In the week leading up to the recent 2016 United States presidential election, UniSuper saw its members make the biggest switch to cash the fund had seen since panic gripped hold at the height of the global financial crisis in 2008.

That was enormously frustrating for UniSuper chief investment officer John Pearce. “The thing I always try to impart to members is that the best long-term strategy is to stay the course,” Pearce says.

“To me it is quite problematic positioning a portfolio for those big one-off type geopolitical events; even if you had perfect foresight of how the election was going to unfold, it would have been impossible to predict the impact on markets”.

Many of those members who “got it right” in their prediction of a Trump win, and moved to cash in anticipation, might be feeling pretty smug. But the problem is that in terms of investment outcomes they still got it wrong, and would have been better off sticking with their balanced or growth options.

The “risk-off” sentiment in global markets following Trump’s surprise victory lasted just one day before many asset classes got a bump.

US bank stocks, which UniSuper had topped-up its holdings of throughout 2016, added 15 per cent in the three weeks following Trump’s victory.

Most members who switched in the GFC did so too late, and more vexingly then left it too late to switch back to growth assets and missed the recovery.

No lack of engagement

Most super funds complain about a lack of member engagement but UniSuper is dealing with a different set of challenges that come with a membership that is “quite inquisitive and active”.

Engaging with members via investment updates over email and video is a growing part of Pearce’s remit.

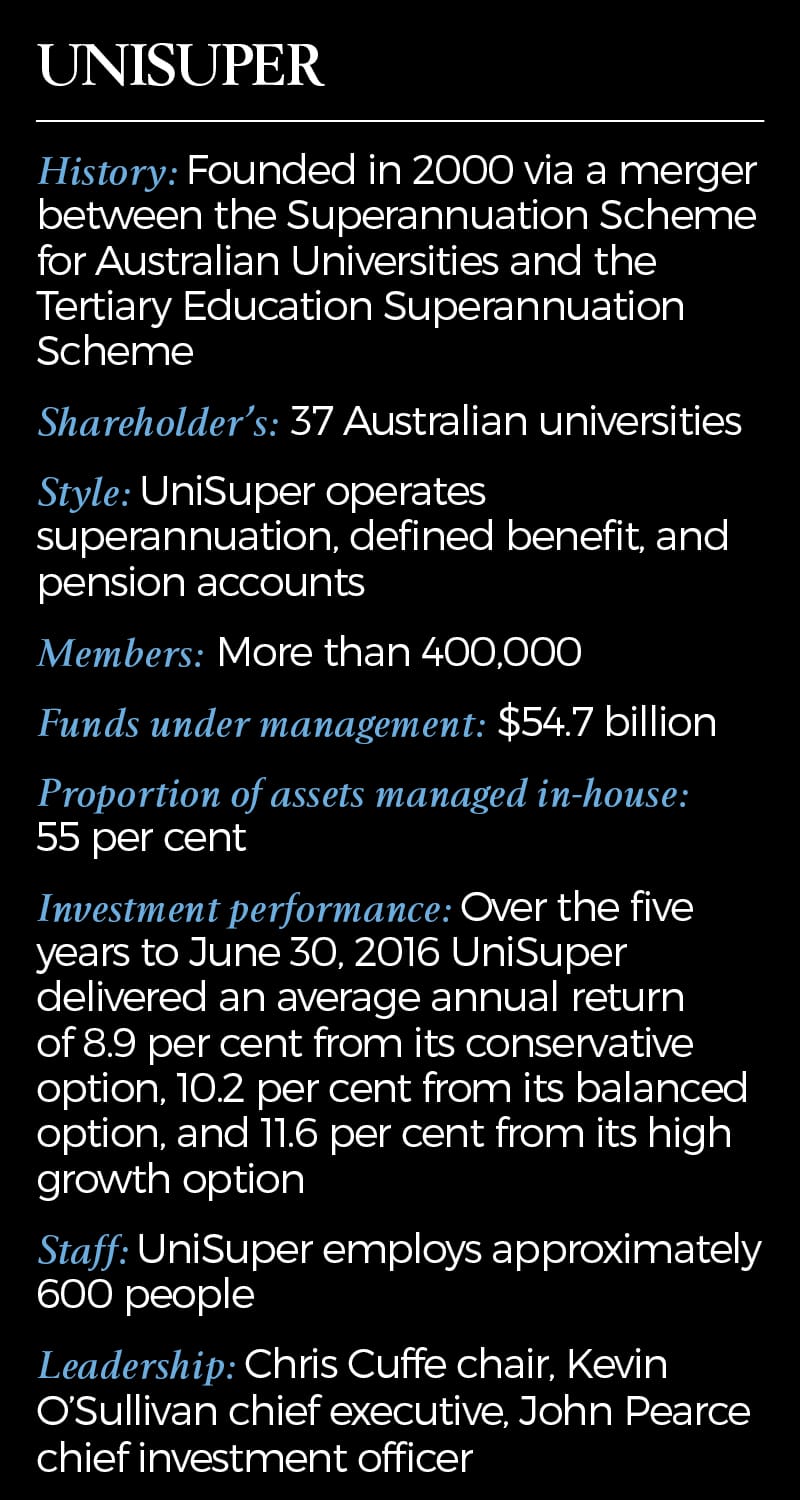

UniSuper is the country’s second largest industry fund and sixth largest super fund overall. It consistently ranks as one of the top-performing funds in terms of investment performance.

Independent director Nicolette Rubinsztein was already a fan of the chief investment officer when she joined the UniSuper board in 2015. A decade ago Rubinsztein was working for Pearce at Colonial First State when she fell pregnant with her first child.

