Institutional asset owners worldwide have been successful at negotiating big discounts from their external fund managers. Now, Australian superannuation funds are trying to do the same, the third-annual www.top1000funds.com/Casey Quirk global CIO sentiment survey has found.

Major asset owners around the globe are under intensifying pressure to control their costs. As a result, the funds management industry, particularly locally, will need to move to more innovative fee structures.

In an environment where chief investment officers cannot rely on markets to generate high returns, and can’t control contribution levels, they are looking to what they can manipulate – costs.

The third annual www.top1000funds.com/Casey Quirk Global CIO Sentiment Survey showed that the efforts of major asset owners to reduce their costs have put investment fees under pressure. But institutions aren’t just looking for a cheaper deal, they are also seeking more innovative fee structures that create a better alignment of interests.

CIOs from 81 asset owners, across 11 countries, with combined assets under management of more than US$2.2 trillion responded to the detailed survey, revealing their outlook for fees and risk management.

All of the funds included in the survey rank among the 1000 largest institutional asset owners in the world.

These investors cited low projected returns, along with increasing stakeholder pressure, as reasons for a greater focus on costs. Poor manager performance was not a prominent reason for putting pressure on fees.

“Our investment beliefs very clearly include the statement that costs matter and need to be effectively managed,” the investment chief of one of the biggest US pension funds told the survey.

The investment chief at another large US pension fund added: “If costs can be lowered without lowering the total net-of-cost return, then net investment outcomes improve.”

Driving a hard bargain

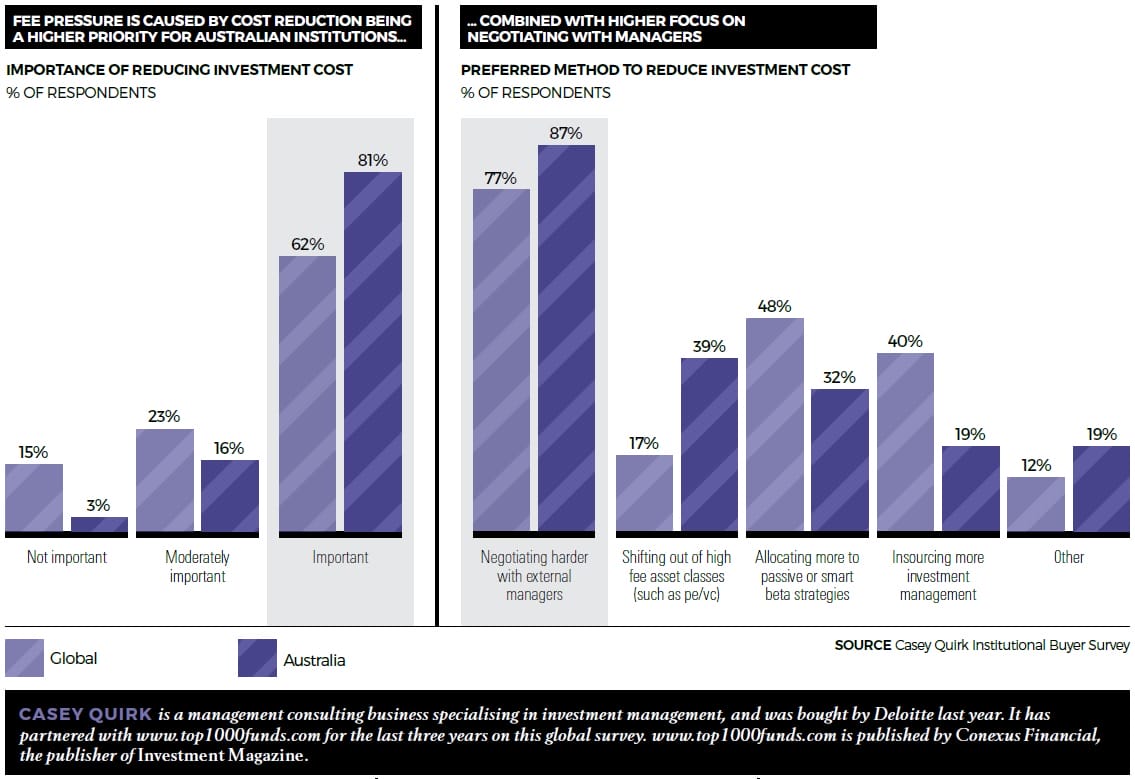

Of the 29 Australian respondents to the survey, 81 per cent rated reducing investment costs as important, versus 62 per cent for the rest of the world.

