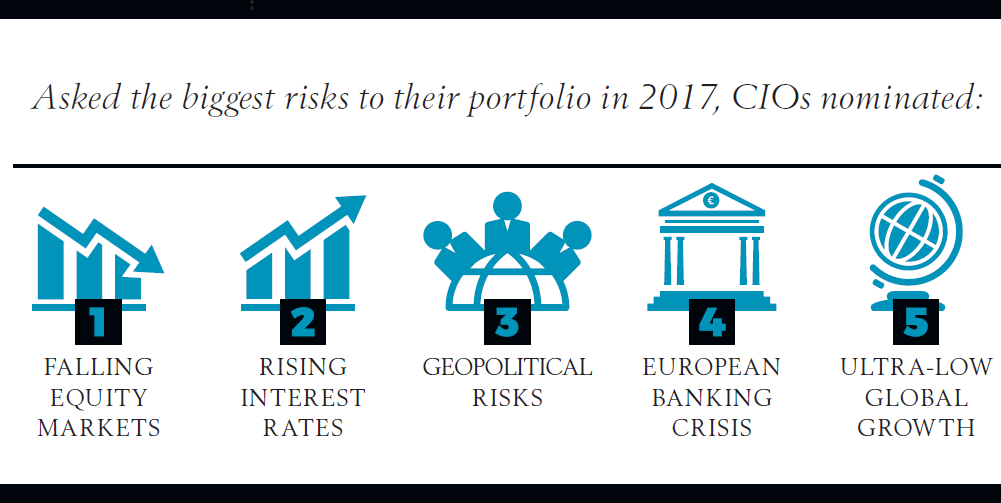

When asked to nominate the three biggest risks to their portfolio in the year ahead the asset owners revealed a few standout concerns. Falling equity markets were identified as a major portfolio risk by 70 per cent of respondents, rising interest rates by 60 per cent, and geopolitical risks by 53 per cent.

Other potential risk factors weighing on the minds of investment chiefs were the threat of a European banking crisis (nominated by 30 per cent of respondents), ultra-low global growth (28 per cent of respondents), and negative bond yields (25 per cent of respondents).

It is notable that geopolitics, which barely rated as a concern a year earlier, rocketed into the top three list of worries. Although this is perhaps not surprising given the double whammy of Britain’s shock vote in June to “Brexit” from the European Union, and the surprise victory of United States President-elect Donald Trump in November.

The 2016 Investment Magazine CIO Survey was completed in the weeks leading up to and immediately following the US election.

Anxiety about the impact of Trump’s anti-globalisation, protectionist policies on international trade and free markets loomed large.

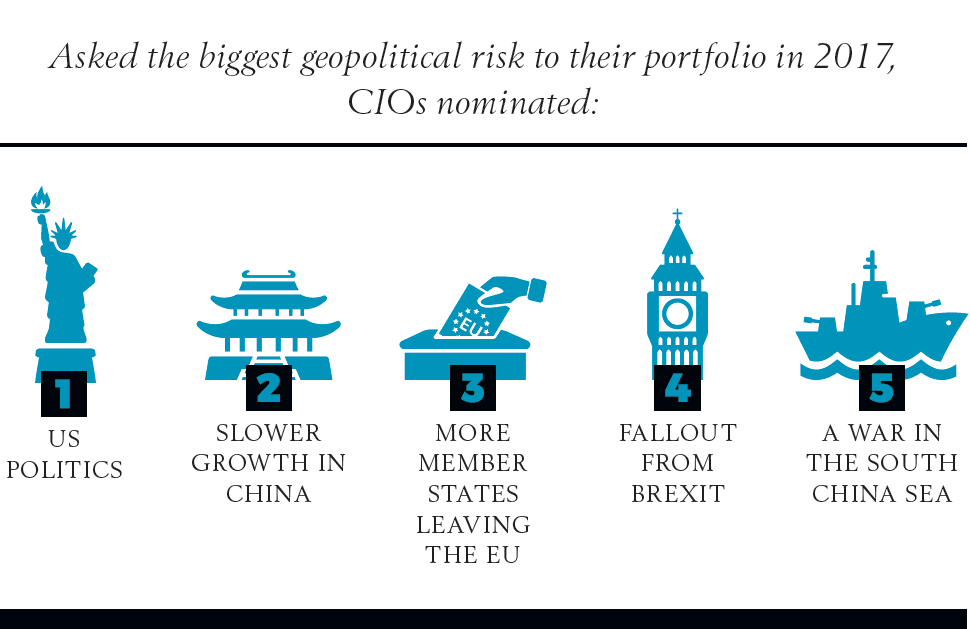

When asked to nominate the three geopolitical risks most likely to pose a threat to their portfolio in the year ahead 73 per cent of respondents pointed to US politics.

Slower growth in China and the potential for other member states to exit the European Union ranked equal second on the list of geopolitical risks, each nominated by 55 per cent of respondents.

The potential for catastrophic fallout from a trade war between declining super power the US and regional powerhouse China was something investment chiefs were keenly aware of.