“I was determined to work part time and I was pretty convinced I would lose my general manager role. I was reporting to John and he agreed to me working part time, and I must say, to this day I’ve been incredibly grateful for that decision,” Rubinsztein says.

“I would put him in the top two leaders that I’ve worked with. He really is outstanding.”

It has been those leadership skills, as much as his investment chops, that have defined Pearce’s tenure at UniSuper.

Seven years ago he began “insourcing” investment management, and today his internal team of 35 managers run 55 per cent of UniSuper’s assets in-house. That ratio is tipped to swell.

“We have a very scalable operation so we could take on a lot more FUM [funds under management] without hiring a lot more people,” Pearce says.

The internal team is focused on “mainstream domestic assets”, such as its large cap Australian shares portfolio. Local small cap mandates are delegated to external managers and most global stock picks are also outsourced.

At the core of the in-house strategy are what Pearce refers to as UniSuper’s “fortress assets”, which include major holdings in toll road operator Transurban, Sydney Airport, and various shopping centres.

The dominant force shaping global financial markets in 2017, “without a doubt”, will be what happens to United States Treasury yields, Pearce predicts.

Recent target reductions

Recent target reductions

In early November UniSuper lowered the return target on a number of its conservative investment options, including dropping the five-year return target on its capital stable option from CPI +2 per cent to CPI +1.5 per cent.

“The mandate for the capital stable option dictates it must be invested in 70 per cent defensive assets, so we can’t avoid having a lot of government bonds in there,” Pearce says.

With real interest rates at zero it would be “both impractical and imprudent” to target a decent margin, so members have to be warned to lower their expectations. This is especially important for retired members who may have to adjust their spending habits.

The fund’s balanced and growth options have not been lowered, although they remain under ongoing review. A much longer time horizon on balanced and growth options, of between seven to 10 years, gives investment managers more opportunity to meet the average targets.

“People panic when they see market corrections, but these are healthy. If we didn’t have market downturns we would have to keep adjusting expected returns because we would be in a bubble situation,” Pearce says.

“I’ve been in the market for 30 years and you’ve just got to keep reminding yourself that things are never as good as they seem, and never as bad as they seem”.

Watching the housing market

Over the year ahead Pearce tips European politics to throw up “a fair bit” of volatility. Closer to home, he has a watchful eye on the local housing market.

“The question is whether we’ll see a correction or an orderly working through of the excess supply of apartments, particularly in Melbourne and Brisbane”.

That is one of the reasons UniSuper reduced its holdings in Australian bank stocks over the past year, redeploying that capital into US bank stocks.

Over the past 12 months UniSuper has also deployed more capital to its US-focused global healthcare share portfolio managed by Janus, global resources portfolio managed by Henderson, and handed a new Indian equities mandate to a Schroders affiliate on the ground.

More recently UniSuper has been researching how to invest in emerging-market Asian credit for the first time, and is in the final stages of reviewing a shortlist to select an external manager for the new mandate.

More recently UniSuper has been researching how to invest in emerging-market Asian credit for the first time, and is in the final stages of reviewing a shortlist to select an external manager for the new mandate.

Pearce remains hungry for more good infrastructure assets but prefers to invest in listed vehicles.

“We tend to stay away from any of the big unlisted deals that look like they are going to get overly competitively bid,” he says, explaining why UniSuper didn’t lob bids in the recent Port of Melbourne or Ausgrid auctions.

Not one for fancy mission statements, Pearce says the closest thing he has to an investment philosophy is simply that “superannuation equals life savings”.

“That sounds quite motherhood,” he squirms, but it has proven a valuable guiding principle.

“It actually rules out a lot of things,” Pearce says. It is why UniSuper does not invest in opaque hedge funds, frontier markets, complex highly leveraged structures, or private equity and venture capital funds, he says.

An aversion to private equity funds should not be misinterpreted as a lack of appetite for private assets. Far from it. He just wants more control and transparency at a lower cost than is possible via a fund structure.

Pearce told Investment Magazine he recently almost signed a “really exciting deal in the tech space” with an undisclosed “global business that just happens to be based locally”.

“Unfortunately it fell over; I mean, it’s not dead, but it’s a complex deal and there were a few details we couldn’t get our mind around,” he said.

Having built a successful in-house team, Pearce is in a better position than ever to drive a hard bargain on fees.

UniSuper currently has external mandates with 14 Australian equity managers, 11 international equity managers, 11 property managers, eight fixed income managers and a handful of managers across other asset classes.

“We have always had the scale to negotiate pretty sharp deals with external managers. I think the in-housing has just added to that competitive strength of ours,” he says.

However he thinks investment management fees in Australia are “pretty sharp” and “takes umbrage” with the finding of the David Murray-led 2014 Financial System Inquiry that superannuation is a “high cost” industry.

Arnhem Investment Management managing partner George Clapham, who has been doing business with Pearce for “nearly a decade”, including running an Australian small caps mandate for UniSuper, says the investment chief probes his fund managers on a lot more than fees.

“John is very active in talking to us about why we make the decisions we do about certain companies,” Clapham says. “He takes an active view on things like executive remuneration.”

UniSuper was one of the institutions that succeeded in putting pressure on Commonwealth Bank of Australia to dump controversial “culture” bonuses in its latest remuneration report.

ASX-listed companies should consider themselves on notice that Pearce will continue to pushback about executive pay structures that are not aligned with shareholder value.

This article first appeared in the December print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.