OPINION |Providing better retirement solutions is a huge, complex challenge. Finding the answer starts with clearly defining what we are trying to achieve for members in retirement.

Obviously, it is easier for super funds to understand the retirement needs of those members who become financial advice clients. However, most members just default into retirement solutions without seeking any advice. What should the trustees of a super fund assume about the retirement outcome objectives of these default members?

The industry needs to mature by developing products, solutions and strategies that meet the retirement outcome challenge. Currently, the absence of a clear, measurable objective hinders the industry’s efforts.

This was the idea behind the Member’s Default Utility Function Version 1 (MDUF v1) project. We as funds typically know little about our default members. MDUF v1 is a framework developed to address this. A panel of academics and industry professionals has established it to determine an appropriate, sensible set of objectives for trustees to assume on behalf of their default fund members. The panel (detailed in the box) has more than 200 years of relevant experience.

We believe this new framework outlines how this challenge can be met.

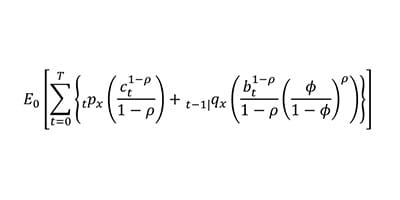

Throughout the MDUF v1 project, the panel asked: What is a sensible set of financial preferences for a trustee to assume on behalf of a default fund member?

These preferences were then converted into a mathematical function, known as a utility function. This was given the name Member’s Default Utility Function Version 1 – MDUF v1 for short.

MDUF v1 captures preferences that are intuitive but aren’t considered by other metrics. In particular, it recognises the importance of income level and variability. It also places a value on any residual benefit and acknowledges that most people are risk averse.

MDUF v1 is a credible and powerful metric that industry, regulators and policymakers can use for varying purposes. Possible applications include: post-retirement solution design by super funds and other product providers, assessment of design by regulators and ratings groups, and welfare analysis by policy groups.

MDUF v1 is a credible and powerful metric that industry, regulators and policymakers can use for varying purposes. Possible applications include: post-retirement solution design by super funds and other product providers, assessment of design by regulators and ratings groups, and welfare analysis by policy groups.

We all know existing retirement outcome metrics the industry uses are flawed. We believe MDUF v1 is superior. The project took about 18 months to complete, due to robust discussion and deep research. We are proud that we have been able to make MDUF v1 available to all through an open architecture format supported by the Australian Institute of Superannuation Trustees and the

Association of Superannuation Funds of Australia, which have jointly taken on the role of custodians of this work.

We encourage the industry to collaborate further on addressing the retirement outcome challenge and we see the sharing of this work as a step in that direction.

David Bell is the chief investment officer of Mine Wealth + Wellbeing and one of the lead authors of the research paper, Member’s Default Utility Function Version 1. The MDUF v1 paper research and framework was unveiled at the Conexus Financial Post Retirement Conference 2017. This article first appeared in the March print edition of Investment Magazine.

Leave a Comment

You must be logged in to post a comment.