Trump has threatened to impose a 45 per cent tariff on Chinese imports into the US.

One investment boss said they were concerned “aggressive trade wars led by Trump” might be “only the beginning” of the potential disruption to global markets stemming from the new president of the US.

Given that China is Australia’s biggest trading partner, with the US behind Japan as the country’s third largest trading partner, the implementation of this style of policy would likely have a big impact on the domestic economy and the equity markets that local funds are major investors in.

Add to that the risk of a break-up of the European Union, the second-largest economy in the world, and the geopolitical landscape looks rocky.

Chief investment officers pointed to the risk of nationalist candidates gaining ground in a series of upcoming European elections.

Economists have warned that the dissolution of the European Union, which could be brought about by the election of Marine Le Pen in France or a ‘no’ vote in Italy’s referendum on parliamentary powers, could have big implications for global financial markets.

One respondent said they were worried about the spread of nationalism worldwide and the risk of “more crazy, populist politicians like Filipino President Rodrigo Duterte”.

Lowering expectations

Lowering expectations

In the face of the bleak geopolitical and investment outlook, 17 of the 40 participating institutions revealed they had lowered the return targets for at least one of their investment options over the past year.

Most balanced portfolio targets are now huddled in the CPI+ 2.5 to 3.5 per cent range.

But a mere 30 per cent of respondents were confident in their fund’s ability to meet the return target on their balanced option in 2017.

A staggering 70 per cent of surveyed investment chiefs indicated they do not expect to meet these return targets in the year ahead. While 21 per cent said they definitely did not expect to hit the target, another 49 per cent felt uncertain in their ability to do so.

Looking ahead, 28 per cent of the investment chiefs said they would consider lowering return targets in 2017.

Even so, few were willing shift to a riskier asset allocation strategy, preferring instead to miss their stated targets in the short term.

“We don’t take on additional risk unless it is appropriately compensated,” one said.

A few investment bosses said they had somewhat increased their risk exposure, but were diversifying into “different types of risk”.

One described their strategy as to “just turn over more rocks”.

“Yes, we are taking on more growth assets but we are putting on more diversifiers also, if the correlation stays low to negative then the answer is no,” said another.

Others said that while the nature of risks in the portfolio had not changed they had taken “a more active approach” to managing them.

Infrastructure and other real assets stand to be the biggest beneficiaries of the hunt for yield, with 48 per cent of respondents planning to allocate more capital to this investment class in 2017.

Property is also set to see big inflows with 23 per cent of investment chiefs surveyed indicating they planned to divert more capital to real estate. The same proportion of respondents said they were planning to allocate more capital to liquid alternatives, such as hedge funds.

Other asset classes investment chiefs said they were keen to deploy more of their assets into were high yield fixed income, emerging market equities, and the private equity and venture capital markets.

Hustling on fees

With pressure on to squeeze out every basis point in low-returning markets, the scrutiny on manager fees is set to intensify.

This will only be compounded by the super funds’ plans to allocate more capital to unlisted, typically more expensive, assets classes such as infrastructure, property, hedge funds and venture capital.

When asked how important it was to reduce investment costs, on a scale of one to 10, more than half of the investment heads surveyed picked a rating higher than 7.

Negotiating harder with external managers was the preferred choice for doing this, with 87 per cent of respondents saying it was their primary method of tackling the issue.

“We would like to do more performance based fees, but they are too asymmetric in most cases (i.e. too much gain, not enough penalty for underperformance) and they’re very difficult in the Australian defined contribution context,” one respondent said.

By far the most popular fee structure for the use of a product was a management fee with discretionary discount, with 36 per cent of super funds preferring this structure. Flat fees came in second, preferred by 29 per cent of respondents.

Another chief investment officer said they approached fee negotiations on a “horses for courses” basis; typically only paying performance fees on opaque private market assets where creating alignment of interest was critical to achieving strong results.

Shifting out of high fee asset classes and allocating more to passive or smart beta strategies were other popular strategies for reducing investment costs.

One-in-five chief investment officers surveyed said they were planning to insource more of their investment capabilities, and while pressure to reduce costs featured in this decision a desire for more control was the primary motivator.

“We are growing and the benefits of scale should go to members,” said one investment chief who planned to expand their internal team.

This desire for greater control was also reflected in what investment chiefs shared when asked what they wanted from their external managers, but weren’t currently getting.

“More co-investment opportunities”, “bespoke mandates and side pockets”, and “customised solutions that use their balance sheets to come up with interesting products”, were a few responses.

Others spoke of a desire for “greater alignment” and “stronger partnerships”.

A “better deal on fees” was another common sentiment.

Other investment heads expressed a desire for more honest and robust thought leadership.

“Tell us what you believe and fear, not what you think we ought to or want to hear,” one said.

More than 80 per cent of respondents said their organisation employed an external adviser as an asset consultant, and this was not expected to change significantly over the next three years.

However the type of advice investment chiefs rely on their asset consultants for was tipped to tilt away from actual investment decisions and towards manager research.

This article first appeared in the December print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.