The preferred method for reducing investment costs worldwide was negotiating harder with external managers, with 77 per cent of total respondents ranking this as their favourite method. The trend was amplified in Australia, where 87 per cent of managers said negotiating a better deal on management fees was their number one cost-saving method.

This was true even though half of all respondents worldwide revealed they already get a discount from external managers, and 15 per cent said they receive a discount of more than 20 basis points. Some respondents said they received as much as a 25 per cent concession on fees. Even so, continued pressure on traditional asset-management fees was clear.

Despite the much talked about trend to insource asset management in Australia – as observed at The Future Fund, AustralianSuper, UniSuper, Cbus Super, and more recently HESTA – the survey showed other markets still emphasise this much more.

In Australia, only 19 per cent of respondents said insourcing investment management was a preferred method to reduce costs. Worldwide, that number was 80 per cent for funds with more than $75 billion in assets under management, and 36 per cent of global funds with less than $75 billion in assets under management.

Other methods for reducing costs included allocating to passive or smart beta strategies, which about half of respondents globally said they planned to do. However, just 17 per cent said they would move out of high-fee asset classes, such as private equity, in an attempt to save.

Again, this differed from the Australian respondents’ answers, which revealed that 32 per cent intended to allocate more to passive or smart beta strategies to cut costs, and 39 per cent planned to move out of high-fee asset classes, such as private equity, in an attempt to save.

Control, rather than cost, was the main motivation for Australian investors to move assets in-house.

Fees under heavy scrutiny

When funds did pay premium fees, the most common reasons they gave were limited product capacity and a lack of high-quality substitute managers, followed by strong service and value-add from managers.

A number of asset owners indicated they were most likely to waver from their focus on costs and agree to pay premium fees for managers who offered “uncorrelated returns” that strengthened their portfolio’s resilience.

“Strategies that are uniquely diversifying to the portfolio, such as those with novel factor exposure profiles, tend to be highly attractive to us and worth a greater fee premium,” one owner said.

Tony Skriba, senior consultant at the Casey Quirk Knowledge Centre, says that in addition to reducing fees, asset owners are focused on alignment of interests as well.

“Investors are looking at performance fee preferences as a preferred model globally, and asset owners think managers don’t have enough skin in the game,” Skriba says.

The survey revealed that performance fee models are of keen interest to investors, particularly the larger institutions; 60 per cent of investors with more than $75 billion in assets preferred a performance-based structure with minimum management fees.

Investors want innovation in fee structures, with a focus on retaining more of the gross value added.

Tyler Cloherty, senior manager at Casey Quirk, says the firm is seeing more innovative fee structures. “When managers move to performance fee structures, and reduce their management fees, it’s usually about retaining clients,” he says.

Cloherty says such deals are usually cut with big clients first, but as they become more normal, some fund managers are starting to adjust their business systems and processes to offer them more systematically.

He predicted a trend towards a combination of performance fees and fulcrum fees – an additional level of performance payments that kick in when an exceptionally high benchmark is met.

The Casey Quirk consultants say an ideal fee structure would probably be one where “managers get a hit on the downside” as well as benefiting from any upside.

“Managers need to alter incentives to show they’ll bear some of the risk as well as the upside,” Skriba says.

Managing risk – and expectations

In addition to wanting to reduce costs, large funds in the survey indicated they are overwhelmingly looking to lower their return expectations, with 80 per cent of funds having already reduced their return targets or planning to do so in the next year.

Locally, 58 per cent of Australian respondents said they had already lowered, or were considering lowering, their return targets.

Worldwide, the targets of respondents varied from 2 per cent to 8.5 per cent.

However, nearly three-quarters of respondents were either not confident or uncertain these would be achievable in 2017.

Nearly one-third (31.5 per cent) of respondents revealed they were “not confident” of meeting their return targets in 2017. A further 42.6 per cent were “uncertain” of reaching their return target.

Falling equity markets were cited as the biggest risk to investors’ portfolios in 2017, followed by geopolitical risks and rising interest rates.

In Australia, the clear concern for investors was rising interest rates, followed by falling equities markets and geopolitical risk, with US politics causing the most uneasiness.

This article first appeared in the March print edition of Investment Magazine. To subscribe and have the magazine delivered CLICK HERE. To sign-up for our free regular email newsletters CLICK HERE.

Leave a Comment

You must be logged in to post a comment.